Daily Comment (November 10, 2017)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EST] We are seeing further equity weakness this morning; interestingly, too, Treasury yields are rising. The asset market weakness doesn’t appear to have a single cause, but rather a mix of factors has weakened investor sentiment. Here is what we are watching:

Who knew tax reform would be so hard? Although analysts persistently warned that tax reform would be difficult, investors seemed to be quite sanguine about the potential for change. The House and Senate have issued their bills and it’s hard to see a path to compromise. The Senate wants to delay implementing the corporate tax changes for a year, which will infuriate the White House. After all, no president has an interest in boosting future growth which may only benefit a successor. In addition to that major discrepancy, the marginal rate structure is vastly different. And, the Senate bill does less to “broaden the base” by reducing tax expenditures. Given the political situation, the Senate bill will tend to be the blueprint because it will be much more difficult to move the bill through that body than the House. We have had strong doubts that a tax reform bill would get passed during this administration. Our position remains the same. It should also be noted that there will be winners and losers if a bill does get passed. Those hurt may be exactly the kind of households that would usually support Republicans.[1]

The populist president: President Trump gave an anti-trade speech in Asia overnight, bookended by President Xi offering a robust defense of globalization. The cover of this week’s Economist is all about the U.S. stepping back from the world. This is a situation we have been discussing (and warning about) for the past eight years. Although there are lots of brave voices suggesting globalization can continue without the U.S., if it does, it won’t look like the last century’s globalization with the U.S. providing global security and the reserve currency for “free” to the world. Instead, we expect either an 18th century sort of colonization (the Eurozone as Germany’s commonwealth, the “one belt, one road” as China’s colonial drive) or a regionalization of power with no global power in place. At some point, financial markets will realize that a deglobalized world will not be good for business. Although we doubt this is the precise moment, the financial markets have mostly been ignoring the anti-trade, anti-immigrant policies of this administration. Perhaps some of that is being priced in.

The Roy Moore situation: Although we doubt the travails of Mr. Moore are significant to today’s weakness, we see one important takeaway. The scandal and the reaction show, in bright lines, the split within the GOP. When the Senate majority leader calls on a candidate to withdraw from a race in a solid Republican state, it begs the question…what kind of relationship will the party leadership have with him if he wins the special election? The election will be held on December 12. Given the polarized nature of the electorate, unless further evidence emerges, we expect Moore to win. Predictit still gives him a 55% chance of winning; that is down from 60% but still looks rather safe. But, for McConnell, how reliable of a vote will Moore be going forward? Our position is that the underlying coalitions of both parties are in flux but they become much more apparent for the party in power because it has to govern. The ACA debacle and now the issue with tax reform are laying bare these divisions with the GOP. The Roy Moore situation does, too.

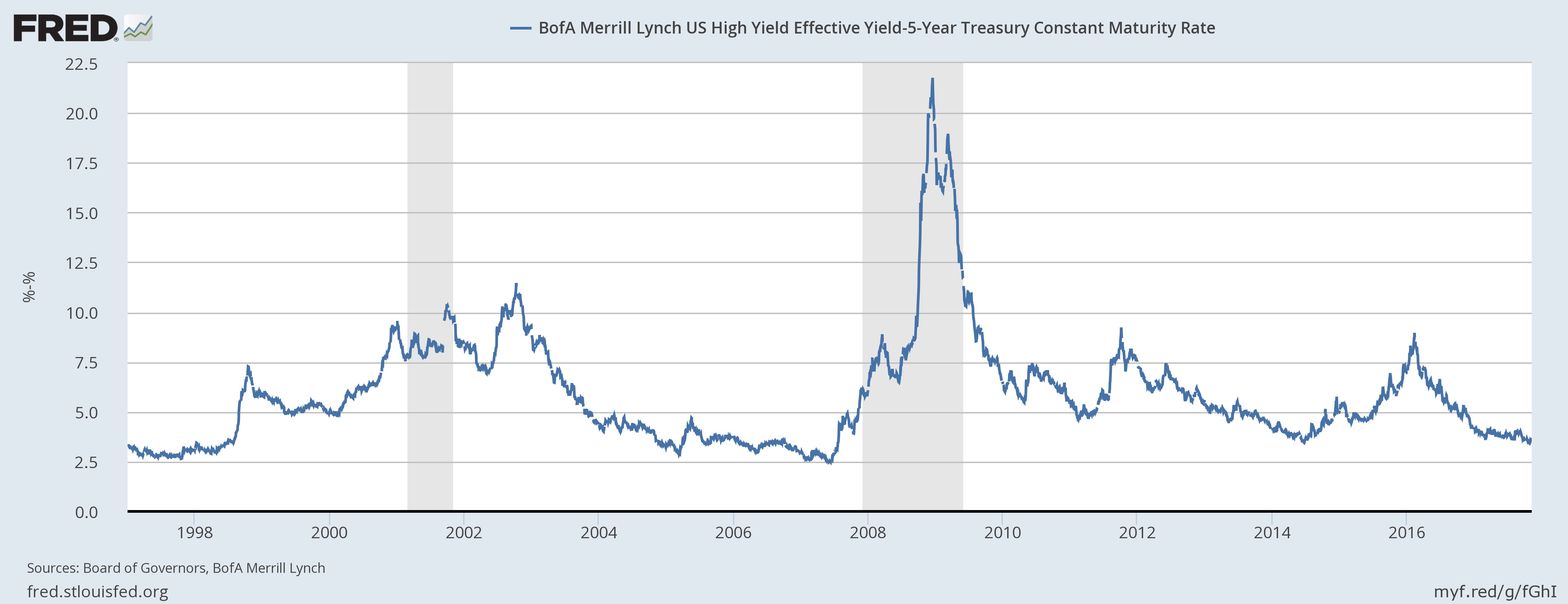

Junk takes a hit: High yield bonds have come under pressure in the past few days, mostly on disappointing earnings from firms that issue these instruments. Spreads have been narrowing for some time.

This chart shows the spread of high yield to the five-year Treasury. Note that the spread is in the lower range of history.

The rise in yields is seen at the right side of the graph. Will this continue? A move toward 6% would not be a shock, but to sustain rates higher than that level would require a rise in financial stress. So far, there isn’t much evidence that stress is rising.

Don’t forget December 8! On December 8, the borrowing capacity of the Treasury will be exhausted and a new debt limit will be required. Given that tax legislation is dominating the debate, Congress will scramble to make a deal to lift the debt ceiling; look for Democrat Party leaders to leverage this moment for their goals.

And, on other items:

China opens: In a surprise move, China announced today it will allow foreigners to purchase a majority stake in Chinese financial firms. This is a shocker, although in reality it will have less impact than it should. While there may be some interest from foreign firms in directly accessing the Chinese financial system, there is no consistent rule of law in China. A foreign firm could find itself the majority owner of a bank that the government forces to do things it doesn’t want to do. So, optically, this is a big deal, but it won’t have much effect if it isn’t accompanied by a consistent regulatory environment.

[1] https://www.washingtonpost.com/business/economy/i-dont-feel-wealthy-the-upper-middle-class-is-worried-about-paying-for-the-tax-overhaul/2017/11/09/a5cf1acc-c55e-11e7-aae0-cb18a8c29c65_story.html?utm_term=.dfb78c5a42bd&wpisrc=nl_todayworld&wpmm=1