Daily Comment (January 6, 2023)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EST] | PDF

Good morning! Today’s Comment begins with a discussion about Fed officials’ speeches and the U.S. jobs numbers. Up next, we review how rising inflation in the developed world impacts investing in emerging markets. We end the report by focusing on Russia and China’s ability to use state power to generate growth as their economies cope with headwinds.

All About Timing: Some investors are positioning themselves for a Fed Pivot, despite monetary policymakers’ insistence that they are not finished tightening.

- Fed officials reaffirmed the central bank’s commitment to tightening policy until inflation falls to its 2% target. Atlanta Fed President Raphael Bostic argued that inflation is the biggest headwind to the U.S. economy, and in an interview with CNBC, his colleague from Kansas, Esther George, added that she would like the Fed’s policy rate to rise above 5% and have it held there until 2024. Meanwhile, St. Louis Fed President James Bullard struck a moderate tone suggesting that interest rates are almost high enough to bring down inflation.

- The labor market remains too hot for the Fed. According to the Bureau of Labor Statistics, the economy added 233k jobs in December, while the unemployment rate fell from 3.7% to 3.5%. Although job creation has eased in recent months, the Fed has made it known that it would like the unemployment rate to increase before it reverses course on policy. As a result of the data, the S&P 500 dropped, and bonds rallied as it added to evidence that the Fed will need to continue tightening.

- Data suggests that the rise in hourly wages may be a side effect of elevated margins from firms. The chart above looks at the annual change in trade services, a measure of retail and wholesale margins, and average hourly wages. If we are correct, a profit margin decline should contain wage growth, relieving some inflationary pressure.

- The Federal Reserve is in a difficult position as it decides what will be the appropriate policy going forward. Although it is clear that the central bank will be ready to pause rate increases later this year, the Fed is reluctant to commit due to concerns that it might be caught flat-footed by inflation. The anticipation of the conclusion of the Fed’s hiking cycle has led investors to position themselves to take advantage of any positive surprises within the data. This behavior may have the Fed worried that financial markets are assuming that it will cut rates aggressively if the economy falls into recession. As a result, we expect policymakers to stress that a pause is not the same as monetary easing.

The Saver’s Rush: The fight against inflation in the developed world may deter overly sensitive investors from allocating capital to emerging markets.

- Inflation in the Eurozone returned to single-digit territory in December, but concern remains about persisting price pressures. The overall consumer price index rose 9.2% from the prior year, below the previous month’s increase of 10.1%. The dip in the index is related to the slide in energy prices. That said, excluding volatile elements, the index rose 5.2% from last year, a jump from the prior month’s report of a 5.0% increase. Price pressures in core components of the index will motivate the European Central Bank to raise rates by at least 50 bps at its next meeting.

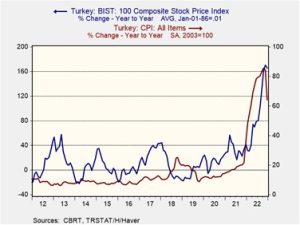

- Meanwhile, in another part of Europe, deceleration in inflation has led to a decline in equity prices. Several days after the Turkish CPI fell by more than 2000 bps, the country’s BIST 100 Composite Index sank by more than 8%. The sharp drop in the index is especially notable, given its strong performance in 2022, when Turkish equities more than doubled. Although much of the decline is related to investors locking in gains from their investments, it also reflects the tendency for investors to pull out of risky countries at the first sign of trouble.

- A lesson can be taken from the situation in Turkey. In this case, we learned that investing can be more about circumstances than solid fundamentals. As the chart above shows, the rise in the BIST 100 in 2022 was largely driven by domestic savers trying to protect the purchasing power of their holdings. Argentina’s stock market, which also performed well in 2022, is another place where this may be happening. The reason for these investments is that equities serve as a form of value storage in countries where inflation is uncontrolled. Hence, high-inflation countries may present short-term opportunities for investors looking to earn capital gains abroad. That said, as global yields begin to rise in the developed world, these countries could face financial outflows as investors become more risk averse.

Return of the State: China and Russia’s governments are intervening in their own economies to prevent backsliding.

- Beijing is pulling out all the stops to help restore faith in its economy. Chinese regulators are considering relaxing the country’s “Three Red Lines” property rules to incentivize more real estate investment. They are also exploring the possibility of raising borrowing caps and delaying the grace period for meeting debt targets. These moves are controversial as China has not fully recovered from the fallout of its property meltdown. However, these measures have added to investor confidence that Beijing will get its economy back on track after ending its draconian Zero-COVID policy.

- As a result of Beijing’s actions over the last few months, the off-shore CNY has surged 7% since October 25, when it hit the weakest level on record, and is currently trading above its 200-day moving average.

- Meanwhile, Moscow has ramped up the pressure on state-owned firms to help fund its war efforts in Ukraine. The government has called for “revenue mobilization,” in which state enterprises pay higher dividends and one-time payments to help improve the country’s fiscal budget. The order could be harmful to its coal-producing sector, which has recently returned to near high levels after Europe loosened transportation restrictions. The Russian government’s pressure on companies signals that the West’s sanctions are working to starve Moscow of the funds needed to maintain its war efforts. However, it also shows that the war is still disruptive to the commodity market.

- Recent moves by China and Russia suggest that as the world becomes more polarized, governments will look to have greater economic control. In the short term, this could benefit international equity markets as stimulus will increase domestic demand and make it easier for firms to boost production. However, as blocs and countries become isolated, firms could struggle to find the opportunities to widen their customer base. Thus, we may be headed to a world that is more favorable to real assets, such as commodities, rather than financial assets.