Daily Comment (March 12, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with an update on the war in Iran, focusing on rising tensions around the Strait of Hormuz. We then review the February CPI report and assess how the Middle East conflict could shape the path of inflation. Next, we highlight key market developments, including shifts in the US trade strategy and China’s recent incursions into Taiwan’s airspace. As always, we include a summary of recent US and international economic data releases.

Rising Tensions: Trade tensions have escalated following reports that shipping lanes in the Strait of Hormuz are becoming increasingly impassable. On Wednesday, an attack on six oil tankers in Iraqi waters signaled the growing risks for vessels navigating the region. The incident has raised concerns that the war is showing signs of becoming prolonged and that trade throughout the region is likely to remain restricted, leading to a significant rise in oil prices due to renewed fears of a supply shock.

- Rising tensions in the Strait of Hormuz have underscored Iran’s capacity to prolong the conflict well beyond earlier expectations. The latest attacks came about just as the United States had tried to reassure shippers by destroying Iranian mine‑laying vessels, warning Tehran over the use of naval mines, and considering naval escorts to safeguard commercial traffic and keep the waterway open.

- These incidents have reignited fears of prolonged disruptions to trade flows, despite a historic, coordinated effort to stabilize markets through strategic oil releases. On Wednesday, the International Energy Agency said member countries will collectively release 400 million barrels, with Japan initiating the first drawdowns and the United States planning to contribute 172 million barrels from its Strategic Petroleum Reserve.

- Additionally, there are growing signs that Iran is prepared to widen the scope of its attacks to ensure that more countries bear the costs of the war. On Wednesday, the United Arab Emirates reported that it had intercepted another wave of missiles after Iran threatened to target Israeli‑linked banks in the region. US officials have also warned of indications that Iran is considering plotting strikes as far afield as California, underscoring the expanding geographic reach of its threat posture.

- Despite the latest attacks, it appears that Iran may be seeking an off‑ramp from the conflict. Tehran has reportedly signaled a willingness to de‑escalate in exchange for international guarantees that the United States and Israel will halt military strikes on its territory. While this is unlikely to bring both sides to the negotiating table on its own, it does suggest that Iran recognizes it cannot prevail in a direct confrontation and may be looking to limit further escalation.

- While we remain cautiously optimistic that the war will begin to wind down over the next couple of weeks in line with the president’s timeline, we are increasingly mindful that its economic and market aftershocks could persist for months. In our view, this evolving backdrop continues to favor value over growth, and we advocate for maintaining broad diversification away from riskier market segments, particularly as the conflict’s trajectory remains uncertain.

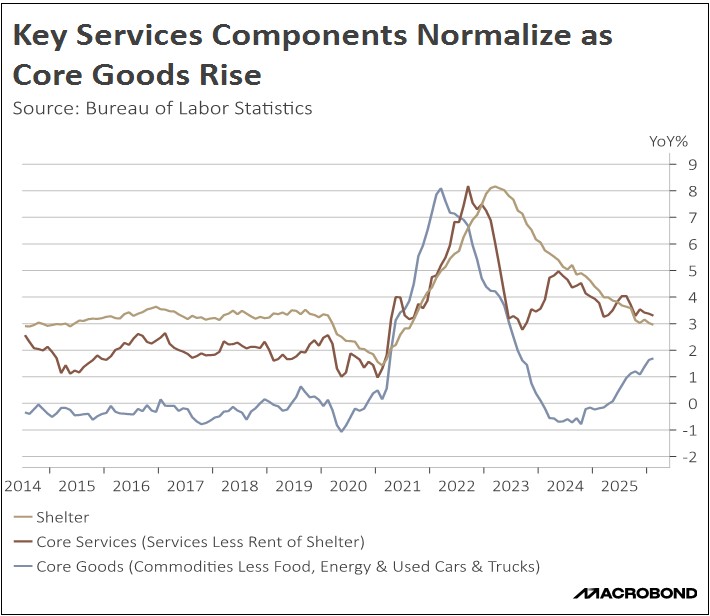

Inflation Risk: The latest CPI report offers fresh evidence that inflation is holding mostly steady but not quite enough to fully dispel concerns about renewed price pressures. According to the BLS, both headline and core inflation held steady in February at 2.5% and 2.4%, respectively, reinforcing the view that some of last year’s inflationary momentum is easing. In a world without the current conflict in the Middle East, this pattern likely would have opened the door to more serious discussions about a potential summer rate cut.

- The modest headline inflation reading reflects gradually easing underlying price pressures, particularly in services, even as some energy components ticked higher. In February, shelter inflation continued to exhibit tentative moderation, with its annual pace the slowest since August 2021. By contrast, the energy index rose for the month, driven by gains in gasoline and natural gas, while electricity prices edged slightly lower after strong increases over the past year.

- The inflation report indicates that price pressures are gradually returning to more normal levels but there are signs that they were starting to lose steam while moving toward the Fed’s 2% target. Shelter inflation has moved back into its typical historical range, and core services inflation, while still slightly elevated, is drifting closer to its longer‑run pace. Goods inflation, which has been influenced by shifting tariffs and supply‑chain costs, also appears to be stabilizing after prior bouts of volatility.

- Renewed turmoil in the Middle East has reignited concerns that supply-chain stress will once again feed into the inflationary pipeline. As higher energy and raw-material costs filter through the production process, core goods prices could face sustained upward pressure. Services may face “cost-push” inflation as energy-intensive services like air travel — currently facing rising fuel, insurance, and rerouting expenses — are likely to face margin pressure due to the conflict.

- The supply chain risks emanating from the Middle East could collide with surging demand pressures stemming from last year’s tax bill. Beyond stimulating household consumption, the legislation’s aggressive investment incentives have triggered a significant capital expenditure boom. The resulting scramble for materials to build AI data centers has already tightened markets for critical inputs like aluminum and energy, a situation poised to worsen as the conflict in the Middle East persists.

- While the current hostilities are contributing to higher inflation, the full magnitude of the impact remains unclear at this time. At present, we do not anticipate a return to the peak inflation levels seen in the post-pandemic era as the current supply-chain disruptions lack the breadth of the 2021–2022 lockdowns. However, the duration of the conflict remains the critical variable. We expect the resulting inflationary pressure to push back the timeline for the Fed to achieve its 2% target, a dynamic that will likely weigh on bonds.

Tariff Wall: The White House is preparing a new trade investigation targeting major partners as it seeks to reimpose tariffs recently struck down by the Supreme Court. The probe will focus on economies with excess manufacturing capacity. While the administration has pivoted from now‑illegal IEEPA tariffs to temporary duties tied to current account imbalances, those measures will expire after 150 days unless Congress intervenes. The new investigation is therefore likely to stoke concerns about renewed tariff hikes and greater trade policy uncertainty.

China’s Moves: Beijing sent warplanes into Taiwan’s airspace on Wednesday in a provocative move that signals rising tensions. The incursion followed a period of relative calm, during which China appeared to scale back such flights after trade and diplomatic talks with the United States. However, the move seems to be a test of what China can get away with while the US is focused on the Middle East, potentially setting a precedent for future actions.