Daily Comment (June 7, 2023)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Our Comment today opens with new, upgraded forecasts for global economic growth from the World Bank. We next review a wide range of other international and U.S. developments with the potential to affect the financial markets today, including a big slide today in the Turkish lira (TRY) as the country’s new finance minister begins shifting polices and the prospect for another big labor action in the U.S.

Global Economy: In its latest Global Economic Prospects report, the World Bank said it now expects global economic output to increase an inflation-adjusted 2.1% in 2023, up from its forecast of 1.7% in January but still weaker than the 3.1% expansion last year. Nevertheless, it also cut its forecast for 2024 to 2.4%, versus its January estimate of 2.7%.

- The revised forecasts essentially reflect how the U.S. and other key countries have maintained their economic momentum better than anticipated at the start of the year, which will likely push much of their slowdown or recession into next year.

- Prolonged economic momentum may be good for labor demand, but the institution warned that the resulting interest-rate hikes by the Federal Reserve and other central banks are causing increasing strains on many less-developed countries.

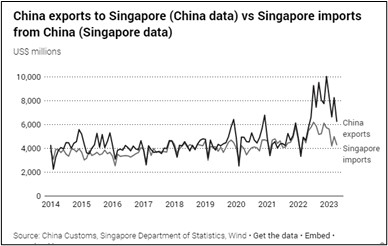

China: Despite the World Bank’s upwardly revised growth forecasts for 2023, the faltering recovery in China remains a concern for global investors. New analyses suggest the government may be fudging its export data upward to show national growth is better than it really is. The analyses show discrepancies between China’s official export data and a range of other export indicators. Faltering demand growth in China would likely be a major headwind for overall global growth and the financial markets.

- In official data released today, China’s May exports were down 7.5% year-over-year, after a rise of 8.5% in the year to April. The reported decline for May was much worse than analysts anticipated, but that won’t necessarily stop the concerns about inaccurate reporting to make the economy look better than it really is.

- Meanwhile, May imports were reportedly down 4.5% on the year, after a fall of 7.9% in the year to April. Falling imports also point to weakening demand in China.

China-United States: In a sign that bilateral relations could be stabilizing, U.S. Secretary of State Blinken will reportedly visit China later this month. That would mark a rescheduling of the meeting Blinken planned to make in February before it was derailed by that month’s Chinese spy balloon incident over the U.S. Any resumption of high-level contact between U.S. and Chinese leaders could help ease the acrimony between the countries, but we believe the overall rivalry will continue to sharpen over time and drive further global fracturing, re-industrialization in the U.S., shortened global supply chains, and higher inflation and interest rates.

United Kingdom: Mortgage lender Halifax said the average British home price in May was down 1.0% from one year earlier, marking the first year-over-year decline since 2012. The decline in home values comes as the Bank of England reports that the country’s average mortgage interest rate has topped 4.5% for the first time since the Great Financial Crisis, with more hikes by the central bank expected in the coming months.

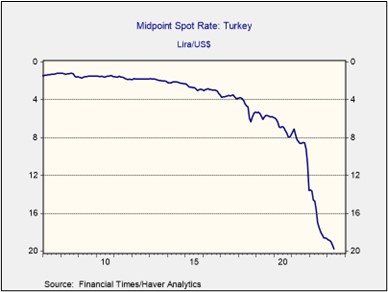

Turkey: The Turkish lira (TRY) is down approximately 7% against the U.S. dollar so far this morning, recently trading at around 23 per greenback. In contrast with the currency’s previous sharp drops, this one doesn’t appear to stem from concern about new, unorthodox economic policies or the threat of a financial crisis. On the contrary, today’s decline appears to reflect a move toward better economic policies by newly installed Finance Minister Şimşek. Specifically, today’s fall appears to reflect the government reducing its support for the currency and letting it trade more freely.

U.S. Fiscal Policy: Investors are becoming increasingly worried that the Treasury Department will have to auction as much as $850 billion in bills between now and September to replenish its coffers and make up for the months when it was constrained by the recent standoff over a new debt limit. As we’ve warned before, massive make-up issuance will drain liquidity out of the financial markets, potentially pushing down asset prices at least in the near term.

- Separately, some defense hawks in Congress are unhappy with the military budget’s minimal 3.3% increase under the deal to lift the debt limit. Hawks in both the House and the Senate have floated the idea of an immediate supplemental appropriation bill to boost defense spending further in the coming fiscal year.

- However, House Speaker McCarthy threw cold water on that idea earlier this week. It remains to be seen whether he will be able to hold the line on the defense budget as Congress gets to work on its appropriation bills in the coming weeks.

U.S. Retailing Industry: While we continue to believe that global geopolitical fracturing will make re-industrialization of the U.S. economy a key trend in the coming years, as discussed in our Comment on Monday, new reporting suggests it will also lead to changes in U.S. retailing. As foreign retailers become more wary about investing in China and its bloc, many that have only a small presence in the U.S. right now are reportedly planning to open large numbers of new stores here in the coming years. Besides creating new competition for U.S. retailers, the expansion could help those foreign firms make up for lost opportunities in the China bloc.

U.S. Labor Market: Teamsters President Sean O’Brien warned that his union will take a highly demanding, “militant approach” to negotiations with employers, including the upcoming talks for a new contract with UPS (UPS, $167.59). That contract expires on July 31, and O’Brien specifically warned that he would take the union out on strike if the company doesn’t agree to universal pay rises, the end of an existing two-tier pay system, the installation of air conditioning into trucks, and other demands.

- The contract between the Teamsters and UPS is the country’s biggest labor deal, covering some 340,000 drivers and package handlers.

- A strike at UPS could therefore have a significant impact on the economy, not only by disrupting activity for businesses and individuals, but also by further signaling to workers their improved bargaining power amid today’s labor shortages.