Daily Comment (June 27, 2022)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Our Comment today opens with an update on the Russia-Ukraine war. New sanctions are being discussed by Western leaders. We next review other international and U.S. developments with the potential to affect the financial markets today, including multiple items relating to China. We wrap up with the latest news on the coronavirus pandemic.

Note: Because COVID-19 has become more endemic and in most countries isn’t disrupting the economy or politics as much as it did previously, we will drop our dedicated COVID-19 section beginning July 1. We will continue to cover pandemic news as needed within our main text.

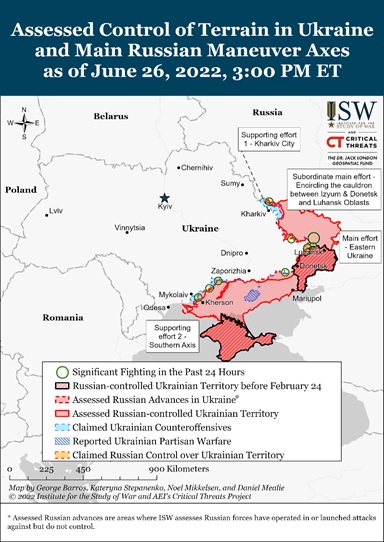

Russia-Ukraine: As Russian forces continue to make slow, plodding progress in seizing territory in Ukraine’s eastern Donbas region, Ukrainian forces continue their increasingly successful counterattacks in southern Ukraine around the port city of Kherson. Both countries face worsening shortages of personnel and equipment, and Russian President Putin continues to implement a “cover mobilization” to raise more troops. According to reports, the Russian State Duma will consider a bill that would allow military officials to offer contracts to young men immediately upon “coming of age” or graduating high school. It circumvents the need for conscripts to complete military service before being sent to fight in the war. On the Ukrainian side, Western leaders will discuss providing further, “sustained” military aid to the country at their summits this week.

- Not only has Putin’s invasion backfired on him by making Ukraine a candidate for membership in the EU, but it has also hastened Ukraine’s integration into the EU economy. As early as July, the EU will begin importing small amounts of electricity from Ukraine, with greater amounts expected in the future as power infrastructure is linked. Since so many people have fled Ukraine because of the war, the country now has surplus generating capacity, even as many EU countries face a deficit.

- U.S. and British officials indicated the Group of Seven summit this week would approve a broad ban on importing Russian gold, one of the country’s key commodity exports after energy. The Russian central bank reportedly holds some 2,000 metric tons of the metal, worth approximately $140 billion. Russia has exported tens of billions of dollars of gold to G7 countries in recent years (especially to the U.K.). The officials are also considering imposing a price cap on Russian oil exports and new tariffs on other Russian goods.

- The ban on Russian gold can be seen as the logical corollary of the Western countries’ freeze on Russian reserve assets. Indeed, it appears an informal ban on Russian gold has already been in place. The weekend announcement was notable for making it public.

- In the immediate term, the ban could give a modest boost to gold prices. So far this morning, gold is trading up about 0.4% to $1,837.00. In the longer term, however, prices could reverse and even go lower. For one thing, Russia has proven adept at getting its commodities to market, despite Western sanctions, by leveraging their fungibility and the willingness of China, India, and other countries to deal with them. For another, the G7 action will likely reduce the attractiveness of holding gold and therefore lead to lower demand. In each case, at least some Western officials probably understand the difficulty in making such sanctions truly painful for Russia, but that concern is probably outweighed by the need to make a political statement against the invasion.

- The G7 nations are also considering a change to their bans on Russian oil imports. To stop Russia from earning high prices by exporting oil to non-sanctioning countries, the G7 is looking at allowing Western shipping, insurance, and other financial services firms to deal with Russian oil exports as long as the importer observes a price cap. Besides cutting Russian oil revenues, the goal would be to bring down global oil prices. All the same, Brent crude is trading 0.7% higher so far this morning, at $109.89 per barrel.

- Reflecting the impact of the West’s previous sanctions, Russia yesterday defaulted on its sovereign foreign debt for the first time in over a century. Moscow has set up a mechanism to deposit rubles in special bank accounts for the benefit of bondholders that doesn’t appear to match the $100 million or so of dollar and euro payments required to be paid by yesterday under the bond documents.

G7 Summit: Besides the ban on Russian gold imports mentioned above, the G7 leaders announced a new “Partnership for Global Infrastructure and Investment” program that will jointly provide $600 billion for infrastructure investments in less-developed countries by 2025 to counter China’s Belt and Road Initiative. Relying on both public and private funds, the program will finance investments in projects such as climate resilience, secure information and communications technology, gender equity, and modernizing health systems, including vaccine manufacturing facilities.

Global Monetary Policy: In its annual report, the Bank for International Settlements warned that global central banks must raise interest rates sharply, even if it significantly hurts growth. Otherwise, the “central banks’ central bank” said the world risks a 1970s-style inflationary spiral. While central banks like the Federal Reserve are clearly behind the curve in fighting inflation, the BIS warning could help push the policymakers into tightening monetary policy so quickly that they produce a recession, most likely sometime in 2023.

Chinese Economy: New reports indicate small and medium-sized businesses throughout China are drastically cutting their hiring plans in response to the country’s draconian pandemic lockdowns, rising costs, and waning orders from overseas. Some firms have even been cutting wage rates and laying off workers.

- The development will make it even harder for officials to meet their official goal of 5.5% economic growth this year.

- The slowdown also increases the chance that officials will resort to their traditional strategy to boost growth: a debt-funded public investment that will further exacerbate China’s high debt levels.

Chinese Politics: Ahead of the Chinese Communist Party’s 20th National Congress this fall, where President Xi will try to win a groundbreaking third term in power, at least nine provincial party chiefs have published fawning articles extolling the president and pledging loyalty to him. The articles have even used over-the-top reverential terms for Xi that have rarely been used since Mao’s cult of personality decades ago.

- The articles have generally coincided with this month’s provincial party congresses, where delegates to the national congress are being confirmed.

- The articles reflect the provincial chiefs’ jockeying for plum positions at the autumn congress, but they alone indicate widespread certainty that Xi will secure his third term at the meeting, further enhancing his power and setting him up to be president for life.

Japan: Amid a blistering heat wave, the government today called on businesses and the public in the Tokyo area to cut electricity use, saying a lack of generating capacity risked plunging the capital into a power blackout. If prolonged, any resulting power outages could be a headwind for Japanese economic growth.

China-United States-Japan, et al.: Alarmed by China’s effort to court the island nations of the western Pacific Ocean, the U.S. and several key allies have launched a new initiative to bolster and coordinate their engagement with those nations. The “Partners in the Blue Pacific” initiative encompasses the U.S., Japan, Britain, Australia, and New Zealand and is designed to blunt Chinese overtures to nations in the region, such as the new pact potentially allowing China to send military forces to the Solomon Islands.

United States-Israel-Saudi Arabia-Egypt-Iran: New reporting shows top military officials from the U.S., Israel, Saudi Arabia, Egypt, and other Middle Eastern states met in March to discuss how they could defend against Iran’s growing missile and drone threats. As the U.S. seeks to step back from its role as the guarantor of Middle Eastern security to focus on threats from China and Russia, the report suggests it is seeking to install Israel in its place, at least in terms of air defense.

- At the March talks, the participants reached an agreement in principle on procedures for rapid notification when aerial threats are detected. The officials also discussed how decisions might be made on which nation’s forces would intercept aerial threats. However, top national leaders need to approve the evolving “Middle East Air Defense Alliance,” which may be helped along when President Biden visits Saudi Arabia and Israel in mid-July.

- Even though the new initiative appears to be in its early stages, other recent events suggest Israel may be preparing to attack Iran’s nuclear weapons facilities as that country gets ever closer to having a workable bomb, just as it took out Iraq’s nuclear reactor in 1981 and Syria’s in 2007. Any such attack would likely spark a global crisis that would push oil prices dramatically higher and cause a steep decline in economic activity.

- Israeli Prime Minister Bennett has recently referred to a new “Octopus Doctrine,” relating to Iran, saying, “We no longer play with the tentacles, with Iran’s proxies: We’ve created a new equation by going for the head.”

- In recent weeks, Israel has also carried out several targeted assassinations in Iran itself, taking out top Iranian military operatives as well as nuclear scientists. It is not the first time that Israel has taken out high-level targets inside Iran, but the increase in strikes suggests a shift.

- Israel has also recently stepped up its military exercises designed to increase its readiness and prepare for a conflict that would involve long-range air attacks on its enemies. Israeli media report a May exercise was explicitly designed to practice a long-range attack on Iran’s nuclear facilities.

- Other Israeli media reporting says the country’s air force can now fly F-35 fighter jets from Israel to Iran without refueling. Those jets can also be equipped with a new one-ton bomb “that can be carried inside the plane’s internal weapons compartment without jeopardizing its stealth radar signature.”

U.S. Housing Market: Reflecting the difficulty in buying a house amid today’s hot home market and rising interest rates, people trying to rent are now getting into bidding wars. That could help push up rental housing costs in the consumer price index and worsen or prolong today’s high inflation rate.

U.S. Regulatory Policy: While Friday’s Supreme Court decision voiding Roe v. Wade and its recognition of a constitutional right to abortion continue to generate intense debate, we suspect it won’t have any immediate, broad impact on the economy or financial markets (our key focus). However, it probably puts particular companies at risk of legal or political blowback, depending in large part on their public statements regarding the issue and their healthcare benefit policies.

- In the coming months, the key issue for investors may be whether the decision will energize left-leaning abortion rights voters enough to limit the Democratic Party’s expected losses in the Congressional elections in November.

- In the longer term, it will also be interesting to see whether overturning Roe v. Wade saps or bolsters the political energy of right-leaning cultural conservatives. On the one hand, the decision satisfies a longstanding goal of those voters, even if decisions on implementing or expanding abortion restrictions will now move to many state legislatures. On the other hand, right-wing elite politicians may try to capitalize on the victory by doubling down on other social issues important to populists, such as gun rights or history teaching in schools.

COVID-19: Official data show confirmed cases have risen to 543,646,378 worldwide, with 6,329,214 deaths. The countries currently reporting the highest rates of new infections include the U.S., Taiwan, Germany, and Brazil. (For an interactive chart that allows you to compare cases and deaths among countries, scaled by population, click here.) In the U.S., confirmed cases have risen to 86,967,639, with 1,015,938 deaths. In data on the U.S. vaccination program, the number of people considered fully vaccinated now totals 222,123,223, equal to 66.9% of the total population.

- In the U.S., the latest wave of infections appears to be topping out, but hospitalizations are still accelerating with their usual lag. The seven-day average of newly reported cases stands at 102,818, unchanged from two weeks ago. The seven-day average of people hospitalized with confirmed or suspected COVID-19 came in at 31,650 yesterday, up 7% from two weeks earlier. New COVID-19 deaths are now averaging 348 per day, up 5% from two weeks earlier.

- In China, the electronics manufacturing powerhouse of Shenzhen has partially locked down a district bordering Hong Kong after almost a dozen local cases were discovered there over the weekend. Illustrating how President Xi’s zero-COVID policy continues to disrupt the economy, the Shenzhen shutdown applies to businesses like wholesale markets, bars, cinemas, gyms, parks, and some bus and subway services.

- Under the new rules, anyone wanting to use public transport or enter public venues in Shenzhen must show a negative COVID test taken within the previous 24 hours—literally once a day.

- The daily test requirement has reportedly helped the city government avoid a more extensive lockdown, but we suspect it will still crimp economic activity in the region, further weighing on Chinese growth and global demand.