Daily Comment (June 11, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with takeaways from the latest CPI report and its implications for monetary policy. We then provide an update on the US-Iran conflict, followed by an analysis of the oil markets. Next, we briefly cover PIMCO’s growing concerns regarding financial weakness, Anthropic’s latest funding round for its AI buildout, and the ECB’s decision to hike interest rates. As always, we conclude with a review of recent domestic and international economic data.

Inflation Problems: Less than a week before Kevin Warsh will chair his first Federal Reserve meeting, policymakers appear to be confronting a renewed inflation problem. The latest CPI report showed headline inflation accelerated to 4.2%, its third consecutive monthly increase and its fastest pace in more than three years. This pickup in inflation is likely to complicate plans for a Fed chair who had previously signaled openness to rate cuts and could instead strengthen the hand of a Federal Reserve Board that has grown more inclined toward further tightening.

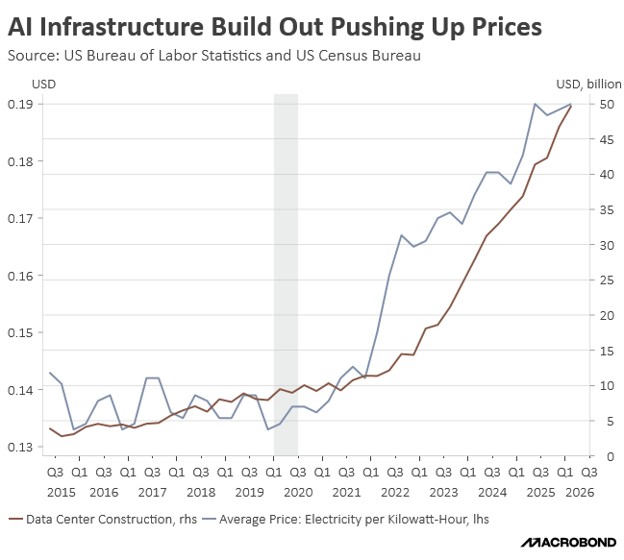

- In May, energy prices were the main driver of the latest CPI upturn, reflecting both the Iran-related supply shock and surging power demand from the AI buildout. Gasoline prices jumped 40.5% year over year, while fuel oil and other household energy costs climbed an even steeper 58.9%. Although such extreme moves are likely to normalize over time, a more troubling development is the nearly 6% increase in electricity prices, which appears increasingly tied to the growing power needs of data centers.

- The pickup in inflation is likely to complicate Kevin Warsh’s efforts to set a monetary stance that accommodates the AI buildout. He has argued that the Fed should be willing to hold rates steady and allow a prospective AI‑driven productivity boom to show up in the data. Yet, the recent energy‑price surge associated with that same buildout risks having the opposite effect, forcing Warsh to persuade more hawkish officials to tolerate above‑target inflation in the meantime.

- May’s inflation data is likely to harden the stance of many Fed officials, several of whom only a month ago had pressed the central bank to drop its easing bias and openly entertain the prospect of a rate hike. Market pricing has moved in tandem — overnight rates have swung from implying a 25-50 basis point cut at the start of 2026 to instead assigning a roughly 70% probability to at least one hike by year end at the time of writing.

- While the latest CPI report likely gives the Fed cover to delay any rate cuts, we remain less convinced than fed funds futures that policymakers will deliver a hike this year. The 2023 episode showed the Fed’s willingness to treat a rise in 10‑year yields as a substitute for additional tightening at the front end, plus, given today’s split among officials and the current chair’s leanings, an extended pause looks more likely than an outright hike as the conflict plays out.

Ceasefire in Jeopardy? The US has escalated its military operations in Iran, reflecting growing impatience over stalled negotiations to reopen the Strait of Hormuz. Iran has retaliated by targeting other Gulf states and signaling its intent to further restrict access to the waterway. The renewed hostilities follow a breakdown in talks that had appeared close to a resolution just weeks earlier. As anticipated, the escalation is likely a strategic effort by both sides to strengthen their bargaining positions and extract additional concessions in forthcoming negotiations.

- Following the latest round of strikes, which lasted roughly four hours before pausing, the president stated that military operations will continue until Iran agrees to peace terms. While several issues remain unresolved, the primary sticking point appears to be US demands that Iran dismantle or relinquish its uranium stockpiles. Iran, in turn, has held firm on securing the unfreezing of approximately $10 billion in assets, along with a ceasefire in Lebanon, as preconditions for any agreement.

- Investors had taken comfort from Washington’s reluctance to abandon the ceasefire, reflecting concerns that a broader escalation could prove difficult to control given Iran’s ability to sustain strikes even after significant damage to its military capabilities. At the same time, although there has been speculation that US forces could reopen the strait with a more substantial ground presence, the White House appears wary of the domestic political backlash that a visible troop deployment could trigger.

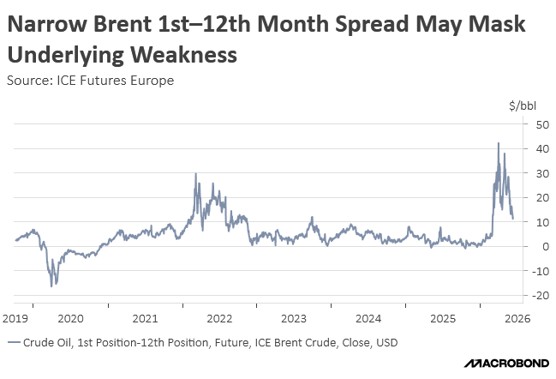

- The stop‑start pattern of strikes between the two sides has added to the volatility in crude, but it has also helped prevent prices from revisiting the peaks seen at the onset of the conflict. One area we have been watching closely is the spread between futures and physical barrels. While that spread has narrowed, the move appears driven less by easing tensions and more by buyers pulling forward deliveries amid concerns about future disruptions, even as some suppliers continue to face resistance in selling into Asian markets.

- While the worst may be behind us, we are reluctant to say that oil prices will normalize anytime soon. For one, it still appears that the US and Iran will continue to trade strikes even as they hold talks. Second, the spread between crude futures and the physical market suggests that near‑term demand and delivery concerns are outweighing any longer‑term optimism about a lasting deal, leaving room for another step higher in prices if negotiations fail in the coming weeks.

PIMCO Fears: PIMCO has reiterated its warning that a credit loss cycle may be approaching. In its latest outlook, the firm cautions that the AI buildout could leave lower‑quality borrowers particularly exposed to defaults. While credit spreads remain near historical lows, PIMCO flags the growing use of maturity extensions and payment‑in‑kind structures — where interest is paid with additional debt — as key red flags. Even so, there are still no clear, broad‑based signs of credit deterioration at this stage.

AI Debt: Apollo and Blackstone have partnered with Broadcom to help Anthropic finance additional chips for its AI buildout. The deal involves roughly $35 billion to fund purchases of Google‑designed chips that Broadcom helped develop. The arrangement highlights both the growing reliance on credit and the increasingly circular financing needed to support the AI infrastructure boom. While this may bolster near‑term growth, it also reinforces concerns about the longer‑term sustainability of the current investment cycle.

ECB Hawk: The European Central Bank raised interest rates by 25 bps for the first time in three years, marking a significant shift toward tighter policy. The move comes as the euro area contends with an energy shock that threatens its ability to maintain price stability. Although the hike was largely priced in and initially met with a muted market reaction, it could offer additional support to the euro if the Federal Reserve signals a pause at its meeting next week.