Daily Comment (September 13, 2021)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] | PDF

Good morning and happy Monday! A lot is going on in the world today as we turn toward autumn. After a soft week, equities are lifting this morning. We begin with comments on what is shaping up to be a turbulent month. There is an abundance of election news around the world, and we take a look at several races. Crypto news comes next, followed by our coverage of China. Next up is economic and policy news and our international roundup. We conclude with a pandemic update.

We used to like September: School resumes, the NFL returns, the baseball season winds down with at least a couple of races for the playoffs. Summer weather gradually cools, and temperatures become less oppressive. The hint of autumn comes with the equinox (September 22 for those keeping score). However, this September could be volatile. The nuts and bolts of the budget are being introduced in Congress. As we noted in the latest WEU, energy companies are trying to prevent, or at least modify, taxes directed at them on carbon and methane. Capital gains taxes are almost certain to rise, but that’s not all being considered. Increases to corporate taxes are also on the agenda, and maybe special taxes on stock buybacks. It is clear that capital is being targeted. Equity markets usually don’t discount these sorts of events very well. The market didn’t anticipate the Trump tax cuts, for example. Thus, we probably won’t see the market take the taxes into account until they are passed. This position makes sense; tax law is very complicated. It’s better not to move until you know exactly what the final outcome is, but the budget will hang over the market for the next several weeks. We will continue to monitor this situation as it unfolds.

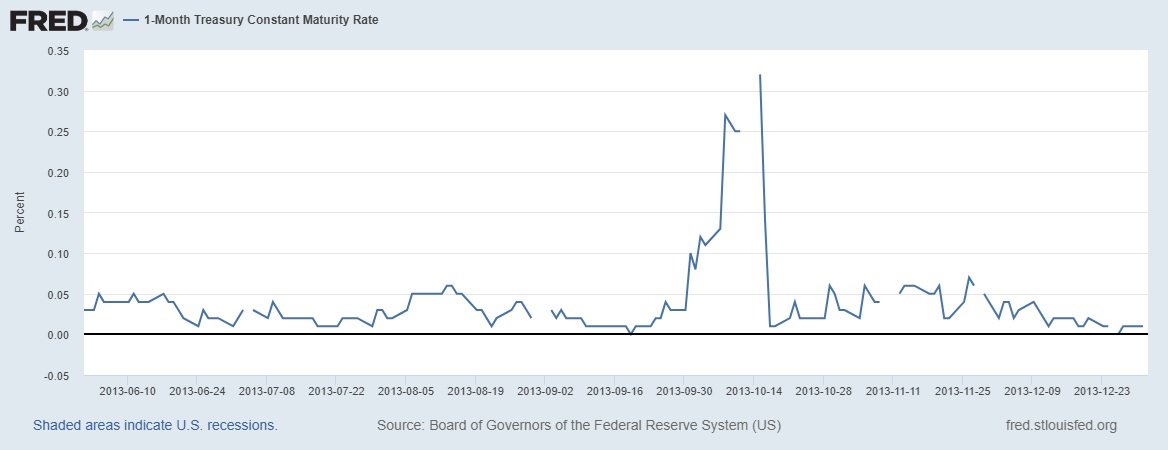

But wait…there’s more! The debt ceiling issue is coming at the same time we are dealing with the budget. In reality, the debt ceiling is a formality. The spending and borrowing have already occurred, but minority parties or the party out of the White House can use the debt ceiling as leverage. This time around, the Democrats who control Congress could simply put the increase into the reconciliation bill and pass it on a party-line vote. However, that creates a campaign issue for the midterms, and it already appears that a change in control is probable. So, the Speaker wants to force a vote on the idea that the GOP leadership won’t vote to shut down the government. Both sides look dug in, which likely means a crisis is in the offing. In the autumn of 2013, when we had similar circumstances, we saw a short-term spike in T-bill rates.

In 2013, the combination of a government shutdown and a new Fed Chair led to a spike in short-dated Treasuries. Although the Fed’s lending facilities in place today would likely prevent significant fallout, there is a risk of short-term volatility in the money markets. The bottom line is that the next eight weeks could be rocky. We don’t think this situation will necessarily require defensive action in portfolios, but we are monitoring the situation closely.

Elections! We have been keeping close tabs on the German elections, but that isn’t the only ones underway. There are others of note.

- Norway is holding elections today, and it appears a center-left party will take control. Although the leadership of the Labor party isn’t calling for an immediate end to oil exploration, the Greens and the Socialist Left, the latter a likely member of the emerging coalition, have made calls for this outcome. In addition, it is possible Labor will need the support of the Greens to form a government. We don’t anticipate an immediate end to Norway’s oil production, but once exploration ends, output levels will decline. What is happening in Norway is consistent with our position that oil prices will tend to be stronger, due to supply fears. Oil companies will likely not perform as well as the commodity.

- Argentina held primary votes yesterday to determine who contests national elections on November 14. Polling suggests the Peronists will lose some of their dominance of the legislature.

- California holds its governor recall election tomorrow.

- Germany held another debate before its upcoming elections. By all accounts, the SDP’s Scholz won the event, increasing the odds of a change in government this month. For the most part, Scholz is the best-looking candidate in a weak field. The CDU’s Laschet appears poised to lose an election he should not have lost. At the same time, it is not unusual that a strong leader prevents the rise of rivals, and when she steps down, there are no adequate replacements.

Crypto: The BIS wants CBDC, and regulators are pushing against cryptocurrencies.

- Late last week, Benoît Cœuré, currently with the BIS but previously an official with the ECB, said that central banks must move “quickly” to develop digital currencies to offset the threat from decentralized finance and stablecoins. Cœuré is leading the BIS research effort on CBDC. He sees stablecoins as a competitor to sovereign currencies. It may also be a source of financial instability that the central banks could be impotent to respond to a funding crisis in this area.

- Regulators are becoming increasingly concerned about decentralized finance lending activities tied to cryptocurrencies. One problem is that if there is a run on these assets, it isn’t clear how central banks could intervene. If this lending has infiltrated the traditional banking system, the potential for a financial crisis becomes elevated.

- A couple of years ago, Facebook (FB, USD, 378.69) tried to roll out a cryptocurrency dubbed “libra.” The program really didn’t get off the ground, but that didn’t kill the project. The new coin is called “diem.” Facebook and the other collaborators on the project wanted to release the coin last year, but not much has occurred yet. The coin is a permissioned blockchain, meaning there is a centralized control regarding who can use the system. Bitcoin, in comparison, is permissionless, meaning anyone can use it. Regulators are pushing back on the release of this currency.

- South Korea has been a hotbed of crypto activity. As we are seeing elsewhere, regulators are cracking down in Seoul, too. By September 24, the government will require all foreign and local exchanges to register as trading platforms. Approximately two-thirds of the local operators appear unable to meet the regulatory standard. If they close, about 42 local “kimchi coins,” the South Korean won-related crypto coins, could be eliminated. These are said to represent 90% of trading in crypto in South Korea. Investors (or more properly, punters) are finding they can’t cash out these altcoins. If they can’t, it is estimated that $2.6 billion may be lost.

China: We are still trying to determine what common prosperity means, and new tariffs on China may be in the works.

- A recent commentary in China over the regulatory crackdown continues to paint a less-than-clear picture about the direction of policy in China. Li Guangman, the author of a recent editorial calling for a wholesale rejection of Western values and the curtailment of capitalist activities, is on one side of the debate. We note that his essay on this topic remains available online in China, which would suggest it hasn’t been rejected by the leadership of the CPC. Other voices have called for moderation, fearing a wholesale rejection of markets will cripple China’s economy. Our take is that General Secretary Xi is determined to bring every part of Chinese society under the control of the CPC, including the market economy. Much of the crackdown is on leaders in industry and culture. Still, there is a degree of uncertainty that will only become clear with time; no one knows how far Xi intends to take this program. For those involved in China, this uncertainty is difficult to manage and has led some to reduce their exposure. Reducing exposure is manageable for financial investment; for direct investment, the options are less attractive.

- Chinese regulators have indicated they want to separate Alipay, the loan app of Jack Ma’s Ant Group (BABA, USD, 168.10), from the rest of the company. Alipay is a prodigious source of data on consumers. It is likely the reason regulators want to pull it away from Ant so Beijing can access Alipay’s data.

- The Biden administration is investigating Beijing’s industrial subsidies to determine whether government support gives these firms an unfair advantage. If the analysis finds it does, countervailing tariffs might be implemented. The White House has kept most of the Trump-era tariffs in place, and now it appears that more may be added.

- We have documented the travails of Evergrande Group (UGRNF, USD, 0.45) in recent weeks. It appears that some degree of contagion is developing, as the bonds of other property developers are plunging. Dollar bonds of Fantasia Holdings (1777, HKD, 0.65) and Guangzhou R&F Properties (2777, HKD, 6.33) have slipped under 60 cents per dollar, pushing yields to around 40%. For years, Beijing didn’t allow companies to default. Banks were encouraged to perpetually extended credit. With the potential of default looming, it remains to be seen if regulators will simply allow these firms to fail and bear the consequences.

- The Biden administration is moving toward allowing a name change in Taiwan’s representative office in Washington. It is currently referred to as the “Taipei Economic and Cultural Representative Office.” The proposal is to change the name to the “Taiwan Representative Office.” This change gives the impression that Taiwan is a separate sovereign. Lithuania recently did something similar, which Beijing didn’t take well. China opposes the move. Coming so soon after the Biden/Xi call, this action suggests a deliberate escalation of tensions.

Economics and policy: Tax proposals are out, a couple of regional FRB presidents are in hot water, and manufactured homes are becoming popular.

- As noted above, we are starting to see tax proposals from the $3.5 trillion budget. Several of the measures proposed are controversial, and we doubt all will be passed. Some missing elements are notable. There are no changes to the estate tax in the linked proposal, for example. Passing this budget will still be tenuous; moderate Democrats remain opposed, and given the slim majorities in Congress, it will be hard to make it all work. We continue to expect something to get done, but probably less than what is currently on paper.

- Dallas FRB President Kaplan and Boston FRB President Rosengren are apparently active traders in their own accounts. This revelation has led to concerns that they may be using information from their role on the FOMC for their benefit. Although neither appears to have violated regulations, the conduct raises questions. Both have indicated they will sell their individual holdings and invest in broad indexes going forward to avoid the appearance of impropriety. This news may turn out to be nothing. However, progressives have eyed the role of the regional bank presidents with concern for a while. Regional bank presidents are appointed by their regional bank boards, which are usually populated with local business leaders. None are vetted by Congress. Voting patterns show a clear skew towards hawkishness. Don’t be surprised if Congressional progressives use this event to gain influence on the selection of a president, potentially removing hawks from the FOMC.

- Although LIBOR isn’t dead quite yet, regulators continue to press for its demise. In advance of the expected conclusion of the rate by year’s end, CLO managers are rushing to do deals while the rate is still available. This seems a bit silly to us. If LIBOR goes away, some other rate must be used. We note that some loan language says that if LIBOR becomes unavailable, the rate is fixed at the last known rate.

- The EPA is moving to block the development of the Pebble Mine project in Alaska. Although there are understandable environmental objections, it is also true that the move away from fossil fuels is essentially a change from oil and gas to metals. Making areas unavailable for development simply drives the prices of metals higher.

- As the courts have ended the eviction moratorium, evictions are starting to occur. This is despite the fact that billions of dollars of rental assistance are available. In the end, the program was a massive failure and shows that money alone won’t facilitate a government program. Planning and bureaucracy are also necessary.

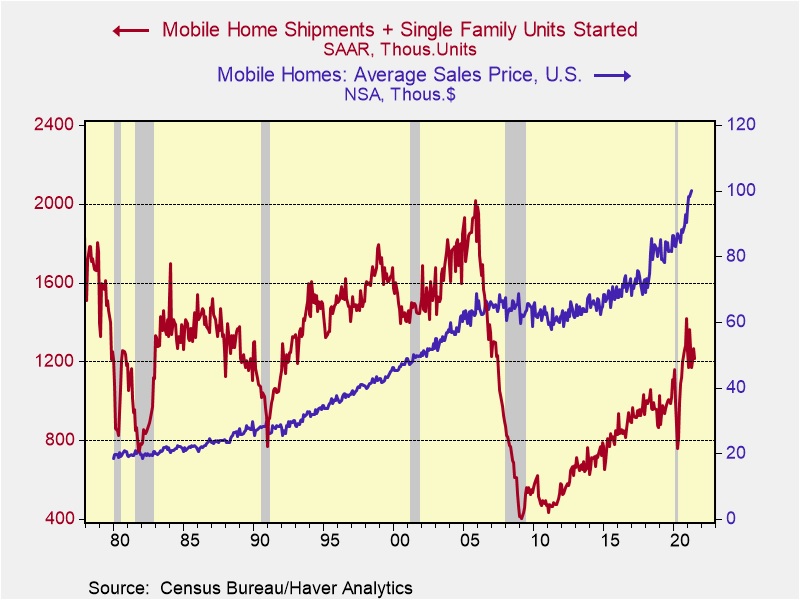

- As home prices soar, manufactured homes, perhaps the lowest end of owned housing, are starting to perk up.

At the peak of the housing crisis, shipments and starts reached 2.0 million units. As housing crashed, that number collapsed too, falling to 400,000. When home prices began to recover, so did manufacturing and shipments, although levels remain below earlier levels. The above chart shows prices moving up rapidly, and manufacturing and shipments are rising, although below levels one would expect given price levels. It is likely that supply chain problems are affecting this industry as well. Part of the problem is that local governments have used zoning to prevent the establishment of manufactured home parks. At the same time, these homes are significantly cheaper than on-site homes and could solve the housing deficit.

- One surprise in this recovery is the robust rise in earnings. Earnings usually rise in recoveries, but current S&P earnings as a percent of GDP are 7.8%, well above the previous highs of 6.5%. A large part of that strength has been the ability of firms to pass higher costs on to consumers. However, at some point, societal pressure will start to affect the ability of firms to move higher costs to consumers, which will adversely affect margins. We are seeing the first industry reaction on this front. The world’s third largest shipper, CMA CGM announced it is capping shipping rates for the next five months. The top six container ship operators control 75% of all ship space, giving them remarkable pricing power.

- On a related note, the White House has a new council on competition; it held its first meeting last week. The narrative being built is that inflation is caused by industry concentration. So, antitrust becomes an anti-inflation policy.

- UPS (UPS, USD, 193.26) says the pandemic will permanently change logistics, reducing globalization and leading to increased regionalization.

- At the same time, BMW (BMWYY, USD, 31.10) and Daimler (DMLRY, USD, 20.26) announced over the weekend that they intend to keep prices high. Ford (F, USD, 12.68) has indicated similar sentiments. Both will likely do so by holding less inventory. The pandemic’s disruption of supply chains has proven to automakers that they really don’t need dealer lots loaded with cars. A casual drive-by of car lots shows a lot of asphalt and little stock. This may become the future, one of the permanent changes from the pandemic. Car buyers are becoming more comfortable with buying online and seem to be less concerned about immediate delivery. Car dealers are rapidly consolidating in front of this trend. For years, dealers were protected by a web of state laws that prevented the auto companies from selling direct to consumers. The dealers themselves began to see their business as providing service after the sale, and thus, the walls of direct-to-consumer sales, or the need for inventory, are rapidly weakening. The days of haggling over a car may be coming to a close. That isn’t necessarily good news for consumers.

International roundup: Will the Eurobond become a permanent feature, and PM Johnson hikes taxes.

- A report issued last week is attempting to frame the relationship between the Russian government hackers operating from that nation. Although the Kremlin has ties to these groups, the relationship is distant enough to give Moscow plausible deniability.

- North Korea has tested a new long-range cruise missile.

- Russia and Belarus are planning joint military exercises. This decision raises fears in the West as the two nations have moved steadily to unify.

- Ireland, which is something of a tax haven for big tech, is apparently failing to enforce EU laws on tech firms.

COVID-19: The number of reported cases is 224,712,819, with 4,632,043 fatalities. In the U.S., there are 40,956,417 confirmed cases with 659,975 deaths. For illustration purposes, the FT has created an interactive chart that allows one to compare cases across nations using similar scaling metrics. The FT has also issued an economic tracker that looks across countries with high-frequency data on various factors. The CDC reports that 456,755,755 doses of the vaccine have been distributed, with 380,241,903 doses injected. The number receiving at least one dose is 209,437,152, while the number receiving second doses, which would grant the highest level of immunity, is 178,692,875. For the population older than 18, 64.9% of the population has been vaccinated. The FT has a page on global vaccine distribution.

- The administration is steadily moving toward vaccine mandates. Opposition to this action is elevated; it should be remembered that opposition to mandated vaccination is nothing new. Yet, it should be recognized that the courts usually favor the implementation of mandates.

- Restaurants are closing dining rooms again as infections rise.

- Brazil is the latest country to move away from China’s vaccines. This is despite Beijing’s attempt to distribute its vaccines in the emerging and frontier worlds.

- The U.S. currently ranks sixth among the G-7 nations for vaccine distribution; with Japan ramping up its program, the U.S. will likely fall to seventh.

- Recent studies indicate that those infected with the Delta variant are 11 times more likely to die from the disease if unvaccinated. The highly infectious Delta variant is adversely affecting working-age populations.

- Eventually, through vaccination and natural post-infection immunity, COVID-19 will probably become a seasonal infection.