by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Our Comment today opens with the latest on the spiraling of tensions between the U.S. and China. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including news that the U.K. will begin training Ukrainian pilots to fly modern jets and an overview of President Biden’s State of the Union address last night.

China: The commander of U.S. Strategic Command, who oversees the country’s nuclear forces, has formally notified Congress that China now has more launchers for ground-based intercontinental ballistic missiles (ICBMs) than the U.S. does. The Chinese launchers include both mobile vehicles and newly constructed silos that are still sitting empty. The U.S. continues to field many more missiles and nuclear warheads than China, as well as many more bombers and submarines capable of launching strategic nuclear weapons. Nevertheless, the notification will likely prompt increased concerns about China’s military expansion and fuel even more calls to decouple from the country and kneecap its development.

China-U.S. Spy Balloon: Yesterday, the U.S. Navy published photos showing its sailors recovering the remains of the Chinese spy balloon shot down off the South Carolina coast. However, it is still probably too early for any analysis of the debris to have been completed.

- That analysis will aim to establish what information the balloon was designed to gather, how capable it was, and whether it contained any U.S. or allied components. Given today’s strong bipartisan enmity toward China, any threatening findings will likely prompt further bilateral tensions, potentially catching investors in the crossfire.

- In a further sign of how the incident has worsened U.S.-China relations, new reporting says Chinese Defense Minister Wei Fenghe refused to take a secure hotline call from U.S. Defense Secretary Austin immediately after the U.S. downed the balloon on Saturday.

Russia-Ukraine War: As Russian forces continue to ratchet up their new offensive in northeastern Ukraine, President Zelensky is visiting Prime Minister Sunak in London today. Zelensky has scored a British commitment not only for more weapons and equipment, but also for British training of Ukrainian jet fighter pilots. The fighter training will evidently be on British Hawk 2 trainers, but that could be a first step toward getting them up to speed on modern fighters like the U.S. F-16 that Kyiv has been clamoring for.

- Separately, the German government announced yesterday that Germany, Denmark, and the Netherlands together would donate 178 older-generation Leopard 1 tanks to Ukraine.

- Despite being an older version of the powerful and highly modern Leopard 2, the new tanks would be a significant upgrade to what Ukraine already has. The unexpectedly high number of tanks from the three countries will also likely be welcomed by Kyiv.

Turkey: After a three-day sell-off triggered by this week’s big earthquakes, the Turkish stock exchange has suspended trading. So far this week, Turkish stocks have lost approximately 16% of their value, although the central bank has been able to keep the value of the TRY relatively stable. There is no word yet on when stock trading will resume.

United States-European Union: After a series of meetings in Washington yesterday, the German and French economy ministers said that top U.S. officials promised to assuage EU concerns about the $369 billion in subsidies for domestic green technology investments in last year’s Inflation Reduction Act. However, they didn’t secure any concrete proposals beyond an agreement on full transparency over the level of subsidies on offer under the IRA so that Europe can match them if necessary. That will ensure that the subsidies remain an issue between the U.S. and the EU in the coming months.

U.S. Monetary Policy: Fed Chair Powell stated yesterday that January’s surprisingly strong labor market data shows why the fight against inflation will take longer and interest rates will need to go higher than many investors have been expecting. We continue to believe that many investors are erroneously anticipating a quick end to excess inflation and a near-term pivot to lower interest rates before the economy falls into recession.

- As one example that many investors still trust the “Fed put,” risk assets rallied strongly yesterday after an initial dip following Powell’s comments. The market moves suggest that many investors were worried that Powell’s comments might be even more hawkish.

- The jump in U.S. stocks yesterday is being followed by a jump in European stocks today.

U.S. Politics: In his State of the Union address last night, President Biden appealed for a bipartisan approach to the nation’s challenges but also focused on selling the benefits of the various legislative victories he’s had, such as passage of his big bill on infrastructure spending and last year’s Inflation Reduction Act. As we flagged in our Comment yesterday, Biden also offered a number of new proposals, such as quadrupling the 1% tax on stock buybacks to channel more money into capital investment and expanding the $35 cap on monthly insulin costs to those outside the Medicare system.

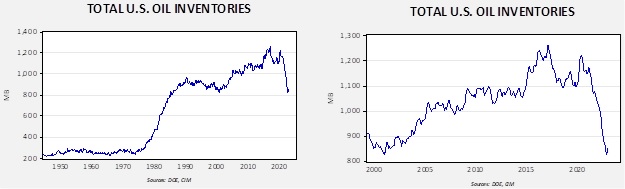

U.S. Energy Market: The Energy Information Administration issued a report showing that U.S. gasoline consumption fell to just 8.78 million barrels per day in 2022, some 6% lower than at the peak before the COVID-19 pandemic. The agency also forecasts that U.S. consumption will continue to decline in 2023 and 2024, reflecting more efficient cars, the growing prevalence of electric vehicles, and work-from-home arrangements following the pandemic.

- Those factors could well drive down the consumption of gasoline far into the future.

- Nevertheless, the decline is likely to be gradual, meaning large amounts of fossil fuels will still be consumed in the U.S. and worldwide. The shortfall in oil and gas investment in recent years is therefore likely to lead to supply shortages and higher prices in the future, which is one key reason we believe commodities will be an attractive asset class once we get through the impending recession.