Daily Comment (October 9, 2023)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Good morning. Financial markets have been roiled by events in the Middle East, which we will discuss. We are seeing market reactions typical with such geopolitical events, such as a stronger dollar, higher oil prices, a surge in gold, and a decline in equities. However, we have seen most of these markets correct since their most extreme levels of the overnight session. As a reminder, this is a bank holiday, so cash Treasury trading is closed and there won’t be any government data releases.

In today’s Comment, we start our coverage with the Hamas attack and our take on the event. Up next is our international overview, and then we look at economic news.

The Second Yom Kippur War: Nearly fifty years ago, Egypt and Syria, along with other Arab states, launched a surprise attack on Israel. After initial successes, Israel halted the Arab offensive and counterattacked. However, the war did nearly bring the U.S. and USSR into a direct confrontation, and a major side effect of the conflict was the first unveiling of the Arab OPEC oil weapon.

This attack was a surprise as well. Hamas fighters launched a multipronged attack on several towns surrounding the Gaza Strip. The attack appeared to catch Israel completely off guard. Although the situation remains fluid, it appears that over 100 Israelis are being held hostage and over 600 Israelis have died in the assault, with the total death toll exceeding 1,000. It is reported that Americans and Europeans are also being held or have died in the assault. Israel appears to be preparing for a major assault on Hamas as it has called up 300k reservists. The towns captured by Hamas are being retaken. The Gaza Strip is under siege, and their utilities have been cut off. Given that the situation is continuing to evolve, we won’t try to report the latest news, but instead, we will note our observations of the event.

A failure of intelligence: Israel’s model of managing the Palestinian areas was to isolate them with walls and checkpoints, regulate the economies of the Palestinian controlled West Bank and Gaza Strip, and use a deep intelligence network to snuff out unrest and potential attacks. The Israeli government had mostly given up on occupation, as occupying Gaza was difficult, and so isolating and controlling was seen as a better solution. This attack was broad and sophisticated. Not only were there a large number of Hamas fighters involved, but there were also large caches of weapons that had been accumulated and stored. The fact that Hamas was able to put this offensive together without losing operational security is remarkable. Coupled with this intelligence failure was the relatively slow response to the attack by the military and the government. How did Hamas pull this off? It seems to have done so by persistently signaling that the Hamas leadership had no interest in any sort of confrontation with Israel. Essentially, Israeli intelligence fell victim to “narrative capture,” which is when analysts become so convinced of a narrative that they ignore evidence that contradicts the accepted wisdom.

Israel and the U.S. respond: PM Netanyahu has declared a state of war on Hamas and the Israeli government has approved “significant military steps.” The U.S. announced that the USS Gerald Ford carrier group will move to the Eastern Mediterranean. The group was already conducting exercises with the Italian Navy. The U.S. is reviewing the sending of additional assistance to Israel. The large number of hostages taken by Hamas will be difficult to manage.

The conflict could widen: There have been reports of rocket attacks in northern Israel, likely carried out by Hezbollah. As the U.S. moves to support Israel, we will be watching to see if Iran or other regional powers, such as Turkey, try to resupply Hamas. While a regional conflict is a low-probability event, when something like this occurs, there is still a chance for expansion. For example, we note that China is now calling for a Palestinian state, and although we doubt Beijing has the ability to project power into the region, a broader proxy conflict could emerge if outside powers begin taking sides. At the same time, China’s tone-deaf response to the Hamas attack on Israeli civilians will likely fall flat with parties in the region. In addition, given that Iran benefits from this conflict (see next point), Israel may decide to directly retaliate against Tehran.

The role of Iran is a key to whether this conflict expands: There appears to be broad evidence of Iranian involvement. The WSJ is reporting that the Islamic Revolutionary Guard Corps was deeply involved in the planning of the attack and approved the operation. Other sources corroborate this assertion. Iran claims it was not involved. We also note that the Biden administration is clearly trying to avoid tying the operation to Iran. As we have discussed in our Weekly Energy Update, the Biden administration has been trying to resurrect the Iran nuclear agreement (JCPOA) since coming into office. Its most recent decision to unfreeze Iranian assets for hostages will be politically difficult to manage. SoS Blinken has indicated that the $6.0 billion of assets were not used for Hamas. Although that might be technically true, the political optics are not favorable. The ongoing investigation of Robert Malley raises concerns that Iran has penetrated the administration. The initial reaction of the Biden administration appears to be to “slow walk” the issue of Iranian involvement. However, that stance will be difficult to maintain, as there appears to be sufficient evidence to point to Iranian involvement, and thus, some sort of retaliation is likely.

The Israeli/Saudi normalization is in peril: Saudi Arabia and Israel, supported by the U.S., have been in talks with the intent to normalize relations. Riyadh’s stipulations are major (formal U.S. security guarantee, nuclear power transfer, peace in Palestine), which has made a deal difficult to achieve, but, as we have noted in our Weekly Energy Update, progress was being made. However, a deal now looks unlikely. Although we think the timing of this assault was to coincide with Yom Kippur, the fact that the hostilities will likely scuttle normalization is a major benefit for Iran. Thus, the attack coming when talks were making progress suggests possible coordination with Iran.

Market ramifications: Here is what we expect from markets:

Oil prices: After running up to just over $95 per barrel, WTI has endured a stiff correction, likely on fears that rising interest rates would hurt the global economy and weaken demand. However, there was also a chance that a successful Israeli/Saudi normalization could have encouraged Riyadh to boost production as part of the contribution to the deal with Washington. Saudi Arabia has 2.0 mbpd of excess capacity, and therefore represents the most bearish factor to the market. Since the attacks are likely to end or dramatically postpone normalization, we don’t see any other reason why the Saudis would lift output. In fact, if Iran is implicated, we could see actions by the West to curtail Iranian oil flows. In addition, given the fact that the U.S. SPR has already been aggressively tapped, it will be risky to authorize another drawdown. If there is a crackdown on Iranian oil shipments, it is possible that the Saudis will offset those barrels, but, barring a significant economic slowdown, this event will likely put a floor under oil prices at a minimum and could lead to higher prices.

The dollar: If we are right on oil prices, the dollar should rally too. As we noted in our June 12 Bi-Weekly Geopolitical Report, as the U.S. has shifted from a petroleum importer to exporter, America’s terms of trade have flipped as well. Higher oil prices lead to an improvement in the terms of trade and thus a stronger dollar. In addition, when crises hit, it is normal for the dollar to appreciate.

Treasuries: Usually, such events lead to the safety buying of Treasuries. We are seeing some of that this morning, but given the other concerns surrounding this market, the rally is unlikely to persist.

Equities: Equities are risk assets and events such as this raise risk perceptions. Thus, it’s a bearish factor for stocks, at least in the short term.

Economic Roundup: Labor actions continue, Boomers support the economy, and we continue to watch the bond market.

- Health care workers in California have returned to work without a contract, but given the state of negotiations, labor action might return. On the other hand, the UAW is expanding its strike to Mack Trucks (VLVLY, $20.58) after workers rejected the company’s offer.

- One of the reasons consumption is holding up so well is due to the spending of older Americans. As the U.S. population ages, more households are living off their accumulated assets and Social Security. This spending is less sensitive to the job market and is turning out to be a surprising source of support for the economy.

- In the 1980s, there were concerns about the size of deficits and the market’s ability to absorb the borrowing. The market did clear, but at rates much higher than what we have seen for the past two decades. There are renewed fears that the market won’t easily absorb the wave of borrowing that the Treasury is planning, and these fears have been a factor behind the recent rise in longer-duration yields.

- Texas cities are reporting high numbers of office vacancies. It isn’t work-from-home that is the problem, but overbuilding. Although this is bad news for real estate owners, it does indicate that a strong Texas economy won’t be adversely affected by rising rents.

- One of the surprises of this rate hiking cycle has been the tame behavior of credit spreads. Normally, tighter monetary policy leads to spikes in credit spreads. What appears to be happening is that private credit has replaced bonds and bank loans for lending. Since private credit spreads are not easily observable, problems in this area may not be observable either.

- Large company bankruptcies are on the rise. Higher interest rates are playing a role.

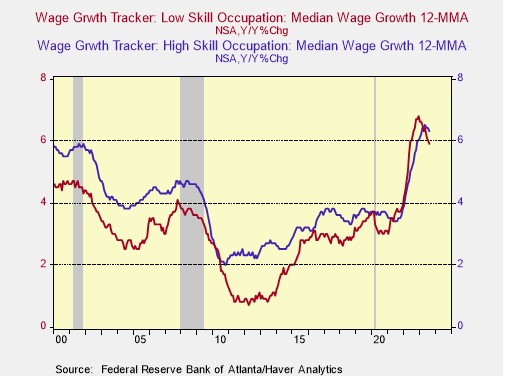

- The post pandemic labor market has exhibited an unusual characteristic—higher wage growth for less skilled workers.

- Recently, the premium for skill appears to have returned. However, anecdotal evidence suggests that higher skilled workers are facing a sluggish job market.

International Roundup: Russia moves to end its compliance with the nuclear test ban, the ruling coalition in Germany takes a drubbing in local elections, and there was an earthquake in Afghanistan.

- Russia claims it will end its compliance with the nuclear test ban treaty. Although this is making headlines, the treaty was never ratified by the U.S. and the agreement was never in force because too few nations agreed to it. But because the U.S. and Russia have abided by the terms, the announcement could lead to a resumption of testing.

- Russia withdrew its Black Sea ships from Crimea due to Ukrainian drone attacks.

- Conservative parties in Germany scored major wins in local elections. The AfD, a populist right-wing party, did surprisingly well. These wins are a signal to the ruling government that their policies are unpopular.

- Poland will hold elections later this week. This report details the parties and their leaders.

- There was a massive earthquake in Afghanistan with a death toll exceeding 2,400.

- The Maduro government in Venezuela has issued an arrest warrant for Juan Guaido, a major opposition leader. Guaido lives in the U.S, and he probably won’t be extradited, but given how the U.S. has eased sanctions on Venezuela, there is a chance Washington might send him off.