Daily Comment (October 11, 2016)

by Bill O’Grady and Kaisa Stucke

[Posted: 9:30 AM EDT] Global equity markets are mixed this morning. The EuroStoxx 50 is trading higher by 0.4% from the last close. In Asia, the MSCI Asia Apex 50 closed lower by 1.7% from the prior close. Chinese markets were higher, with the Shanghai Composite moving up by 0.6% and the Shenzhen index moving up by 0.5%. U.S. equity futures are signaling a lower opening.

Financial markets were mostly quiet overnight. We are seeing some modest weakness in oil prices. Oil rose yesterday, bolstered by comments from Russian President Putin who indicated that Russia would consider production cuts if OPEC reduced output. This morning, the Russian Energy Minister, Alexander Novak, indicated that Russia was only considering a freeze on production, not a cutback. The head of the state controlled Rosneft (MCX: ROSN, RUB 362.40), Igor Sechin, a key oligarch, indicated his company would not reduce output. Rosneft controls 40% of Russia’s output, which hit a new national record recently at 11.1 mbpd. In fact, analysts project Russia will increase output next year by 1.6%. Russia has a history of promising to cooperate with OPEC but failing to follow through.

The WSJ reports that Libya, Iran and Nigeria could add as much as 0.7 mbpd of production in the coming months. The IEA indicated that OPEC output recently reached 33.6 mbpd, a new record. Thus, even the advertised cut would only reduce output to 33.1 mbpd, and if the aforementioned nations hit their targets, OPEC output would actually rise to 33.8 mbpd. We believe the talk about cutting output is driven by a form of Saudi “window dressing” as it prepares for a global bond issue and the Saudi Aramco IPO in 2018. Given the run up in oil prices, any disappointment could lead to a sharp selloff in the near term.

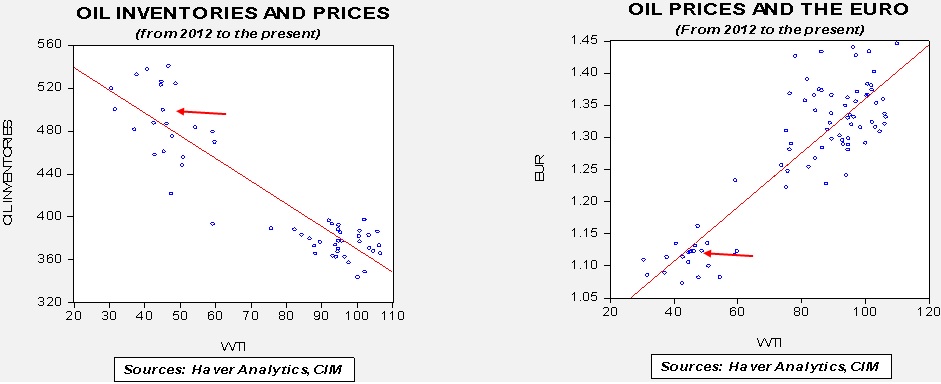

On the topic of oil, there are two other side notes of interest. The DOE, for some unknown reason, has decided to exclude a category of oil called “lease stocks” which is oil in the process of moving to pipelines, railcars or trucks on their way to refineries or tank farms. In reality, it’s still oil and will eventually become part of the inventory number, but the change is material—lease stocks represent about 31 million barrels (mb) which will be cut from the inventory number this week. Thus, on Wednesday, expect to see a massive draw in crude oil. In reality, any number less than 31 mb will actually be a build in oil inventories. Why did the government do this? Strictly speaking, lease stocks are not available for current use and thus are not actually accessible. On the other hand, the oil is available in short order and so excluding it now doesn’t necessarily make much sense. The weekly data won’t contain it, although once we get past this week, the weekly changes should be consistent with the data that have the lease stocks included. It appears that lease stocks generally run between 31 to 33 mb. They probably should be considered like base gas in the natural gas inventory numbers; base gas pressurizes storage wells and remains mostly stable, although we have seen circumstances where storage operators tap base gas when supplies are unusually tight. The bottom line…don’t be shocked to see a massive drop in stockpiles this week.

Second, we are seeing a steady rise in the dollar. A strengthening dollar is generally bearish for commodities, including oil. The longer this rally in the dollar extends, the greater the odds of an oil correction. Based on a $1.1100 €/$ exchange rate, fair value for oil is $46.49. Each penny drop in the exchange rate cuts the fair value for oil prices by $2.33.

We did see a rather sharp selloff in the South African rand after news broke that the well-respected Finance Minister Pravin Gordhan was summoned to appear in court over fraud allegations. According to reports, the fraud stems from his role as head of South Africa’s tax authority a decade ago. Gordhan and President Zuma have been at odds for some time over control of the country’s state finances. Zuma tried to fire him in the past but was forced to relent due to financial market volatility. We suspect these charges are a power grab by the president.

{kind=link}