Daily Comment (July 16, 2020)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EDT] | PDF

Good morning! Global equity markets are lower this morning. Chinese stocks fell hard overnight but have been very strong recently. China’s GDP data came in stronger than forecast; we may be seeing a bit of “buy rumor, sell fact” behavior in Chinese equities. Retail sales in the U.S. came in better than forecast; we cover the data below. The ECB met this morning, and there was no change in policy. The EU suffered a blow yesterday in its attempt to tame the U.S. tech sector. There is much to discuss on the policy front. We update the pandemic news. The Weekly Energy Update is available. Here are the details:

China news:

- China’s Q2 GDP roared back, rising 59.7% on a quarterly annualized basis, up 3.2% from last year. What is most remarkable about the bounce is that the level of GDP exceeds Q4 2019 by CNY 80MM. Of course, this stunning recovery was engineered through the usual policy path—a massive rise in debt and forced investment. Michael Pettis, one of our favorite China analysts, has always argued that China can have any GDP level it wants; it’s just a matter of how much debt and uneconomic investment it is willing to make. At the same time, cross-country comparisons will look like China has fully recovered from the COVID-19 event and will be used for the full benefit by Chairman Xi to promote China’s economic model as superior to Western democracy.

- China continues to face sporadic bank runs. Although China established a system of deposit insurance in 2015, it only covers deposits up to CNY 500K ($70,400). In addition, there is deep suspicion that Chinese banks are suffering from loan losses and depositors fear they could be at risk if a bank fails. Finally, social media has been the platform for spreading rumors about bank instability, causing runs even against sound banks.

Foreign news:

- The EU suffered a stunning defeat yesterday when its second highest court overturned its order for Apple (APPL 390.90) to pay €14.3B in back taxes. The EU has been trying to push for harmonization of tax rates across member nations, undermining low tax regimes such as Ireland’s. The court indicated that Ireland didn’t violate any laws because its taxing doesn’t specifically give Apple a tax break. The decision was seen as a rebuke to Margrethe Vestager, who has campaigned against U.S. tech firms on anti-trust grounds.

- The U.S. will remove a sanctions exemption related to the Nord 2 gas pipeline. This controversial pipeline will deliver Russian natural gas directly to Germany, bypassing Ukraine and Poland in the process. The U.S. worries the pipeline will make Germany overly dependent on Russian natural gas and deprive transit nations the usual fees they gather for hosting pipelines. The decision to build the pipeline has always been contentious, especially after Russia’s annexation of Crimea and its interference in eastern Ukraine.

- EU leaders are meeting on Friday through the weekend to determine if a support package and the decision to fund the Eurobond will be approved. The “frugal four,” Sweden, Austria, Netherlands and Denmark, are all expressing opposition; at a minimum, they want conditions on the grants and loans. Chancellor Merkel has thrown her support behind the measure and will meet with Greek officials before the meetings.

- There are longstanding tensions between Azerbaijan and Armenia, mainly over the disputed region of Nagorno-Karabakh (for background, see our WGR). Azerbaijan forces destroyed an Armenian military facility on the border between the two nations yesterday. Armenia is said to have killed an Azerbaijani general. Usually, Russia eventually brokers some sort of arrangement to bring an end to overt hostilities, but if it refuses to act, conditions could deteriorate further and may support oil prices.

Policy news:

- As several fiscal programs are set to expire, congressional leaders are laying their markers for what follows. Congress took aggressive steps earlier this year to offset the impact of the pandemic and the actions did prevent a deeper decline in growth. Now, leaders are trying to figure out what they should do going forward, with an eye on using the crisis to promote their longer-term policy goals. We do expect additional support, but also would not expect an agreement until the 11th hour.

- A couple of points on Fed policy:

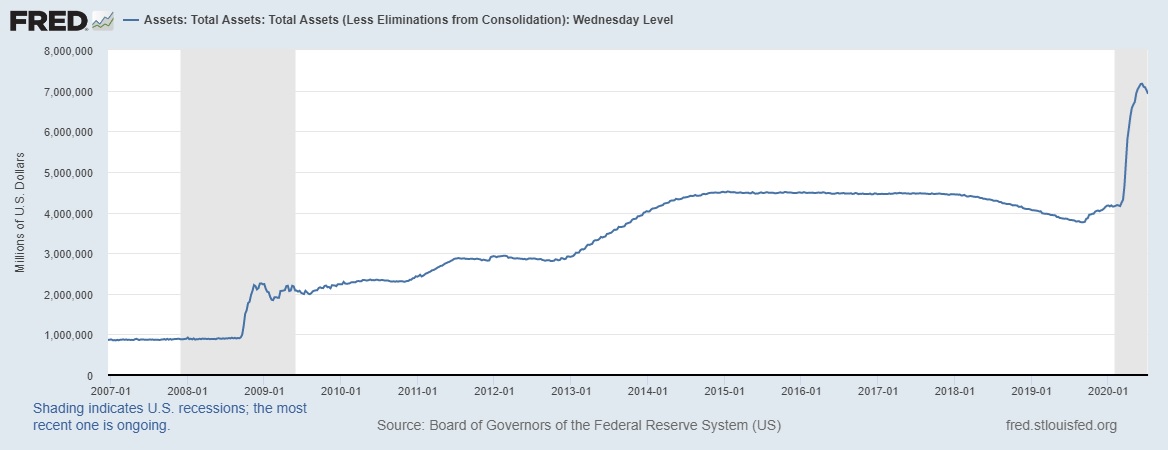

- There has been some consternation among the financial media over a decline in the Fed’s balance sheet.

Worries surrounding this decline are misplaced. The reason the balance sheet is contracting isn’t because the Fed is tightening support. It’s declining because market participants aren’t using available facilities because they aren’t needed. In other words, knowing the Fed is backstopping markets is keeping financial markets well behaved. It is worth noting that a number of facilities do have expiration dates for the end of Q3. We expect these deadlines to be extended, but even if they are not, if market participants expect the Fed to maintain low levels of financial stress then the need for actual facilities is unnecessary. Simply put, the fact that the Fed has signaled it will provide support will tend to preclude the actual need to do so because the markets will act as if the support is in place.

- As Fed officials work through a post-mortem of the crisis, the non-bank financial system is, again, seen as the fount of the overall system’s weakness. In other words, the “shadow” banking system remains vulnerable to runs and remains a source of financial instability. The Fed said its aggressive expansion of policy support was due to funding problems in the shadow system. At the same time, the non-bank system can’t really be closed because the banks won’t make loans to many areas of the economy due to the inability to scale the lending.

- U.S. sanctions on Hong Kong are putting global financial banks in a difficult position; essentially, it will be impossible to satisfy both Chinese and U.S. regulations. Of course, these large institutions will try to figure out what they can do to maintain operations in both jurisdictions, but it will be an additional complication.

- The USMCA included labor regulations designed to reduce Mexico’s edge in lower labor costs. Japanese auto firms are examining the laws and are trying to determine if remaining in Mexico or moving production to the U.S. makes sense in light of the changes.

COVID-19: The number of reported cases is 13,538,763 with 584,922 deaths and 7,600,418 recoveries. In the U.S., there are 3,499,394 confirmed cases with 135,205 deaths and 1,075,882 recoveries. For those who like to keep score at home, the FT has created a nifty interactive chart that allows one to compare cases across nations using similar scaling metrics. Axios has updated its state map.

Virology:

-

- We continue to closely watch the path of vaccine development; Bloomberg has a profile of Sarah Gilbert, who is spearheading Oxford’s program. Although we are heartened by the rapid developments on the vaccine front, there remain worries that the level of immunity may be limited.

- Meanwhile, Chinese firms are using their employees as testing subjects for their vaccine candidates.

Market and Economy news:

- Yesterday’s Beige Book suggested the economy is improving, but at a very gradual pace.

- As of July 13, 87.6% of apartment households paid some amount of rent.