Portugal held parliamentary elections on October 4, 2015, in which the incumbent center-right Social Democratic Party received the most votes but fell short of an outright majority. Historically, as part of the Portuguese political process, the country’s president tasks the party that receives the most votes with forming a government. However, in this case, the center-left opposition party and some far-left parties have formed a coalition, together garnering a majority of votes and currently awaiting presidential approval to form a government and take control from the center-right party.

This week, we will look at the current political environment in Portugal. First, we will start with a brief history of Portugal. We will then turn to the economic conditions leading up to the most recent elections and discuss the election results, the change in coalition powers and the possible path of developments going forward. As always, we will conclude with market ramifications.

There is no doubt that the EU migrant crisis is a catastrophe in terms of human costs. It is fairly evident that the EU was not prepared to deal with the magnitude of migrant movement into the region. This crisis also presents a political dilemma for Europe and may lead to the re-establishment of border controls, intensify internal schisms over the extent of sovereign/EU authority and possibly sow the seeds of the dissolution of the EU.

Migrant flows from the Middle East and Africa have affected European countries unevenly. The border countries have received heavy inflows of migrants, some of whom wish to stay in those countries, but most continue on to Germany and Sweden, which have indicated openness to accepting immigrants. However, many countries are not open to taking immigrants, either due to a lack of ability or willingness. Each of these countries is dealing with the flow of asylum-seekers differently as their approach is determined by relative economic wealth, number of immigrants and societal structure.

Hungary has received an overwhelming number of immigrants due to its location on the main migrant routes to Germany and Sweden. The large number of immigrants, both in absolute terms and relative to Hungary’s population, has overwhelmed the country’s refugee facilities. Hungary has indicated that it cannot accept all refugees without a clear plan from Brussels and has tried various tactics to control the immigration flow, from erecting a 108-mile barbed wire fence to simply facilitating refugee transportation to the Austrian border.

This week, we will look at how Hungary is handling the immigrant crisis and what its actions may signal for other European countries. We will start by looking at Hungary’s history and its position at the crossroads of empires which have shaped Hungary into a country that often directs a changing tide for Europe. As always, we will conclude with geopolitical and market ramifications.

Over the past three years, we have witnessed what appears to be a steady erosion of American power. Russia annexed the Crimea and has encouraged a rebellion in eastern Ukraine, undermining the sovereignty of a European nation. This apparent invasion was considered by Western observers to be the first hostile acquisition of territory since WWII.

The breakdown in the Middle East has become another problem. The U.S. allowed the Arab Spring to unfold with little interference; to some extent, the administration encouraged the developments. The U.S. took a secondary role when intervening in Libya, allowing France and Britain to lead operations. That action has devolved into a disaster; Libya stands divided as various ethnic and sectarian groups fight for control. Syria has become a major problem as well. The administration has pressed for the removal of Syrian President Assad but hasn’t created conditions to foster his exit. The decision not to bomb Syria after Assad used chemical weapons, a self-proclaimed “red line” by President Obama, further gave the impression of disengagement.

Russia’s recent decision to send military equipment and personnel to Syria suggests that Putin is filling a power vacuum in the region. Sunni allies in the region are becoming increasingly concerned that the U.S. is not going to continue to play the role of outside stabilizer in the region.

Yet, the Obama administration recently announced that it would send U.S. Naval vessels within 12 miles of the artificial islands that China is building in the South China Sea. Although military advisors have been pushing for such incursions for some time, the president’s decision to take this rather aggressive step is in direct contrast to the passive response seen in other areas of the world.

In this report, we will examine President Obama’s foreign policy, using the construct of Ian Bremmer’s recent book, Superpower.[1] After discussing President Obama’s foreign policy and the potential effects, we will examine how the next president may shift from the current policy. As always, we will conclude with potential market ramifications.

The Federal Reserve decided not to raise rates in the third quarter. Attention now turns to if, when and how it will raise rates going forward. Although we expect the Fed to move gradually and not cause a recession, the likelihood of policy errors has increased.

We continue to believe both growth and inflation are likely to remain low in the United States. Still, we expect U.S. growth to be higher than that of many foreign countries.

Financial market returns are likely to remain lower than the rates earned in recent years. At the same time, we expect volatility will continue to rise.

Our equity allocations remain focused on domestic stocks and include large, mid and small caps.

We continue to favor intermediate and longer maturity bonds, which should continue to provide diversification and reasonable returns in an environment of low growth and low inflation.

Our style guidance remains in favor of growth over value but shifts from 70/30 to 60/40.

ECONOMIC VIEWPOINTS

Over the summer, investors had to deal with a variety of issues affecting the financial markets. These included Greece and its debt, Middle East turmoil, and currency and equity swings in China. While each of these issues was relevant, none got more attention than the Federal Reserve. Investors watched to see whether or not the Fed would raise short-term rates in September, and what the policy guidance might be going forward. Ultimately, the Fed did not raise rates, acknowledging low inflation, limited wage pressure and weak global growth. This decision created a bit of a relief rally near the end of the quarter, but now all attention shifts to what the Fed may do in the fourth quarter and 2016.

Because we expect economic growth and inflation to remain low, we believe the Fed is inclined to move very slowly and any rate increases are likely to be telegraphed with a high amount of clarity. We don’t foresee a recession, but do recognize that the likelihood of Fed policy mistakes has grown—tightening in a low growth environment can be hazardous. Absent a recession, however, the environment should be reasonably good for investors. Broadly speaking, we expect asset returns to remain lower than recent years and volatility to rise. Less return and more risk is far from ideal, but investors should keep in mind that multiple years of easy monetary policy have created unusually high returns and particularly low volatility. As such, if and when the Fed begins to tighten, the overall return/risk profile should remain attractive, but will probably not be as favorable as it has been.

It’s also important to factor in ongoing geopolitical frictions. For many years, we’ve written about the withdrawal of the United States from its superpower role. As this trend has unfolded, we’ve witnessed rising regional instability around the world, ranging from the European migrant crisis to China’s territorial expansion in the South China Sea. In addition, the U.S. also faces its own brand of geopolitical change as 2016 is a presidential election year. Although all these factors have varying amounts of direct impact on the U.S. financial markets, they are sources of potential or perceived risk.

To address rising volatility and geopolitical risk, we maintain a diversified posture, one that includes a variety of asset classes. Diversification is important, but so too is the nature of the exposure. Accordingly, we remain overwhelmingly domestic in our equity allocations. This positioning reflects our belief that the U.S. will lead the global economy, making domestic equities relatively more attractive. However, even as the global leader, we expect fairly modest U.S. economic growth, making intermediate and longer maturities more attractive in our bond allocations. We had most of these positions already in place, and therefore we make few allocation changes this quarter.

STOCK MARKET OUTLOOK

Stock volatility has continued to rise in 2015, with some indices dipping near correction territory during the late summer only to recover in October to a range not far from where they began the year. China’s currency, economic growth, equity market volatility and governmental policies often played in the minds of equity investors, particularly in the third quarter. Even more important to investors was Fed policy. By passing on a rate increase in September, the Fed recognized slow U.S. growth and the drag caused by weak foreign economies. So, going forward, we believe the Fed will move very slowly with great transparency. Its policy will remain important to equity investors who will carefully watch to see if the Fed goes too far or too fast.

Fundamentally, stocks remain in good shape, although earnings growth has slowed significantly for many companies. Valuations are reasonable and tend to reflect a degree of risk aversion. This trend has helped curb a cycle of excessive valuation. We continue to favor domestic equities over foreign ones, given our belief that the U.S. should lead global growth trends. We recommend exposures across capitalization sizes and our favored large cap sectors include technology and consumer discretionary, while we are underweight energy, healthcare, financials, basic materials and telecom. Our style bias continues to favor growth over value, although we dial down the bias this quarter from 70/30 to 60/40, reflecting our changing preference for a more balanced posture.

BOND MARKET OUTLOOK

For many years, bond investors have lamented the low interest rate environment and the challenges in pursuing reasonable returns in fixed income portfolios. While it’s true that returns have declined, bonds continue to offer lower levels of volatility and meaningful diversification relative to equities and other asset classes. These characteristics are often overlooked, but when volatility and risk rise in the markets, they become more apparent…and appreciated.

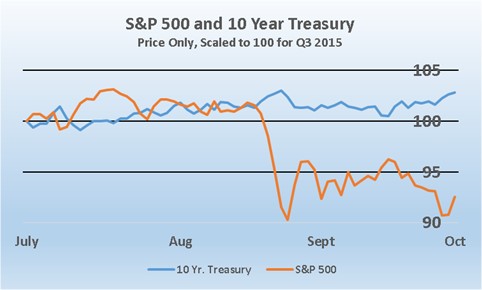

The chart to the right illustrates this point. The prices of the S&P 500 (in red) and the 10-year Treasury (in blue) are scaled to a common value (100) at the beginning of the third quarter. Two characteristics are noteworthy. First, the Treasury price changes are comparatively mild, remaining within a four percent range during the quarter. In contrast, the stock index was much more volatile, with a range of almost 13 percent. Second, note how the 10-year Treasury moved in opposite direction of the S&P 500 (this is called a negative correlation). Having investments in securities that don’t behave in the same manner is an important part of managing risk. So, even while bond returns have not been particularly high, their contributions in a portfolio have been significant.

Source: Bloomberg, CIM

As we move into a period when financial market volatility is likely to rise, bonds can continue to play an important role in helping to address risk. We maintain allocations to intermediate and longer maturities, which we believe can perform well in a low growth environment. We also remain overweighted toward high quality corporate bonds, which we expect to have relatively mild default rates.

OTHER MARKETS

Real estate faced headwinds earlier in the year when interest rates moved higher and investors became concerned about tighter Fed policy. However, this asset class has benefited from the recent decline in interest rates. We continue to believe real estate can play a constructive role in portfolios, particularly where income is an objective. Occupancy and rental rates are keeping fundamentals strong, while foreign investors continue to move into the space.

Our view toward commodities has begun to improve at the margin. However, we remain out of this asset class given large amounts of excess supply capacity for most commodities around the world. Furthermore, China’s slowing growth continues to limit demand and we don’t believe the correction in commodities has yet reached a point where an allocation is appropriate.

On October 6, trade negotiators announced a final agreement for the Trans-Pacific Partnership (TPP), a multilateral trade deal between 12 Pacific Rim nations in both the eastern and western hemispheres.

In this report, we will begin by discussing the nations involved. We will examine some of the details of the treaty. An analysis of the geopolitics will follow along with a look at specific political factors surrounding the treaty. As always, we will conclude with potential market ramifications.

“Catalonia, a new state within Europe” is the slogan of the pro-independence secession movement in the Spanish region of Catalonia. Catalonia has always pined for more autonomy, but calls for secession have intensified as the Spanish economy has suffered from slow growth and corruption scandals have discredited the central government. At the end of September, Catalonia held regional parliamentary elections. These elections were touted by some as a prelude to Catalan secession from Spain. However, the Spanish federal government has made it clear that it will not hold negotiations for secession and, in fact, even holding an independence referendum is considered unconstitutional. Although the majority of Catalans support independence, they could likely be appeased with more autonomy, especially financial autonomy.

This week, we will look at the separatist movement in Catalonia. We will start by giving a brief overview of the region’s history and politics, then look at the roots of the independence movement. We will explore the probability of independence, the potential future relationship between the region and the central government, and the roles of the EU and the Eurozone. As always, we will conclude with market ramifications.

Back before talk radio became the domain of either political opinionates or “shock talkers,” it was dominated by the friendly conversation of morning humorists in the path established by Arthur Godfrey. Here in St. Louis, a very funny fellow named Jack Carney dominated the airwaves in the mid-morning for a generation. At least a quarter of all the radios in the area were tuned in to his show during his time slot, ratings current radio execs can only dream of. One of his recurring call-in guests was an elderly woman named “Miss Blue.” She and Jack engaged in funny chit-chat that always began and ended with her pronouncing (in a delightful Southern accent) that, “Aaw-ll is way-ll!” You just had to smile when she said it. I think of her when I field calls from agitated friends who are concerned that the world is falling apart. I just want to tell them that, “All is well,” and have it calm them in the way that Miss Blue did.

Of course, people won’t believe that all is well, which, of course, it never is. But all is rarely on the verge of doom either, even though these days that’s what many people seem to think. We are always wrestling with a number of difficult problems in the world economy; the trick is to identify the ones that really matter. Only rarely do the ones that the “talking heads” fixate on really matter to your portfolio. In a nutshell, here are the problems that I think really matter:

The level of U.S. consumer debt is still relatively high (though down quite a bit from seven years ago), leading to low levels of consumer spending and, hence, slow growth in the U.S. economy. These phenomena won’t change anytime soon.

China and the emerging markets are seeing their growth decelerate at alarming rates, simply because the U.S. is not buying as much of their goods as it used to. China, in particular, is trying to transition to a more sustainable consumer-oriented economy, but this transition will take a very long while and will probably stumble a few times. These phenomena will probably get worse before they get better.

Our Federal Reserve seems determined to raise short-term interest rates, even though we see no inflation problem coming and believe there is a fair amount of “slack” in our economy. I was glad to see them postpone the rate increase last month and hope they keep postponing it. This question of Fed policy will remain with us for quite a while.

Problem #1 has been with us for a long time, so we’ve learned to deal with it. Slow growth is no fun but, like getting old, it beats the alternative. Problem #2 will continue to trouble us, but because we buy a lot more from the developing world than we sell to them, their problems will generally not be imported to us. We are embarking on a time, I believe, when the emerging markets’ economies will be worse than ours. Finally, problem #3 is the one we should worry about the most. Although they are well-meaning people, the Fed’s Open Market Committee has sometimes done harm by setting the wrong policy at the wrong time. We are encouraged that they are still waiting to raise rates.

As I noted in last quarter’s letter, investment conditions in the U.S. really are much better than the rest of the world. Particularly after the recent decline in equity prices, U.S. stocks are more reasonably priced than we’ve seen in a while. It appears to me that the investor pessimism is considerably “over-shooting” the reality of the situation. In other words, I think the investment outlook is much better than it “feels,” even if it’s not quite as good as Miss Blue would say.

Thank you for your confidence in us.

Gratefully,

Mark A. Keller, CFA CEO and Chief Investment Officer

Last month, Russia moved a significant amount of military hardware into areas of Syria controlled by the Assad regime. The action caught the Obama administration by surprise and raises questions about what Russian President Putin is trying to accomplish.

In this report, we will examine Russia’s short-term geostrategic goals and the tactics Putin is using to achieve these aims. As always, we will conclude with potential market ramifications.

Meteorologists have been calling for an El Niño event since last year. Current forecasts place the likelihood of an El Niño occurrence this winter at over 90%. Now, talk has turned from the likelihood of an El Niño to whether the abnormal weather pattern event will be super-sized or monster-sized. Water temperatures in the Pacific, one of the first signs of a looming El Niño, have measured much higher than normal. In fact, water temperatures have been on par with the most severe El Niño event from the past 30 years. As investors, we monitor larger climate events as severe weather can have an effect on most commodity markets.

This week, we will look at how an El Niño develops and its possible climate, economic and geopolitical effects on the global economy. As always, we will outline the potential investment implications of this event.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.