Asset Allocation Quarterly (Fourth Quarter 2015)

- The Federal Reserve decided not to raise rates in the third quarter. Attention now turns to if, when and how it will raise rates going forward. Although we expect the Fed to move gradually and not cause a recession, the likelihood of policy errors has increased.

- We continue to believe both growth and inflation are likely to remain low in the United States. Still, we expect U.S. growth to be higher than that of many foreign countries.

- Financial market returns are likely to remain lower than the rates earned in recent years. At the same time, we expect volatility will continue to rise.

- Our equity allocations remain focused on domestic stocks and include large, mid and small caps.

- We continue to favor intermediate and longer maturity bonds, which should continue to provide diversification and reasonable returns in an environment of low growth and low inflation.

- Our style guidance remains in favor of growth over value but shifts from 70/30 to 60/40.

ECONOMIC VIEWPOINTS

Over the summer, investors had to deal with a variety of issues affecting the financial markets. These included Greece and its debt, Middle East turmoil, and currency and equity swings in China. While each of these issues was relevant, none got more attention than the Federal Reserve. Investors watched to see whether or not the Fed would raise short-term rates in September, and what the policy guidance might be going forward. Ultimately, the Fed did not raise rates, acknowledging low inflation, limited wage pressure and weak global growth. This decision created a bit of a relief rally near the end of the quarter, but now all attention shifts to what the Fed may do in the fourth quarter and 2016.

Because we expect economic growth and inflation to remain low, we believe the Fed is inclined to move very slowly and any rate increases are likely to be telegraphed with a high amount of clarity. We don’t foresee a recession, but do recognize that the likelihood of Fed policy mistakes has grown—tightening in a low growth environment can be hazardous. Absent a recession, however, the environment should be reasonably good for investors. Broadly speaking, we expect asset returns to remain lower than recent years and volatility to rise. Less return and more risk is far from ideal, but investors should keep in mind that multiple years of easy monetary policy have created unusually high returns and particularly low volatility. As such, if and when the Fed begins to tighten, the overall return/risk profile should remain attractive, but will probably not be as favorable as it has been.

It’s also important to factor in ongoing geopolitical frictions. For many years, we’ve written about the withdrawal of the United States from its superpower role. As this trend has unfolded, we’ve witnessed rising regional instability around the world, ranging from the European migrant crisis to China’s territorial expansion in the South China Sea. In addition, the U.S. also faces its own brand of geopolitical change as 2016 is a presidential election year. Although all these factors have varying amounts of direct impact on the U.S. financial markets, they are sources of potential or perceived risk.

To address rising volatility and geopolitical risk, we maintain a diversified posture, one that includes a variety of asset classes. Diversification is important, but so too is the nature of the exposure. Accordingly, we remain overwhelmingly domestic in our equity allocations. This positioning reflects our belief that the U.S. will lead the global economy, making domestic equities relatively more attractive. However, even as the global leader, we expect fairly modest U.S. economic growth, making intermediate and longer maturities more attractive in our bond allocations. We had most of these positions already in place, and therefore we make few allocation changes this quarter.

STOCK MARKET OUTLOOK

Stock volatility has continued to rise in 2015, with some indices dipping near correction territory during the late summer only to recover in October to a range not far from where they began the year. China’s currency, economic growth, equity market volatility and governmental policies often played in the minds of equity investors, particularly in the third quarter. Even more important to investors was Fed policy. By passing on a rate increase in September, the Fed recognized slow U.S. growth and the drag caused by weak foreign economies. So, going forward, we believe the Fed will move very slowly with great transparency. Its policy will remain important to equity investors who will carefully watch to see if the Fed goes too far or too fast.

Fundamentally, stocks remain in good shape, although earnings growth has slowed significantly for many companies. Valuations are reasonable and tend to reflect a degree of risk aversion. This trend has helped curb a cycle of excessive valuation. We continue to favor domestic equities over foreign ones, given our belief that the U.S. should lead global growth trends. We recommend exposures across capitalization sizes and our favored large cap sectors include technology and consumer discretionary, while we are underweight energy, healthcare, financials, basic materials and telecom. Our style bias continues to favor growth over value, although we dial down the bias this quarter from 70/30 to 60/40, reflecting our changing preference for a more balanced posture.

BOND MARKET OUTLOOK

For many years, bond investors have lamented the low interest rate environment and the challenges in pursuing reasonable returns in fixed income portfolios. While it’s true that returns have declined, bonds continue to offer lower levels of volatility and meaningful diversification relative to equities and other asset classes. These characteristics are often overlooked, but when volatility and risk rise in the markets, they become more apparent…and appreciated.

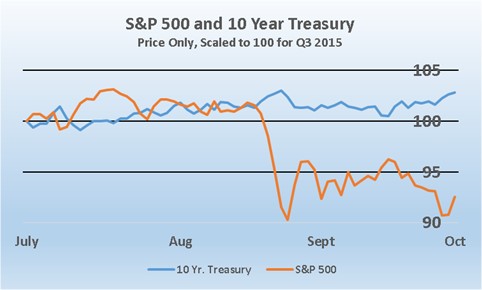

The chart to the right illustrates this point. The prices of the S&P 500 (in red) and the 10-year Treasury (in blue) are scaled to a common value (100) at the beginning of the third quarter. Two characteristics are noteworthy. First, the Treasury price changes are comparatively mild, remaining within a four percent range during the quarter. In contrast, the stock index was much more volatile, with a range of almost 13 percent. Second, note how the 10-year Treasury moved in opposite direction of the S&P 500 (this is called a negative correlation). Having investments in securities that don’t behave in the same manner is an important part of managing risk. So, even while bond returns have not been particularly high, their contributions in a portfolio have been significant.

As we move into a period when financial market volatility is likely to rise, bonds can continue to play an important role in helping to address risk. We maintain allocations to intermediate and longer maturities, which we believe can perform well in a low growth environment. We also remain overweighted toward high quality corporate bonds, which we expect to have relatively mild default rates.

OTHER MARKETS

Real estate faced headwinds earlier in the year when interest rates moved higher and investors became concerned about tighter Fed policy. However, this asset class has benefited from the recent decline in interest rates. We continue to believe real estate can play a constructive role in portfolios, particularly where income is an objective. Occupancy and rental rates are keeping fundamentals strong, while foreign investors continue to move into the space.

Our view toward commodities has begun to improve at the margin. However, we remain out of this asset class given large amounts of excess supply capacity for most commodities around the world. Furthermore, China’s slowing growth continues to limit demand and we don’t believe the correction in commodities has yet reached a point where an allocation is appropriate.