Daily Comment (May 29, 2018)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EDT] It’s clearly another “risk off” morning—equities are lower around the world, the dollar, yen and Treasury prices are up, and most other currencies are lower. Europe is the culprit. Here is the story:

The Italian job: Over the Memorial Day weekend, Italy’s president, Sergio Mattarella, refused to allow a populist coalition of the Five-Star Movement and the League to form a government.[1] The sticking point was the group’s decision to name Paolo Savona as finance minister. Savona is deeply skeptical of the Eurozone and would likely press for Italy to exit the single currency. So, Mattarella scuttled the negotiations and instead appointed Carlo Cottarelli as a caretaker PM. Cottarelli is an anathema to the populists; he is a former IMF official and represents everything the populist coalition detests.

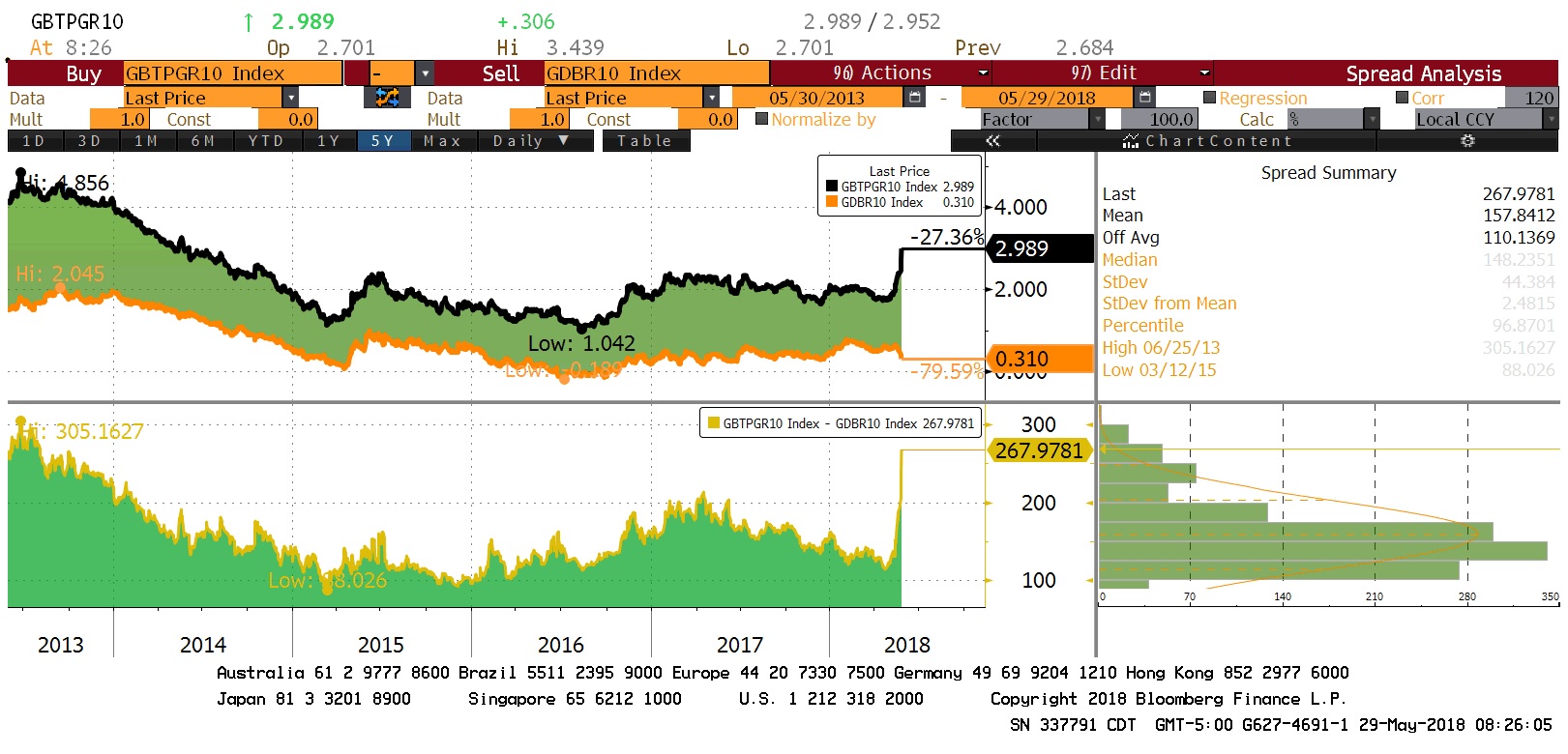

Italian bond yields continue to rise on the news.

Perhaps what is most impressive isn’t the spike in Italian yields but the drop in German Bund yields, which are now down to 31 bps from mid-60 bps before the crisis. The drop in German yields is a clear indication of capital flight, most likely from Italy.

The disgruntled coalition has called for Mattarella’s impeachment and there are reports that demonstrations and strikes are possible.[2] Assuming Cottarelli cannot form a government (and it is highly probable he won’t be able to), elections are likely to be scheduled for September. This election could be pivotal for the future of the Eurozone and the euro. Up until this point, the Italian parties have not really campaigned on leaving the single currency. The populist parties, instead, planned on flouting fiscal restrictions, daring the EU to stop them. However, the September poll is shaping up to be about Italy’s status in the Eurozone. Most polls show a slim majority support for continued membership in the Eurozone; only about 55% support the single currency, the second lowest of any Eurozone nation. Only Cyprus is marginally lower. Still, that means the majority of Italians still support remaining in the Eurozone. Thus, if the election does become a referendum on the single currency, the populists may not win. At the same time, the centrist parties are in deep disarray and may not be able to form a government anyway. Thus, the risks are unusually elevated that the September vote leads to a radical outcome.

What we find most interesting about the Italian situation is that Italy has created the “Nader coalition” of populist right and left wings.[3] Nader’s vision is that the economic goals of the right- and left-wing populists are close enough to build a dominant political coalition. Nader wrote his book for U.S. voters; however, to date, a Trump/Sanders coalition looks like a low probability event. Italy may be closer to Nader’s idea; interestingly enough, the policy mix of lower taxes, immigration restrictions and a basic national income doesn’t fit with any degree of fiscal restraint. Perhaps the secret to the Nader coalition is to jettison fiscal control.

Although purchasing power parity clearly favors the euro over the dollar, the potential for a bust-up of the Eurozone will hang as a major threat to the single currency and consequently weigh on the exchange rate. Of course, the worst case scenario rests on a significant populist win in September, which may not happen. Although Italy’s debt/GDP ratio is a whopping 132%, most of that debt is held domestically…in euros. If the Italian government leaves the Eurozone and tries to change the debt currency to the “new lira” instead of euros, the backlash would be significant. Our read is that most Italians like the external governor that Eurozone membership provides but oppose the fiscal constraints. Leaving the Eurozone would almost certainly be painful for Italian savers; thus, if the September vote becomes a referendum on remaining in the Eurozone, we suspect the populists will fail to form a government. But, the vote will be close and any casual observation of Italy’s economic performance since joining the Eurozone makes it clear that Italy will be better off outside the Eurozone once the painful adjustment process is complete. Getting to that “promised land,” however, requires a great deal of disruption that no one wants in the short run.

Spain, too: PM Rajoy faces a confidence vote on Friday. Rajoy’s center-right government has faced a series of scandals that have undermined sentiment. If the vote goes against Rajoy, the odds of new elections increase. Additional European political turmoil adds to concerns about the euro.

North Korea dialogue: After postponing talks, North and South Korea have moved aggressively to support negotiations. The leaders of the two Koreas have met[4] and envoys from both the U.S. and North Korea are meeting; in fact, a high-ranking North Korean official, Kim Yong Chol,[5] has arrived in New York for discussions. Although the Trump/Kim summit isn’t officially on, in reality, there are indications that talks are likely.

China trade: Breaking at the time of this writing, the Trump administration indicated it would proceed with tariff plans against China.[6] Given that negotiations continue, we see this as mostly posturing rather than signaling action.

[1] https://www.ft.com/content/f495fc3a-6283-11e8-90c2-9563a0613e56?emailId=5b0cd171da224c00049b3d0f&segmentId=22011ee7-896a-8c4c-22a0-7603348b7f22

[2] https://www.reuters.com/article/us-italy-politics/italys-league-leader-dismisses-talk-of-presidents-impeachment-idUSKCN1IT0GK

[3] Nader, R. (2014). Unstoppable: The Emerging Left-Right Alliance to Dismantle the Corporate State. New York, NY: Nation Books.

[4] https://www.reuters.com/article/us-northkorea-missiles/south-korea-calls-for-more-impromptu-talks-with-north-korea-as-u-s-seeks-to-revive-summit-idUSKCN1IT0JK

[5] https://www.cnn.com/2018/05/29/asia/kim-yong-chol-united-states-intl/index.html

[6] https://www.nytimes.com/2018/05/29/business/white-house-moves-ahead-with-tough-trade-measures-on-china.html