by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment section opens with a deep dive into the recent drop in gold prices and its stark implications for US-China trade tensions. We then explore the potential pathway to persuading Russia to end the war in Ukraine. Closer to home, a strong earnings season and a landmark AI deal could signal robust market momentum, while in the EU, there is mounting pressure to recalibrate climate strategy. As always, we include a summary of key economic indicators from US and global markets.

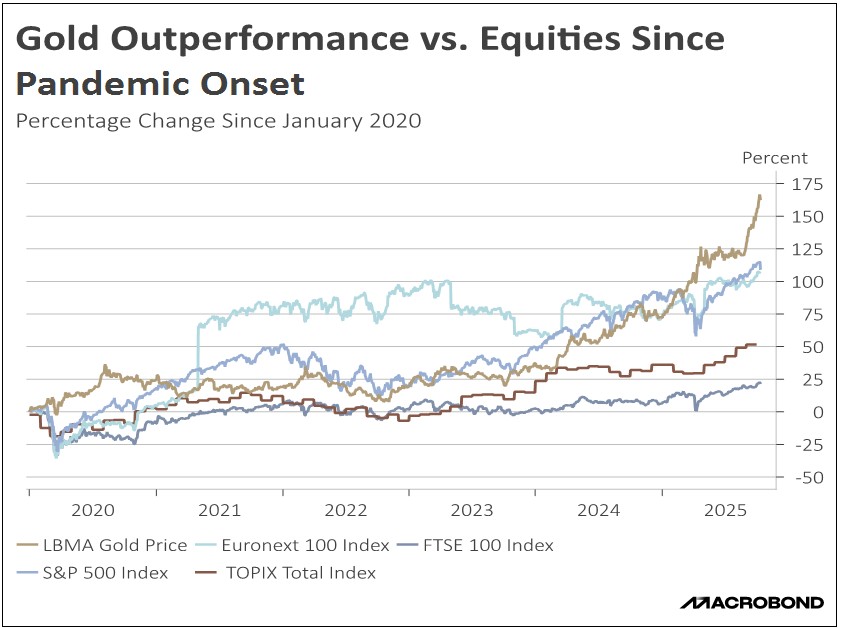

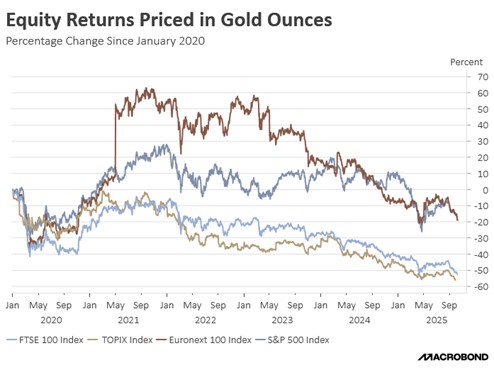

Gold Retreat: Precious metals, including gold and silver, sold off as the de-escalation of US-China trade tensions reduced the appeal of safe-haven assets. This decline was amplified by the post-Diwali lull in Indian demand and widespread concern that the metals were overbought, triggering significant profit-taking. While the retreat from gold and silver signals investors are shifting away from safe havens, the lack of a corresponding surge in equities suggests lingering investor caution.

- The market’s hesitation to embrace riskier assets reflects a standoff-ish posture as investors await for more details about US-China trade negotiations. This hesitation persists despite the White House’s upbeat remarks on Tuesday, expressing confidence in reaching a “fantastic deal.” Yet, skepticism lingers, with no meeting date set and the President Trump implying he will only attend if the talks show real promise of progress.

- The White House has indicated that it will seek a deal that includes provisions on rare earth exports, measures to curb the flow of fentanyl, and the resumption of US soybean purchases. In exchange, Washington could offer tariff relief. There has also been speculation that the US could soften its stance on Taiwan, particularly after the president suggested that Beijing is not currently inclined to pursue an invasion.

- We continue to anticipate a meeting between the two sides at the upcoming ASEAN Summit in Malaysia, ahead of the crucial November 1 tariff deadline. Our base case projects a minimal consensus with a commitment to extend negotiations supported by reciprocal minor concessions. Failure to achieve even this minimal step toward de-escalation, however, would likely serve as a negative catalyst, prompting immediate short-term profit taking across various market sectors.

- That said, a successful meeting yielding a “grand bargain” between the world’s two largest economies would be a highly positive event for markets. We believe this agreement would center on Chinese assurances regarding rare earth exports and a commitment to major purchases of American agricultural products. This outcome would provide a significant boost to both Chinese and US equities, with technology stocks and the US agricultural sector poised for the greatest immediate sectoral benefits.

No Putin Meeting: A high-stakes meeting with Russian President Vladimir Putin in Budapest is now off the table, the White House has confirmed. The decision to halt talks comes after Russia offered no reassurances regarding an end to its invasion of Ukraine, leading the US to conclude that the discussion would be unproductive. This cancellation follows reports of internal US debates, including a recent reversal on sending Tomahawk missiles to Ukraine and rumors of possibly pressing Kyiv for more territorial concessions to secure a deal.

- Two structural factors entrench the conflict’s persistence: a strategic imperative for Putin to obtain a definable victory that legitimizes the invasion’s staggering costs, and the Russian economy’s absorption of war-related production as a key driver of growth. Therefore, the war may be prolonged, as its continuation is directly tied to fulfilling these core strategic and economic objectives.

- While the path to ending the war is challenging, the US retains significant leverage. In addition to sanctions relief, a potent bargaining chip is the unsold, frozen Russian state assets, which could be used as a strategic tool in negotiations. Furthermore, Moscow may be incentivized by the potential for a diplomatic off-ramp, specifically the opportunity to re-establish a closer relationship with the US and secure a pathway for re-engagement with the European Union.

- Recent overtures point to potential avenues for de-escalation. For instance, Moscow has recently floated the idea of an Arctic tunnel connecting Russia and the US across the Bering Strait. On the European side, some speculation persists that the conclusion of the conflict could lead to a significant policy shift in Germany. This includes the possibility that a future German government might reconsider the Nord Stream 2 gas pipeline project.

- While the suspension of talks suggests a pushback on the immediate ceasefire timeline, we maintain an optimistic view that the conflict could be resolved by early 2026, if not sooner. A definitive end to hostilities is expected to be a strong catalyst for European equities. Conversely, the anticipated full resumption of Russian energy (oil, gas, and coal) flows to international markets would likely create significant downward pressure on global commodity prices.

Earnings Season: With only a fraction of S&P 500 companies having reported, the earnings beat rate (the percentage of companies surpassing consensus EPS estimates) this quarter is the highest in over four years. This outcome defies even high initial expectations and suggests better-than-anticipated corporate fundamentals. The primary pillars supporting this profit strength are robust consumer spending, expansive investment in AI technology and infrastructure, and the flow-through effects of ongoing federal deficit spending.

US-India Trade Deal: A pending US-India trade agreement aims to dramatically lower tariffs on Indian goods, cutting them from around 50% to 15-16%. The deal is part of a broader strategic bargain. In return for this tariff relief, India will reduce its reliance on Russian oil and increase imports of American non-GMO corn and soymeal. Successfully concluding this pact would mark a significant diplomatic achievement for the White House, demonstrating its capacity to broker deals that advance both economic and foreign policy objectives.

EU Under Pressure: The United States and Qatar have joined forces to pressure the European Union to revise its proposed climate regulations. The push comes as EU lawmakers debate legislation that would fine companies up to 5% of their global revenue for supply chain practices that harm the environment or violate human rights. Washington has warned that the measure could undermine economic growth and jeopardize the trade agreement reached with the EU in July.

Anthropic and Google: A major rival to OpenAI is negotiating a deal with Google for its cloud computing services. The agreement would grant Anthropic access to Google’s Tensor Processing Units (TPUs), which are specifically designed for machine learning workloads. This move comes as one of its largest suppliers, Amazon, is contending with outages of its cloud services. The deal reinforces an industry trend of heavy spending to build AI supply chain resiliency, while also highlighting the intensifying competition for dominance in AI infrastructure.

Japan Stimulus: Newly appointed Japanese Prime Minister Sanae Takaichi is proposing a targeted economic package to counter rising inflation. The proposal, which aims to mitigate rising costs of living, is believed to center on direct subsidies for winter energy bills and grants to local governments. Deliberately avoiding the broad stimulus spending that has unnerved financial markets, Takaichi’s strategy emphasizes targeted expenditures. However, key questions regarding the package’s total cost and financing have yet to be clarified.