Daily Comment (May 26, 2022)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Good morning! Today’s report begins with a summary of the Fed meeting minutes and other central bank news. Next, we discuss the latest developments in the Russia-Ukraine war. Afterward, we go over the pushback regarding China’s zero-COVID strategy and the possibility of global famine due to the Russian blockade of the Black Sea. We end with international news and our COVID-19 coverage.

Fed Meeting Minutes: The Fed meeting minutes revealed a consensus among voting members for the central bank to hike rates 50 bps over the next couple of meetings. The minutes reaffirmed market sentiment that the central bank might push rates into restrictive territory to tame inflation. As a result, the S&P rose slightly, and Treasuries were relatively unaffected. The Fed’s decision to maintain 50 bp hikes appears to be related to its confidence that the economy is strong and capable of withstanding additional tightening. Fed members and staff shrugged off the unexpected decline in Q1 GDP as being temporary. Additionally, the group downplayed the possibility that decreases in inventory spending, government spending, as well as net exports, would persist throughout the year. Although the Fed was generally upbeat about the economy, it mentioned the Russia-Ukraine war and lockdowns in China as threats to the expansion.

Central Bank News

- Federal Reserve Bank of Kansas City President Esther George has announced that she will be stepping down in January. The decision to leave her post was not surprising. Fed officials are required to step down due to mandatory retirement rules of Fed Presidents. Chicago Fed President Charles Evans is also expected to step down for a similar reason. As a result, there will likely be two vacancies in 2023 among the 12 regional banks.

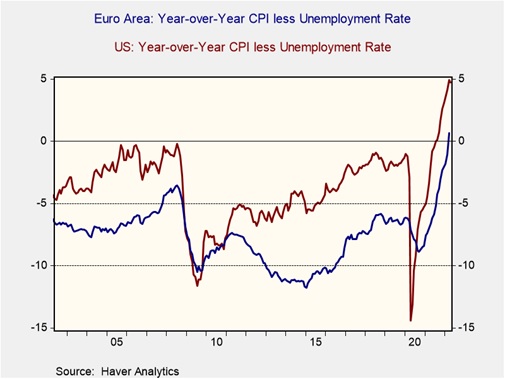

- There are growing fears that the ECB is behind the curve in containing inflation. Veteran British economist Charles Goodhart warned wage pressures would contribute to inflation as workers demand higher pay to cope with increasing food and energy prices. There seems to be a broad consensus among ECB members to end negative rates next quarter, with Dutch central bank chief Klaas Knot stating that he would support a 50 bp rate hike in July. By one of our central bank policy measures, seen in the chart below, the ECB may be behind the curve but still in a better position than the U.S. This suggests that the ECB may not have to raise rates as aggressively.

- The chart above shows the annual change in CPI minus the unemployment rate. When CPI exceeds that unemployment rate, it signals that the economy may be overheating.

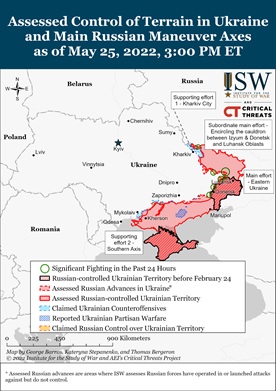

Russia-Ukraine: As the war enters its fourth month, the Kremlin faces growing criticism on social media regarding the way it is handling the Ukraine war. Bloggers on Telegram have complained that the government has not adequately supplied Russian soldiers with military equipment needed to hold off Ukraine troops. Although it is unclear how impactful these messages are on the general public, the backlash suggests the government may be losing control over the narrative. Meanwhile, the West is preparing for the possibility of a long war. NATO general Jens Stoltenberg urged countries need to be prepared to provide Ukraine with additional support. We believe that as the conflict rages on, the West will struggle to maintain its coalition. The inability of the EU to secure an agreement on the Russian oil ban reinforces the concern that this coalition may fracture in the future. If we are correct, it could mean the West could push Ukraine into accepting a ceasefire with Russia. At this time, leaders in both Russia and Ukraine have been postponing peace talks, hoping to secure more leverage. We believe such negotiations will happen sooner rather than later.

On the ground, Russian forces have entered Lyman and are closing in on Popasna. Russian troops are making gains in Ukraine but very modestly. The military is struggling to find reserves to carry out the mission. It has raised the maximum age for army recruits and forced border guards to cancel their vacations.

The Global Food Crisis: The Russian blockade of Ukrainian ports continues to stir fears of global famine and instability. Russia and Ukraine supply about 30% of the world’s wheat, a crucial food source for developing countries. In response to criticism, Russia has agreed to relieve some of the pressure by opening the Black Sea port for foreign ships. The move should put downward pressure on grain prices.

- Brazil agreed to supply China with corn. The move comes as Beijing looks to build up its stocks to hedge against a potential food crisis. The agreement led to a decline in corn prices due to concerns that the deal could reduce demand for U.S. corn.

Zero-COVID Policy: In a rarity, Chinese Premier Li Keqiang openly acknowledged that the zero-COVID strategy is harming the economy. In a meeting with multinationals operating in China, Li offered reassurances that the country would do its best to expand vaccinations. In addition, conceding the need for increased vaccinations, Li warned that the Chinese economy could struggle to avoid a contraction in the second quarter. His remarks highlight the growing unease among members of Chinese leadership about Xi’s decision to reimpose COVID-19 restrictions.

International News

- Hungarian President Viktor Orban has demanded the largest companies turn over “extra profits” to help the government with its finances. The Hungarian government lacks funding for it wants to pay for utility subsidies and improvements in the country’s armed forces. The government had its funding frozen by the EU over accusations that Orban is undermining democracy.

- Iran’s nuclear program was likely more advanced than previously thought. Intelligence officials believed Iran secured access to United Nations atomic agency reports and falsified a record to conceal its past work on nuclear weapons. However, the revelation may complicate the efforts of the Biden administration to secure a nuclear agreement.

Interesting facts:

- Saudi Arabia is exploring a takeover of Valvoline’s lubricant business.

- A financial scam has led to protests in China’s Henan Province.

COVID-19: The number of reported cases is 527,228,581, with 6,282,713 fatalities. In the U.S., there are 83,702,508 confirmed cases with 1,003,738 deaths. For illustration purposes, the FT has created an interactive chart that allows one to compare cases across nations using similar scaling metrics. The CDC reports that 739,095,455 doses of the vaccine have been distributed, with 583,221,364 doses injected. The number receiving at least one dose is 258,312,266, the number of second doses is 221,050,854, the number receiving the first booster is 102,997,276, and the number receiving the second booster is 12,988,274. The FT has a page on global vaccine distribution.