Daily Comment (September 6, 2017)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EDT] Financial markets are easing off the flight from risk exhibited yesterday. There wasn’t a lot of breaking news overnight, but there are currently several significant news items. Here’s a recap:

Hurricane Irma: There are three tropical events in the Atlantic but Irma is the current focus of attention. It is a massive Category 5 storm that is presently hitting the Caribbean islands. Yesterday, a majority of the computer models were showing the storm taking a northward hook into Florida by the weekend, but there were a couple of models that suggested the turn may occur late enough for the storm to enter the Gulf of Mexico. If the path continued west, Texas and Louisiana might be hit again by a major storm. However, there is universal agreement among the models this morning that Irma is going to move straight up the Florida peninsula by Monday. The cold front that moved across St. Louis on Monday will steer the storm northward. As we have covered energy since 1989, we do know that computer models are not perfect; if the cold front stalls, a more western drift is possible. But, for now, it appears that the Sunshine State will be the target on the U.S. mainland.

This will be the second major storm to strike the U.S. this hurricane season. The need for emergency government spending should end any uncertainty surrounding the debt ceiling passage, at least in the short run. However, this issue may return by late December. Interestingly enough, financial markets are not convinced that the hurricanes will force a debt ceiling reconciliation.

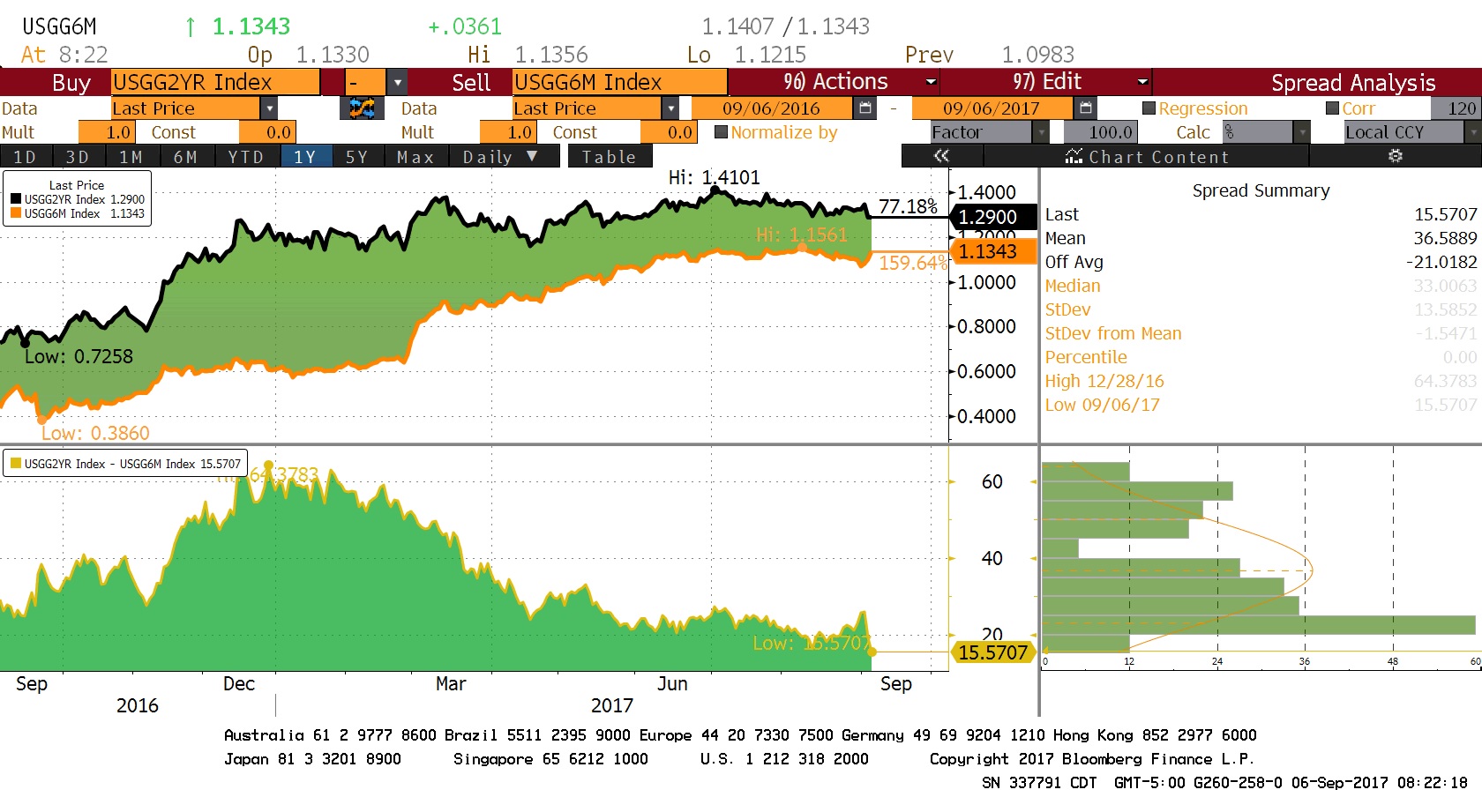

This chart shows the six-month T-bill rate along with the two-year T-note rate. Note that the spread has significantly narrowed recently as bill rates increased while two-year rates fell. We suspect that fears of a short-term disruption related to the debt ceiling are boosting bill yields, while the feared negative impact on the economy weighs on the potential for future Fed rate hikes, easing the note rate. We would expect this spread to widen again if our analysis is correct and the hurricanes force a clean debt ceiling rise.

When doves cry: Fed Governor Brainard and Minneapolis FRB President Kashkari gave talks yesterday. Both are doves; the latter has dissented from recent rate hikes and the former has expressed deep caution about moving rates higher too quickly. Kashkari said yesterday that the recent hikes may have already adversely affected the economy. We find this argument difficult to support; GDP growth is running around 3% and the current Atlanta FRB GDPNow forecast for Q3 GDP is 3.2%, incorporating the somewhat weaker than expected employment data. Maybe Kashkari will be right in the future but, for now, the impact of recent hikes doesn’t appear onerous. Brainard’s comments appear to be on more solid theoretical footing. She suggests that current low inflation isn’t just a series of idiosyncratic events but is, in fact, structural in nature. In other words, inflation is coming down on a secular basis, and running monetary policy on the premise that price levels will normalize will likely lead to overly tight policy and invite a recession. Essentially, Brainard is arguing that inflation expectations are becoming unanchored to the downside and that monetary policy should take this idea into account and perhaps lean against this trend.[1] Our economic work suggests that the central bank has little impact on inflation; instead, inflation is the intersection of aggregate supply and demand. And, in a globalized and deregulated world, the aggregate supply curve is nearly horizontal, meaning that increased demand has little impact on inflation. However, the central bank does have an impact on inflation expectations; if it appears too accommodative, it can spook businesses and households into precautionary spending. Simply put, if a household or business fears future price increases, it “saves” by holding inventory, further boosting price levels. The central bank isn’t the only factor in inflation expectations, though. One’s experience of inflation over a 10- to 20-year time frame also affects inflation expectations. Essentially, the Fed now has the opposite problem it faced in the 1970s. At that time, inflation expectations were elevated and the Volcker Fed had to act aggressively to convince households and firms that it would take steps to bring down inflation. Now, expectations of continued low inflation have become so entrenched that the Fed faces the need to convince economic actors that it won’t snuff out the economy prematurely.

The key question is whether or not Brainard’s position will sway her fellow FOMC members. It’s probably unlikely. Although it’s too simplistic to say that age affects the process of monetary policy, in fact, a significant number of influential members, including the chair and vice chair, came of age during the 1970s and are probably affected by that experience. It is no coincidence that Brainard and Kashkari are among the youngest members of the FOMC. Perhaps the only way the Fed becomes comfortable with persistently easy policy is through generational change. It is true that policy has been persistently accommodative, but it is also true that the preponderance of policymakers at the Fed appear to view current policy as an emergency measure and not a structural shift. Brainard is arguing for a structural shift. We doubt her argument will carry the day at the current Fed but it may in the future.

DACA: We haven’t commented on this issue yet because our focus is on financial markets. However, now that action is being taken, this issue will begin to affect the financial markets. DACA now becomes another distraction for a Congress that has lots of them. So, instead of working on tax reform or infrastructure spending or a budget, Congress will have to deal with this issue. Given the deeply divided nature of Congress, it is hard to see how they can address such a contentious problem and thus working on DACA will delay other agenda items.

[1] We recently discussed the issue of weak wage growth and noted that while nominal wage growth is running well below where it historically should be based on labor market conditions, real wage growth is actually consistent with current labor market conditions. https://www.confluenceinvestment.com/asset-allocation-weekly-july-14-2017/