Daily Comment (June 17, 2022)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Note: the markets and our office are closed on Monday, June 20, in observance of the Juneteenth holiday. Our next report will be published on Tuesday, June 21.

Today’s Comment starts with a discussion about Thursday’s steep sell-off in equities. Next, we review the latest news from Ukraine followed by a brief overview of market headlines, including the BOJ’s policy decision, rising mortgage rates, and new details about the ECB’s anti-crisis tool. Finally, we wrap up the report with our daily COVID coverage.

About yesterday: On Thursday, equity prices slumped, the dollar weakened, and bond prices rose as investors continued to de-risk their portfolios. Recession worries are rising, triggering this caution. Even Energy, the best performing sector this year, has declined 12% over concerns that the industry will face windfall profit taxes. Although the likelihood of a recession is elevated, we note that a recession isn’t likely this year.

- Default rates have not shot up drastically over the last few months. The S&P/Experian Consumer Credit Default Composite Index shows that consumer defaults are still well below the level they were in 2020.

- Firms are hiring at a solid pace. The latest payroll report showed that the U.S. economy added 390,000 jobs in May, well above the 10-year median of 218k. The modest rise in initial claims is nowhere near an area of concern.

- The financial system remains stable. We have been concerned that crypto may have infiltrated the traditional banking system, but the fact that we haven’t seen signs of stress despite a collapse in cryptocurrencies is a positive sign. We remain vigilant, but so far, so good.

That said, equities may receive a boost today due to the expiration of stock options, stock index futures, and stock index options contracts on the same day, also known as the quarterly triple witching. Set to expire are $3.5 trillion worth of options, which could lead to some short-covering.

Russia-Ukraine update: European leaders met with Ukrainian President Volodymyr Zelensky on Thursday to reaffirm their commitment to the country’s military effort. During the visit, Zelensky emphasized that an attack on Ukraine is an attack on all of Europe. He said that although he is committed to his country joining the European Union, Ukraine still needs more weapons to defend itself. Meanwhile, Russia is growing more confident that it will take over Donbas. Kremlin spokesperson Dmitry Peskov claimed that Russian soldiers are being welcomed by residents within the regions. However, in what appeared to be a concession, Peskov admitted that Russia’s intention to occupy other territories in Ukraine, specifically Odesa, Kharkiv, and Kherson, will depend on the “will of local people.” The comment seemed to suggest that Russia may be satisfied with just taking over Donbas and Luhansk. If true, it would be a remarkable scale-down of its initial aim to conquer the entire country. In another sign of de-escalation, Peskov signaled that Russia would not retaliate against Baltic countries that apply to join NATO.

It will be difficult for the West to support the war in the long run if Russia maintains this stance. The war has pushed inflation higher in most countries, forcing central banks to tighten monetary policy to restore price stability. Rising interest rates and prices have already slowed the global economy and may tip some countries into recession, which is why the West may be open to compromise. Assuming Moscow will stop its invasion in exchange for control over the Donbas and Luhansk regions, the West could push Ukraine to engage in ceasefire talks. Zelensky will likely not be happy, but he may not have any choice but to negotiate given his dependence on the West for weapons. French President Macron has already hinted that he does not want to see Putin humiliated by this conflict. Meanwhile, politicians in the U.S. are growing skeptical of helping Ukraine fight a war indefinitely. As a result, we believe that an off-ramp is forming in the conflict, which should offer some relief to equities.

- More European countries are reporting problems receiving gas supplies from Russia. On Wednesday, Gazprom stated that turbine issues have made it difficult to deliver LNG to Germany and Italy. On Thursday, Slovakia and Austria also reported having their supplies cut from the state-owned energy company. Europe believes the moves are political retaliation for its support of Ukraine and could force the bloc to accelerate plans to wean itself from its reliance on Russia. As a result, the lack of supply has pushed natural gas prices upward.

- Moldova and Ukraine received candidate status to join the European Union.

Mortgage rates: U.S. home mortgages rose to their highest rate since 2008. According to Freddie Mac, the average interest rates on 30-year mortgages rose by more than half a percentage point to 5.78%. The rise in mortgage rates is due to heightened inflation concerns. Thus, the sharp rise in mortgage rates will likely contribute to a slowdown in home prices.

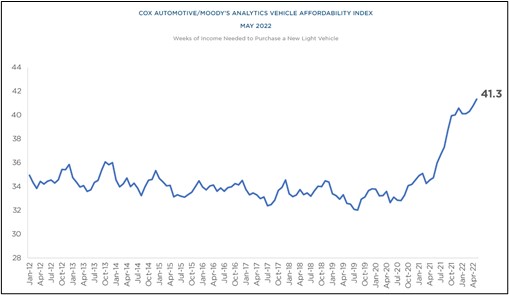

- In slightly related news, research from Cox Automotive showed that the typical new car payment could be as high as $712 a month due to rising interest rates and car prices. The decline in new-car affordability will likely dampen demand for auto purchases. Cox data shows it takes 41.3 weeks of income for the typical person to afford a new car.

Bank of Japan: The BOJ held firm in maintaining its ultra-easy monetary policy. Although there were no expectations that the central bank would raise interest rates, there was speculation that the yen’s weakness could pressure the BOJ to change its yield curve control strategy. The yen slumped following the news of inactivity from other central banks. Bank Governor Haruhiko Kuroda stated that the central bank will take appropriate action to decrease bond market liquidity but will avoid tightening monetary policy because it does not want to place downward pressure on the economy.

- The Bank of Japan would take huge losses on its balance sheet if it were to end monetary easing. According to research from Bloomberg, an upward shift in the yield curve of 100 bps could lead to a $219 billion loss on the BOJ’s holdings.

European fragmentation: The ECB announced it would fund the purchase of bonds through the sale of securities within its portfolio. The central bank wants to prevent bond yield spreads between Eurozone members. The bank will look to prevent widening by purchasing bonds of periphery countries. In related news, Klaas Knot, a member of the ECB Governing Council, stated that he expects rates to increase by 2.00% by 2023. The ECB is currently walking a thin line on its monetary policy by trying to raise rates without leading to another debt crisis. At this time, we are paying close attention to the situation.

China sales slump: A major Chinese retailer expressed concern about consumer reluctance to shop. The drop in sales suggests that consumer confidence is still low after easing COVID restrictions. If this continues, the lack of demand could lead to weaker economic growth in China.

COVID-19: Official data show confirmed cases have risen to 537,736,109 worldwide, with 6,315,979 deaths. The countries currently reporting the highest rates of new infections include the U.S., Taiwan, Australia, and Germany. (For an interactive chart that allows you to compare cases and deaths among countries, scaled by population, click here.) In the U.S., confirmed cases have risen to 86,050,615, with 1,013,006 deaths. Regarding the U.S. vaccination program, the number of people considered fully vaccinated now totals 221,924,152, equal to 66.8% of the total population.

- The WTO agreed to ease patent restrictions on vaccines to allow manufacturers to make and export more shots to countries in need.