by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an analysis of the recent upward revisions to US GDP data. We then explore several pivotal global developments, including Japan’s potential shift away from long-duration bond issuance, Canada’s concession on US tariffs, and the sell-off in British bank shares. Finally, we conclude with an overview of other essential domestic and international factors shaping the financial landscape.

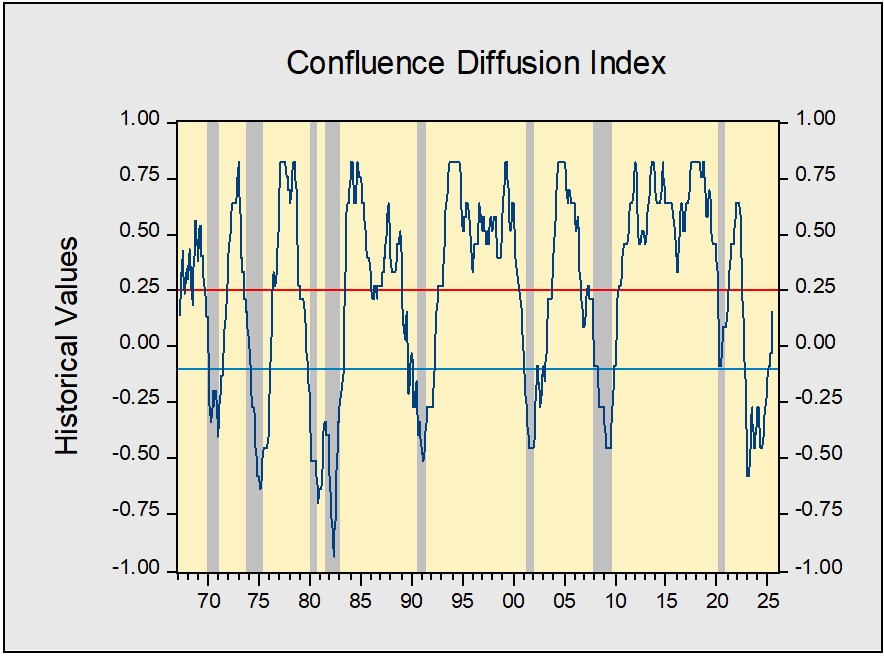

GDP Surprise: The US economy grew even faster than initially thought in the second quarter, with GDP revised up to a robust 3.3% annualized rate. This upgrade was fueled by strong consumer spending, solid net exports, and increased business investment, which more than offset a slight dip in government outlays. Crucially, underlying domestic demand — measured by Final Sales to Private Domestic Purchasers — remained sturdy, growing at a steady pace and signaling that the economy retained its momentum from the start of the year.

- The stronger-than-expected GDP data bolsters the argument that the economy is not in recession. The solid expansion in the second quarter effectively offsets the prior quarter’s contraction, signaling resilience rather than a downward trend. A key driver of this performance was household spending on durable goods, with orders for motor vehicles providing a significant lift to overall sales figures.

- Although the data is positive, it warrants cautious optimism. The labor market’s stagnation, characterized by a hiring freeze amid a lack of layoffs, indicates that firms view the economic softness as transitory. For investors, we believe this environment presents an opportunity to increase risk exposure. We advise focusing on companies with strong profitability and domestic supply chain reliability, which are critical differentiators in the current climate.

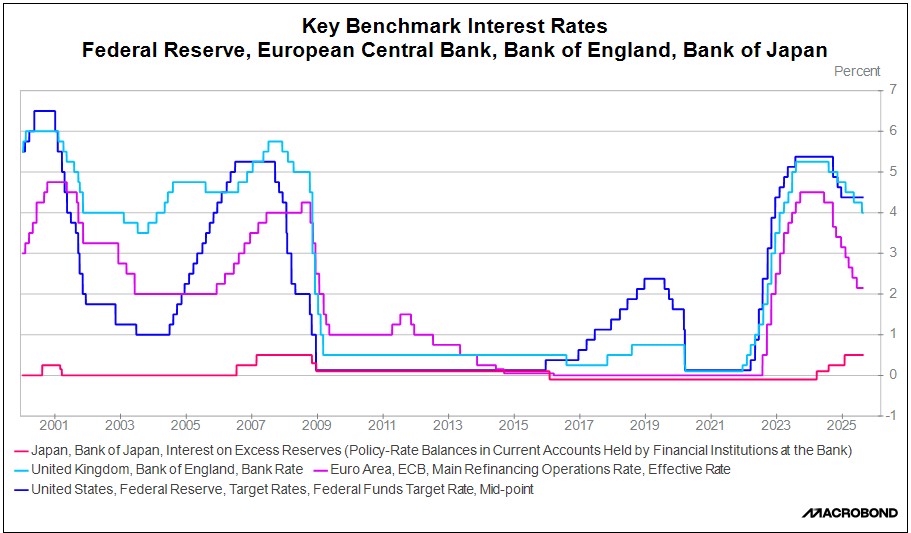

Japan Reducing Long Bond Supply: The Ministry of Finance in Japan has reportedly surveyed primary dealers regarding a potential reduction in the issuance of long-term government bonds. This action is a strategic move to address the upward pressure on domestic interest rates. It comes as the Bank of Japan (BOJ) begins to unwind its extensive quantitative easing program, and the government continues with its own fiscal expansion.

- By reducing the supply of these longer-dated bonds, the Ministry aims to stabilize the bond market and help prevent a sharp increase in government borrowing costs, which have been rising due to weak demand and the BOJ’s reduced market presence.

- This trend is indicative of a deteriorating appetite for debt among bond investors. While we have not yet witnessed a failed auction, the clear pushback from the market is a cause for vigilance. In response, major sovereign debt issuers like Japan, the US, and the UK have indicated a strategic pivot towards shortening the maturity of their debt issuance to accommodate investor demand.

Jumbo Cut in September? Fed Governor Christopher Waller stated he is prepared to cut interest rates aggressively if upcoming jobs data shows further labor market softening. His comments come amid growing market expectations for a September rate cut, fueled by recent downward revisions to payrolls that have raised doubts about the labor market’s strength. This highlights the ongoing tension within the Fed over whether to prioritize its price stability or maximum employment mandates.

Brazil Response: In response to recent US tariffs that imposed duties as high as 50% on Brazilian exports, the administration of President Lula da Silva is preparing retaliatory measures. The Brazilian Chamber of Foreign Trade has been tasked with assessing the tariffs’ economic impact and developing a list of potential countermeasures. The government is scheduled to officially announce this retaliatory investigation later today. The rise in trade tensions between the two countries will likely impact Brazilian equities more than their US counterparts.

Canadian Tariffs: The Canadian government now concedes that it will not secure the complete removal of US tariffs on its exports. This pessimistic outlook follows Canada’s commitment to unilaterally lift its retaliatory tariffs on American goods by September 1, among other concessions made to ease trade tensions. Although the majority of bilateral trade flows freely, persistent US tariffs on Canadian steel continue to inflict economic damage.

Taiwan-US: Two US senators have reignited the debate over America’s commitment to Taiwan. Mississippi Senator Roger Wicker and Nebraska Senator Deb Fischer have voiced strong support for the island’s freedom and its right to self-determination. Their statements come during a fact-finding trip to the region, aimed at assessing the security situation amid heightened military pressure from China, which seeks to assert its control over Taiwan.

UK Banks Under Fire: Shares of British financial services firms are facing selling pressure due to investor concerns over potential tax increases. The government is exploring options to address a 20 billion GBP ($26.9 billion) budget deficit, and a recent think tank proposal to raise taxes on bank profits has fueled fears that the sector will bear a significant burden. This approach signals a potential policy shift, as the governing party appears to be moving away from the idea of a wealth tax to instead concentrate fiscal measures on specific industries.

Taliban-Pakistan: The Taliban has warned of retaliation against Pakistan after airstrikes hit two provinces in Afghanistan. The strikes, which Pakistan is believed to have conducted, threaten to escalate tensions between the two Muslim nations. Pakistan has accused Afghanistan of sheltering militants responsible for recent terrorist attacks on its soil. While the conflict is likely to remain localized, it contributes to the broader instability that has kept global oil markets on edge.