by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with a focus on the president’s new tariffs following the expiration of the August 1 deadline. We then assess major international and domestic developments impacting financial markets, including the ongoing legal challenges to the president’s tariff authority in federal appeals court, and the administration’s expanding campaign to put pressure on monetary policy, which has now extended from Fed Chair Powell to the broader Federal Reserve Board regarding interest rate cuts.

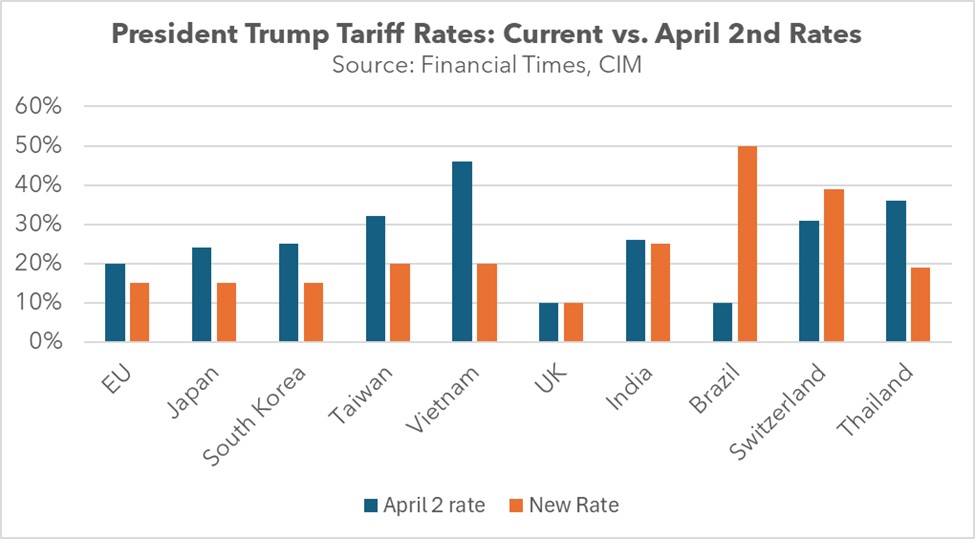

Deadline Passed: New tariff rates have been announced by President Trump for countries that were unable to finalize a deal by the August 1 deadline. Although rates for most nations are still lower than the April 2 levels, Brazil and Switzerland are notable exceptions as both are seeing an increase in their rates. It is worth noting that the new tariffs will not be imposed for seven days.

- While many countries received their new tariff rates, a few notable exceptions were granted extensions. China and Mexico, for instance, received deadline extensions beyond August 1 from the Trump administration as negotiations continue. This suggests that potential trade deals could be close to finalization with these nations. While Canada was hit with 35% tariffs, goods covered under USMCA were excluded.

- On a more positive note, some countries successfully negotiated more favorable terms. Australia, for example, secured a baseline tariff of 10%, a rate comparable to that granted to the UK, another country with a trade surplus with the US. Additionally, Taiwan has stated that it expects its tariff rate to be cut after talks.

- However, the president has established a global baseline tariff rate of 10%, signaling the permanence of this policy. Our view is that these country-specific tariffs are intended to be the president’s primary tool to generate revenue from abroad, which would thereby help fund US spending.

Tariff Court Showdown: The administration’s tariff plans faced a cool reception on Thursday. At the heart of the dispute are the reciprocal tariffs, which the White House defends under the International Emergency Economic Powers Act (IEEPA). During the hearings, judges expressed broad skepticism as the act does not explicitly mention tariffs. Given the high stakes and the challenge to presidential authority, the case is almost certain to reach the Supreme Court, irrespective of the appellate court’s ruling, since the losing side is very likely to appeal.

Fed Board Targeted: President Trump has called on the Federal Reserve Board to take over for Fed Chair Powell if interest rates aren’t lowered at the upcoming policy meeting. This latest demand reflects the president’s ongoing campaign for rate cuts, which he argues would alleviate the government’s debt burden. While the previous meeting saw two dissenting votes against the rate decision, there is no indication that the board has lost confidence in its chair. However, four opposing votes by Fed governors have previously led to a chair’s resignation.

Asian Factory Pessimism: Asian manufacturing sentiment has plummeted due to concerns about Trump’s tariffs. According to the S&P Global Manufacturing PMI, confidence in output among surveyed businesses in the region has fallen to its lowest level since July 2020. While a surge in demand from “tariff front-running” was observed, doubts persist about the ability of these manufacturers to sell to the US market given the new levies.

AI Wariness: Investors are growing wary after Amazon reported weaker-than-expected operating income and cloud revenue, which lagged that of key rivals. The disappointing earnings arrive at a critical juncture, as markets scrutinize whether massive AI investments by tech giants will deliver returns. AI-driven optimism has fueled the market rally for the past three years, but if sentiment sours, a shift in leadership could emerge.

Lower Drug Prices: President Trump has demanded that pharmaceutical companies lower drug prices by September 29. His administration sent letters to 17 major firms with a warning that if they fail to act, the White House will use all available tools to prevent price abuses. This aggressive stance underscores the executive branch’s willingness to leverage its authority — potentially at the expense of corporate interests — in a bid to appeal to populist sentiment.

Eurozone Inflation: The eurozone’s July flash CPI estimate showed prices rose 2.0% year-over-year, broadly stable from the prior month but marginally exceeding the 1.9% consensus forecast. The subdued inflation reading may fuel speculation about further ECB rate cuts, as concerns over slowing growth and elevated debt levels could push the central bank toward more accommodative monetary policy.

Firm Merger & Acquisitions: Dealmaking activity has picked up as investors gain greater clarity on tax and trade policies, according to Ares Management’s CEO. The comments follow a wave of recent takeovers across the railroad, cybersecurity, and industrial sectors. This trend suggests that when investors have more predictable policy outlooks, they become increasingly willing to assume additional risk.

No Term Limit: El Salvador’s legislative assembly has voted to abolish presidential term limits, clearing the path for Nayib Bukele to potentially remain in power indefinitely. This consolidation of executive authority follows a regional pattern where leaders have eroded democratic institutions in the name of combating crime. Notably, Latin America has a complex history with strongman leaders, and while they are often politically controversial, their regimes have at times maintained relative stability for financial markets.