by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment begins with our analysis of concerns over a rise in job cut announcements. Next, we examine what JPMorgan’s involvement in the Argentine bailout reveals about the evolving relationship between the private and public sectors, along with updates on OpenAI seeking a government backstop, the recent drop in Chinese exports, and the potential weakening of new EU regulations. As always, the report includes a comprehensive roundup of key international and domestic data releases.

Layoffs Rising? Market sentiment soured sharply on Thursday following a grim report on the US labor market. According to Challenger, Gray & Christmas, employers announced 153,074 job cuts in October—the highest for the month in over two decades. The report also showed hiring plummeted 35% from the previous year, reinforcing fears of a significant cool-down. With official government data unavailable, investors have reacted sharply to private data as they try to gauge the state of the economy.

- The report detailed the drivers behind the layoffs: cost-cutting was the top-cited reason, followed by artificial intelligence (AI), and general market and economic conditions ranking third. The technology and warehousing industries bore the brunt of the cuts, suggesting companies are actively shedding jobs due to redundancies and overcapacity concerns after a period of rapid pandemic-era expansion and subsequent automation efforts.

- While the massive total of job cut announcements from the Challenger report paints a stark and severe picture of the economy, it represents just one proprietary measure. Other high-frequency data suggests the labor market’s underlying health remains resilient. For instance, the latest state initial jobless claims data, gathered by Bloomberg, indicates that actual reported layoffs are still subdued despite a modest increase from the previous week.

- The recent layoff figures are undoubtedly concerning. However, the pronounced market volatility likely stems less from the data itself and more from the absence of official government benchmarks. This information vacuum forces an overreliance on fragmented proprietary reports, magnifying their impact. We anticipate a return to stability upon the release of comprehensive official data and, barring any major surprises therein, retain a constructive view of the economy’s underlying path.

Bank and Government: JPMorganChase executed purchases of Argentine pesos on behalf of the US Treasury, an action confirmed publicly for the first time by Senator Elizabeth Warren. This revelation confirms the bank’s direct role in a White House initiative to stabilize Argentina’s currency—a move that, in effect, provided a financial backstop for President Javier Milei’s administration. The case highlights a growing trend of the private sector being enlisted as partners in statecraft, blurring the traditional lines between public policy and private commerce.

- Although the specifics of the arrangement are not fully known, reports indicate that the bank’s function was to purchase Argentine pesos and subsequently sell them to the Federal Reserve Bank of New York. JPMorgan was not the only bank involved; Goldman Sachs, Bank of America, Banco Santander, and Citigroup also participated in the $20 billion currency swap lifeline.

- The coordination between the White House and the private sector comes as the government has taken on a more active role in promoting business interests abroad. Prior to the decision to help stabilize the peso, JPMorganChase CEO Jamie Dimon visited the South American nation and signed a lease in the capital as his bank looks to expand its footprint in the region.

- This event highlights the growing overlap between public and private interests as the US seeks to expand its global influence and enhance national security. While this collaboration can benefit firms through government protection for overseas expansion, it could also pave the way for outside political influence in firm decision-making, or at least create the perception of it.

OpenAI Wants US Backing: OpenAI, the creator of ChatGPT, has suggested that the US government provide loan guarantees to backstop its significant infrastructure expansion. The request arises from concerns about how the company will fund its ambitious projects, which represent over $1 trillion in commitments against only roughly $13 billion in annual revenue. While OpenAI clarified that it does not require the assistance to survive, it maintains that such government support would be highly beneficial for its growth.

Financial Plumbing Concerns: Wall Street banks continue to express concerns about funding stress as signs of tightening liquidity in the system appear. These fears are rooted in the sharp rise in short-term funding rates, particularly in the repo market, which has caused strain on the broader financial system. While this liquidity problem currently appears to have subsided, there is growing concern that the Federal Reserve may be forced to intervene to prevent a more severe market dislocation from emerging.

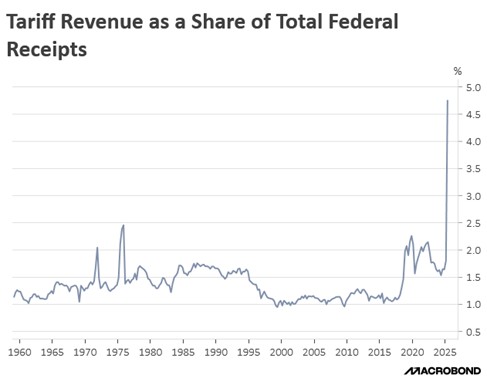

New Critical Minerals: The US Department of the Interior has added several metals, including copper, silver, and metallurgical-grade coal, to its list of “critical minerals,” a move that could pave the way for higher tariffs. This designation means these materials will be included in a Section 232 national security review, which can result in new import levies. The expansion of the list underscores the US government’s growing influence over the domestic commodity market.

Chinese Exports Fall: China’s exports fell unexpectedly last month for the first time since February. The decline suggests the world’s second-largest economy may be feeling the effects of US tariffs imposed in April. This could signal that China is exhausting its alternatives for circumventing those tariffs and may also point to a broader slowdown in global demand. The drop likely points to an economy losing momentum, which could force Beijing to inject fresh stimulus to bolster growth.

EU Regulatory Pullback: In an effort to enhance its global competitiveness, the European Commission is weighing a pause in the implementation of certain digital regulations. The proposal follows significant pressure from a coalition of large technology companies, the US government, and prominent European businesses. By creating a more favorable regulatory environment for tech development, the EU aims to strengthen its position relative to the US and China and attract greater foreign direct investment.