Daily Comment (May 10, 2019)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EDT] The tariffs were applied at midnight. Here is what we are watching:

China trade: As the president promised, tariffs on trade with China were applied at midnight.[1] Interestingly enough, financial markets took the news in stride, with equities up across the world…until a series of early morning tweets from the president indicated a high level of comfort with tariffs, in general, and included a threat to apply tariffs on all goods from China.[2] The comments reversed equities, sending U.S. futures lower.

As we have watched this issue play out this week, here are some observations we have made:

- It is becoming obvious that the president views tariffs as taxes that foreigners pay. And, it has become an article of faith in the mainstream media that consumers pay the tax.[3] The reality is far more complicated. In public finance, which is a branch of economics that studies government spending and taxing activity, who ultimately pays the tax is called the “incidence” of the tax. With tariffs, the incidence can fall on several parties.

- In its simplest form, a good reaches our border, customs officials apply a tariff and collect the fee from the buyer and the buyer passes on the tax in the final goods price. In this case, the incidence is, indeed, on the consumer.

- But, if a foreign seller faces competition for his product in the nation applying the tariff, the importer may take price action to protect market share. In this case, the importer may reduce the price to offset the tariff, thus the ultimate incidence of the tax falls to the exporter.

- Under conditions of flexible exchange rates, the importer’s currency may weaken. This would lower the price of the imported good, offsetting some or all of the tariff, meaning the incidence of the tax falls on the consumers in the foreign nation (who now face higher prices for all imports) and on the domestic nation’s exporters (who face a markup on their exports due to the currency appreciation).

- So, what is likely to occur? The most likely outcome is dollar appreciation. Although the dollar is overvalued on a parity basis, the trade war is an outlier event and therefore nearly impossible to model. Tariffs have become increasingly less common in the postwar era; U.S. hegemonic policy tended to support free trade and flexible exchange rates undermine the effectiveness of tariffs. Consequently, the more we see “saber rattling” on trade, the greater the odds are that the dollar becomes a one-way bet. We have covered currencies since 1986.[4] And, one observation we have about exchange rates is that markets tend to focus on one factor to the exclusion of all others and that factor drives trading until valuation levels become untenable. In the early 1980s, during the Volcker era, it was all about interest rate differentials. After the Plaza Accord, trade data drove exchange rates. Interest rates made a brief return in the early 1990s, only to be eclipsed by productivity differences into the turn of the century. Interest rate differentials returned into the financial crisis, when flight to safety dominated. And, since 2009, interest rates have mostly dominated exchange rate trends. We are becoming concerned that tariffs might dominate traders’ minds in the coming months and push the dollar to levels that will undercut U.S. exporters and pressure foreign stocks and large caps. It hasn’t happened yet and, if this doesn’t occur, it will be due to the Fed moving to cut rates.

- In our 2019 Outlook we focused on four potential risks to the market, with monetary policy and trade issues as the first two risks. Until recently, we felt rather confident that these two risks had mostly been addressed. The Fed had gone on hold and it looked like a trade war with China would likely be avoided. Perhaps the biggest risk to the markets now isn’t necessarily the trade issue as much as the Fed may see tariffs as inflationary and begin to make noise about raising rates. This is still a low probability event. The Fed remains data-sensitive and probably won’t move to lean hawkish without clear evidence of rising prices. And, if our expectation for a stronger dollar plays out, the chances of rising inflation diminish even further. But, if we are wrong, if the dollar doesn’t rally and the incidence of tariffs falls on consumers, then the risk to the expansion from monetary policy returns as a significant threat.

- We have been paying close attention to the politics of the tariffs. This attention is mostly art and less science but we take note of local media reports, podcasts, commentary, etc. Our take, so far, is that China is being seen as a bad actor and the president has much more support for his tariff actions than is probably understood. Even in the farm belt, an area bearing the brunt of the trade conflict, the tariffs are seen as harmful but probably necessary. The only group that is consistently pro-trade is the right-wing establishment, who are committed to globalization (the left-wing establishment is also pro-trade but is a less vocal supporter). The U.S. has been steadily becoming anti-trade. Note that both TPP and TTIP failed to progress even though, from a geopolitical viewpoint, both would have led to U.S. trade dominance, at least in terms of setting rules. To some extent, this shift against trade makes sense. Trade becomes popular when inflation is considered a problem. With inflation being low and controlled for a long time, support for policies that reduce inflation would be expected to wane. The other factor we note is that, in a hyper-partisan era, there is a great deal of cross-party support for actions against China. The lack of political fallout for tariffs, even if it has some negative effects on the economy, will likely embolden the president further. Thus, it would be unwise to think the trade conflicts are going away anytime soon. If anything, the EU is next; we would expect something on auto tariffs with the EU next week[5] and increasing trade tensions with Europe.[6]

- If our analysis of the politics is correct, at least initially, the negative impact from tariffs on equities may be limited. To some extent, multiples are a reflection of sentiment, and if there is a “rally ‘round the flag” moment with tariffs then equities may be able to offset the potential loss of margins from deglobalization by multiple expansion. Tariffs are, in isolation, bearish for stocks but the negative impact may not be extreme until a clear adverse impact on the economy becomes evident.

North Korea: As the Kim regime tests short-range “projectiles” the U.S. has seized a coal ship, which the administration says has been used to avoid sanctions.[7] We have no doubt that North Korea has been systematically working to evade sanctions, but the timing of this seizure will heighten tensions.

China and grain: China says it will have a bumper soybean crop this year.[8] If true, that would mitigate the price effects of tariffs on U.S. grain imports. However, the USDA reports that China could be facing a new foe, the armyworm, a pest that would affect all its crops.[9] If the pest spreads, it would have an adverse effect on China’s crop production and force it to import more corn and soybeans, just when it is restricting U.S. grain due to the trade conflict.

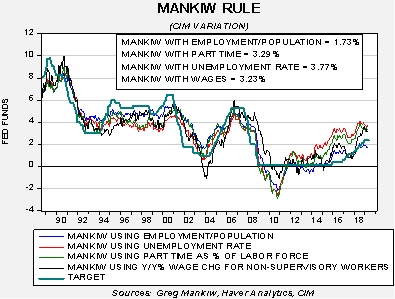

Mankiw Rule update: The Taylor Rule is designed to calculate the neutral policy rate given core inflation and the measure of slack in the economy. John Taylor measured slack using the difference between actual GDP and potential GDP. The Taylor Rule assumes that the Fed should have an inflation target in its policy and should try to generate enough economic activity to maintain an economy near full utilization. The rule will generate an estimate of the neutral policy rate; in theory, if the current fed funds target is below the calculated rate, then the central bank should raise rates. Greg Mankiw, a former chair of the Council of Economic Advisers in the Bush White House and current Harvard professor, developed a similar measure that substitutes the unemployment rate for the difficult-to-observe potential GDP measure.

We have taken the original Mankiw Rule and created three other variations. Specifically, our models use core CPI and either the unemployment rate, the employment/population ratio, involuntary part-time employment and yearly wage growth for non-supervisory workers. All four compare inflation and some measure of slack. Here is the most recent data:

This month, the estimated target rates were little changed. Three of the models would still suggest the FOMC is behind the curve and needs to be increasing the policy rate. However, the employment/population ratio suggests a rather high level of slack in the economy and would suggest the Fed has already lifted rates more than necessary. Given the uncertainty in the economy, coupled with political pressure, we expect the FOMC to remain on the sidelines.

Odds and ends:Treasury Secretary Mnuchin has been more sensitive to the exchange rate issue than the rest of the administration. He clearly sees that foreigners could respond to tariffs with depreciation and has warned nations against it. Vietnam has been duly warned.[10] Canada has just noticed that the capital flight that has led to a real estate boom in select cities may have been with laundered money[11]…what a shocker![12]

[1] https://www.ft.com/content/ed52b21c-72ca-11e9-bf5c-6eeb837566c5?emailId=5cd4e901e1e6070004875dfb&segmentId=22011ee7-896a-8c4c-22a0-7603348b7f22 and https://www.nytimes.com/2019/05/09/us/politics/china-trade-tariffs.html?emc=edit_MBE_p_20190510&nl=morning-briefing&nlid=5677267tion%3DtopNews§ion=topNews&te=1

[2] https://twitter.com/realDonaldTrump?lang=en

[3] https://www.axios.com/trump-wrong-china-tariffs-b951dd76-3da8-492e-8cb2-5cbffe695498.html

[4] Obviously, this is Bill talking; Thomas was not yet on the earthly pale in 1986.

[5] https://www.reuters.com/article/us-autos-tariffs/automakers-expect-white-house-to-delay-decision-on-auto-tariffs-sources-idUSKCN1SE2MA?utm_source=GPF+-+Paid+Newsletter&utm_campaign=06d84cdbff-EMAIL_CAMPAIGN_2019_05_09_02_50&utm_medium=email&utm_term=0_72b76c0285-06d84cdbff-240037177

[6] https://www.reuters.com/article/us-usa-trade-hogan/eu-commissioner-says-agriculture-not-on-agenda-for-u-s-talks-idUSKCN1SG09F

[7] https://www.ft.com/content/1e55a9e0-7231-11e9-bf5c-6eeb837566c5?emailId=5cd4e901e1e6070004875dfb&segmentId=22011ee7-896a-8c4c-22a0-7603348b7f22

[8] https://www.reuters.com/article/us-china-crops/china-expects-its-2019-20-soybean-output-to-hit-highest-in-14-years-idUSKCN1SG0FR

[9] https://www.cnbc.com/2019/05/08/voracious-pest-threatens-chinas-crops-could-boost-need-for-imports.html

[10] https://www.axios.com/newsletters/axios-markets-9b3debf1-3895-4738-aa07-2c69d8dfdd86.html?chunk=5#story5

[11] https://www.wsj.com/articles/canada-says-money-laundering-is-raising-housing-prices-11557440252?mod=hp_listc_pos1