Daily Comment (May 28, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our thoughts on a potential AI tax. We then turn to Federal Reserve policy and the possibility of a rate hike. Next, we provide brief updates on the US-Iran conflict and the rise in semiconductor stocks. As always, we include a review of recent domestic and international economic data.

Taxing AI: In a recent Time op-ed, Senator Elizabeth Warren (D‑MA) called for changes to the tax code that would channel a portion of AI‑related gains into federal revenue and ensure the benefits are shared more broadly with everyday Americans. Her proposal comes as lawmakers search for ways to make rapid advances in AI more politically and socially acceptable to voters. It also lands at a moment when AI is playing a growing role in the economy while facing mounting public backlash over its pace of adoption, perceived equity implications, and the extent to which its expansion is seen as being facilitated by government support.

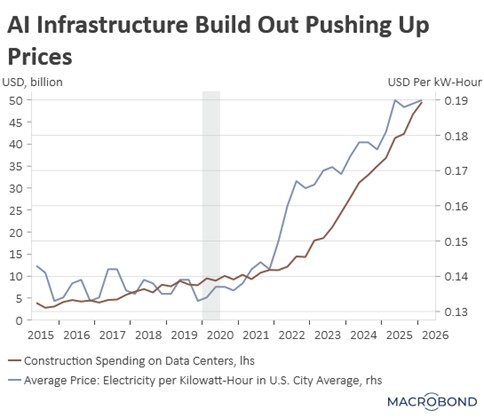

- Most of her tax proposals are familiar, including a wealth tax and higher capital gains taxes, and do not target AI specifically. However, she is also floating a more novel idea: an excise tax on data centers’ energy usage, which has received limited mainstream attention so far. In her view, such a levy would help large tech firms compensate local communities for higher utility costs tied to surging data‑center demand, and support the competitiveness of US companies in the global AI race.

- The idea of taxing data centers is not new as there has also been a recent push to tax computer processing. The key distinction between taxing energy and taxing computation is that an energy tax applies to the electricity consumed, while a compute tax applies to the volume of computational work itself. An electricity tax mainly nudges firms toward cheaper or cleaner power sources, whereas a compute‑based tax would more directly incentivize reducing or optimizing workloads.

- The renewed push to tax AI comes as major tech companies sharply increase capital spending to keep up with surging demand for the technology. In 2025, Nvidia CEO Jensen Huang argued that computing capacity will need to scale by orders of magnitude — potentially up to 1,000x — to support more advanced, agentic forms of AI. If AI capacity growth continues on this trajectory, an AI‑linked tax on energy use or consumption could become a meaningful revenue source for governments over time.

- While the idea of an AI tax remains purely speculative for now, it could gain momentum heading into the 2028 election. If enacted, such a tax would likely create a headwind for tech companies that rely heavily on data centers, as it would increase their operating costs. However, if AI continues to grow as fast as projected, the tax could also help raise government revenue and reduce the national debt, which might ultimately bring down longer-term bond yields.

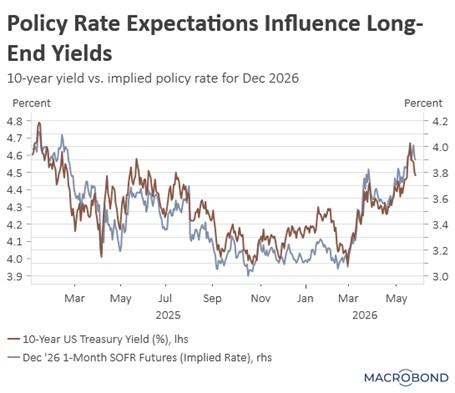

Hikes Possible? Nearly a month after the last FOMC meeting, Fed officials appear to be shifting away from an easing bias toward a more tightening-oriented stance. Following Governor Christopher Waller’s call to abandon the easing bias, several policymakers have begun signaling openness to a rate hike later this year. This shift in sentiment will likely place upward pressure on bond yields, as markets begin to reprice the policy path to reflect a higher probability of further tightening.

- On Wednesday, Fed Governor Lisa Cook highlighted a range of risks to the Fed’s price stability mandate, including artificial intelligence related disruptions, tariffs, and escalating tensions with Iran. She indicated a willingness to raise interest rates if inflation remains elevated. In contrast, Fed Governor Philip Jefferson struck a more optimistic tone suggesting that current policy remains well positioned, noting that inflation appears to be cooling, while emphasizing that upside risks to inflation persist.

- Inflation risks are rising as the Federal Reserve confronts a series of overlapping supply shocks. The AI build-out is lifting household utility costs and memory chip prices, while tariffs are increasing import prices. At the same time, the war in Iran is pushing up energy and food costs. These pressures are already feeding into goods prices — historically the more responsive component — but may increasingly spill over into services, where disinflation has proven far more persistent.

- The recent shift in risk sentiment has started to push the 10‑year Treasury yield higher. Market pricing indicates that the 10‑year yield remains highly sensitive to year‑end fed funds expectations. That tight relationship reflects the fact that long‑term yields are largely driven by the expected path of short‑term rates plus the term premium investors demand for bearing inflation, and bond supply risk over time. However, we think geopolitical risks may also be impacting term premia.

- The Fed’s pivot marks the start of a new regime during which the central bank must navigate recurring, supply‑driven geopolitical shocks — something it has not faced at this scale before. This backdrop is likely to complicate monetary‑policy calibration over the next several years, particularly as the global economy continues to deglobalize. In our view, that combination argues for elevated volatility in long‑term rates as the Fed adapts its reaction function to an evolving geopolitical landscape.

Iran Setback: The US on Thursday carried out multiple strikes on Iranian targets in the Strait of Hormuz, underscoring its commitment to keeping the waterway open. Ahead of the strikes, the US president vowed not to allow any actor to control the strait and warned Oman, a US ally, against supporting any Iranian effort to impose a toll in the region. Although the current truce still appears to be holding, developments on the ground suggest the ceasefire remains fragile.

Chipmakers Rise: AI enthusiasm has propelled chipmakers to their strongest run since the dot‑com era. The PHLX Semiconductor Index is up roughly 75% year‑to‑date, marking its best start to a year since 1999. The move has been driven largely by surging AI‑related capex and earnings expectations, even as macro and geopolitical uncertainty remain elevated. While we see scope for further upside in the near term, we continue to advocate adding value exposure as a way to mitigate concentration risk in AI‑heavy growth names.