by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with the latest on the US-Israeli war against Iran, including news that the US will support a rebuilding fund for Iran. We next review several other international and US developments that could affect the financial markets today, including the European Parliament’s formal approval of last year’s trade deal between the US and the EU and a few words about the Federal Reserve today as it starts its first policy meeting helmed by new Chair Kevin Warsh.

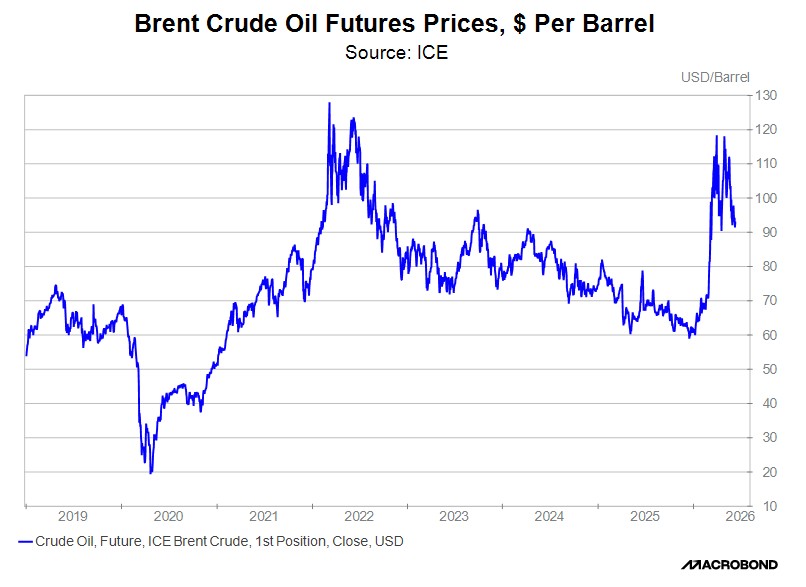

United States-Israel-Iran: Citing an unidentified senior US official, the Financial Times late yesterday said the Trump administration is prepared to allow the private sector to establish a $300-billion investment fund for Iran if Tehran agrees to a final settlement to end the war that includes a nuclear deal. According to the official, sanctions relief and the fund “to rebuild their country” would be connected to Iran’s “performance” in adhering to the framework of the US-Iran ceasefire extension that is to be formally signed on Friday.

- If the reporting is accurate, it could draw criticism as payment of reparations to Iran or bribing the country to get a nuclear deal. Even though the proposed fund would apparently be financed by private companies, Washington could offer tax or regulatory incentives for companies to participate, essentially transforming the fund into a US institution.

- Separately, the chief executive of Mitsui OSK Lines, the world’s biggest operator of oil tankers, has warned that shippers will not resume transit through the Strait of Hormuz for weeks until they are confident that the US-Iran deal is “material.” That being the case, he estimated that shipping through the strait probably won’t start in earnest until at least two weeks after the new US-Iran ceasefire extension is formally signed on Friday. Such a delay would further raise the risk of new surges in energy prices.

United States-European Union: The European Parliament today finally approved the trade deal reached last year between President Trump and European Commission President von der Leyen. Under the deal as it now stands, the US is relying on temporary emergency legislation to impose a 10% levy on top of existing duties, putting the total US duty north of 15% for some products. Meanwhile, the EU will cut its duties on US industrial goods and some farm products to 0%. The formal parliamentary approval will now provide more certainty in US-EU trade.

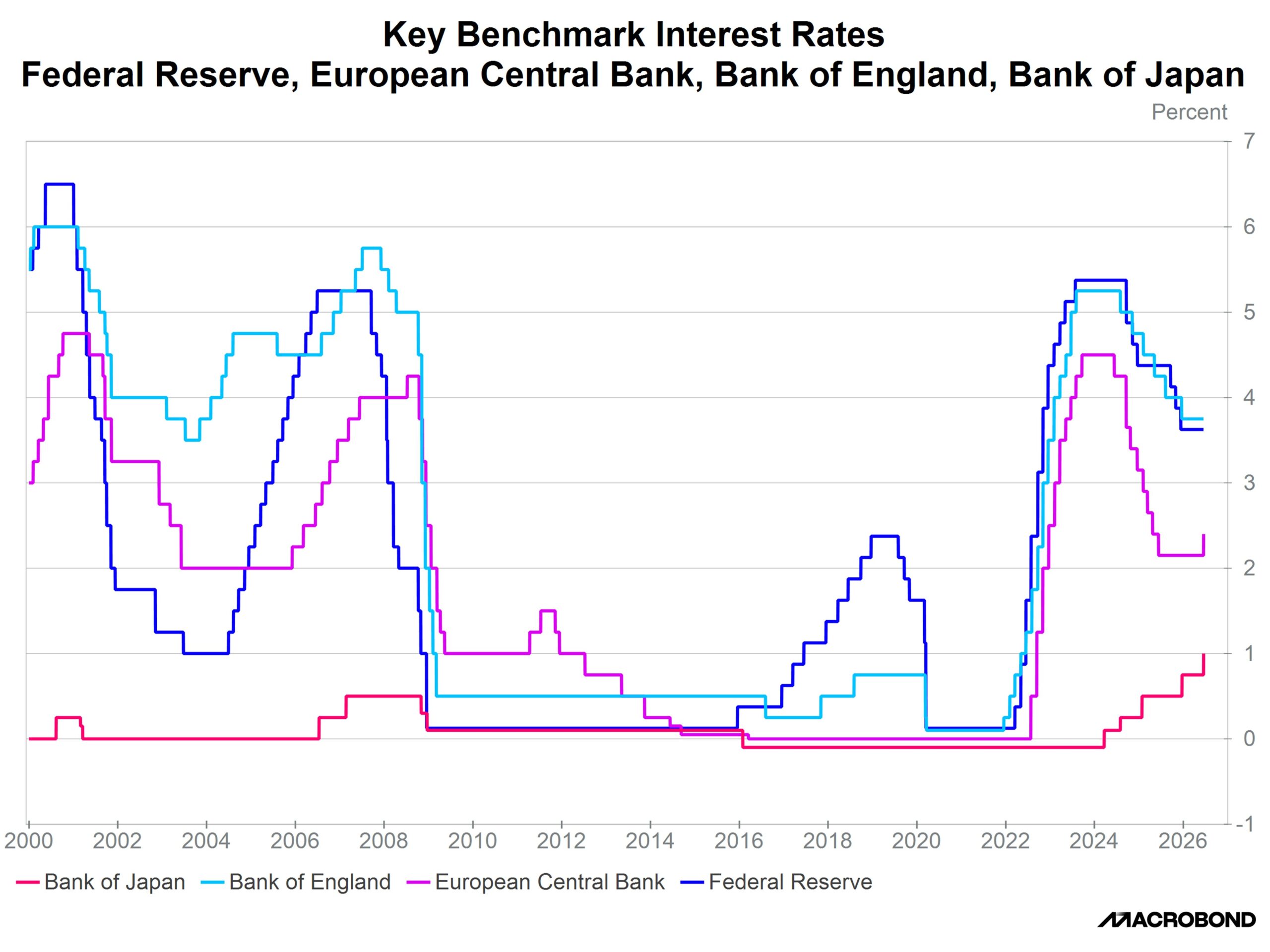

US Monetary Policy: The Fed starts its latest two-day policy meeting today, with its decision due tomorrow at 2:00 PM ET. This will be the first policy meeting led by new Fed Chair Warsh, with former Chair Powell also at the table. Based on the latest futures trading, investors are nearly unanimous in expecting the policymakers to hold their benchmark fed funds rate steady at a range of 3.50% to 3.75%. In fact, investors appear to be assuming rates will be held steady through the end of the year.

US Defense Industry: In a scoop last night, the Wall Street Journal said auto giant General Motors is in talks with Lockheed Martin about making parts for the defense contractor’s weapons. Under the arrangement, GM would manufacture commonly used parts that could help Lockheed bolster munitions output. The companies are currently discussing which components GM could potentially make.

- The potential deal harkens back to the World War II era, when many civilian firms shifted rapidly to military production to leverage their manufacturing expertise and excess capacity.

- The potential Lockheed-GM deal echoes developments that we’ve also seen in Europe, where firms with idle civilian production lines have made their workers and facilities available to support the Continent’s rearmament.

- In sum, the phenomenon illustrates how increasing defense budgets around the world are creating financial opportunities for firms far beyond the defense sector.

Japan: As widely expected, the Bank of Japan today raised its benchmark short-term interest rate to a 31-year high of 1.00%, compared with 0.75% previously. The hike reflects Japan’s new experience of continued high price inflation, as well as concerns about the weakness of the yen. The move follows the European Central Bank’s rate increase last week, which was also driven in large part by inflation concerns as global energy and commodity prices have jumped in response to the war in Iran.

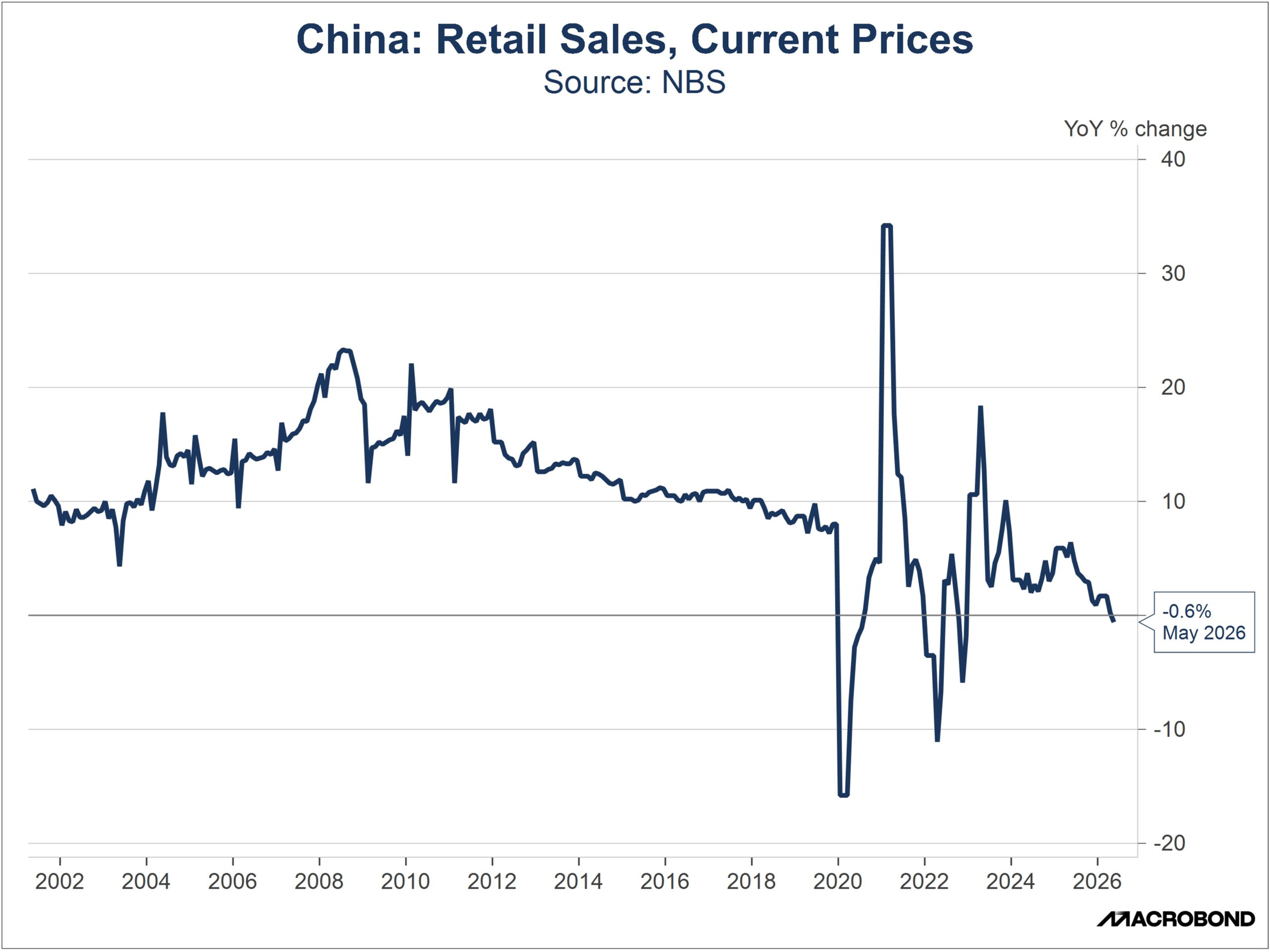

China: May retail sales were down 0.6% from the same month one year earlier, marking their first annual decline since 2022 and illustrating the country’s persistently weak domestic demand. Meanwhile, fixed-asset investment in January through May was down 4.1% on the year, largely because of an ongoing slump in property investment. The weakness in Chinese domestic demand will likely encourage the government to keep emphasizing exports for growth, which in turn will keep pressuring foreign firms and raising international trade tensions.

Global Gold Market: A survey by the World Gold Council shows many major central banks, including those of France and India, have been pulling their gold reserves out of New York and London as they worry more about the security of their holdings. The finding illustrates just how concerned central bank reserve managers have become about geopolitical risk. Although central banks and some other major market participants have sold gold in recent months to raise liquidity, that concern suggests they will resume buying once the US-Iran conflict eases.