Daily Comment (February 9, 2018)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EST]

Looking for something to read? In our travels we are often asked about books we recommend. As a result, we have created The Reading List. The list is a group of books, separated by category, that we believe are interesting and insightful. Each book on the list has an associated review to help you decide if you want to read it. We will be adding to the list over time. Books marked with a “*” are ones we consider classics and come highly recommended.

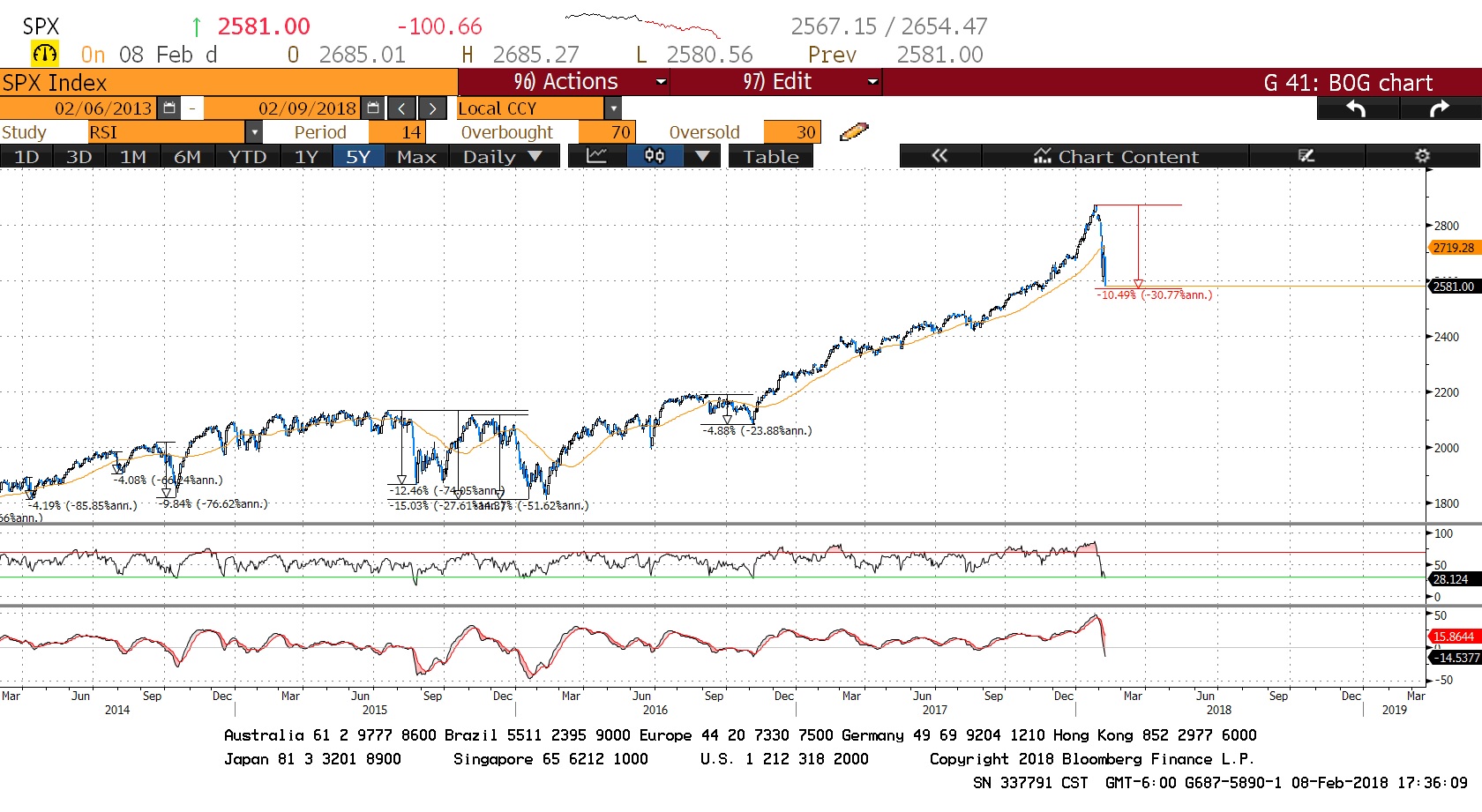

It’s official! We are in a correction. The S&P 500 has now declined just over 10% on an intraday high-to-low basis.

Do we have more downside from here? Probably not materially, although we expect more grinding around current levels before we head back higher. Next week’s CPI data will be important. If inflation does appear to be accelerating, it may trigger another downleg. Overall, the economy is still doing fine; the drop in equities might affect sentiment but it’s important to remember that nearly 85% of equities are held by households in the top 10% of income brackets. In other words, the real losses are concentrated at the top end of the income scale so, for most Americans, the gyrations in equities are not a materially negative factor.

What are we paying attention to? It is clear in the data that the last major equity market decline in the absence of recession occurred in 1987. This begs the question, “Is this another 1987 event?” At present, we don’t think so but, if it is going to be that kind of event, the trigger would probably be the use of volatility products. In 1987, portfolio insurance led to a selling effect that exacerbated the downdraft. Volatility trading won’t necessarily involve the same methods, but it could lead to similar results.

We have been getting questions on the volatility trade and note there is some confusion on how it works. It’s important to note that betting on volatility is just that—it’s essentially trying to predict when the “freight train” is coming while others pick up nickels from the tracks. To get an idea of this, we refer to the prospectus for the VXX (55.24), which says (on pages 13-14):

The long-term expected value of your ETN is zero. If you hold your ETN as a long-term investment, it is likely you will lose all or a substantial portion of your investment.

The reason is the roll yield. The long volatility products are long the front contract of the VIX futures when the term structure of the VIX futures are normally in contango, meaning the deferred futures price is above the nearest price. When the nearest contract expires, the VXX manager buys the next nearest contract at a higher price. If nothing happens, that contract will decline to where the previous contract expired, meaning the value of the positon will decline. Over the long term, that means steady losses for the holder of long volatility. So, the inverse position in volatility is in the opposite position. Their position gains over time. The anti-vol trade is really more of a roll yield position and less of a position on volatility. Now, when policymakers are dampening volatility with accommodative and transparent monetary policy, the periods lengthen between volatility spikes (when the VXX pays off, or, when the “freight train” arrives), making the anti-vol positions quite profitable.

What led to the collapse of the anti-vol ETP was not just the jump in volatility but the fact that the volatility futures term structure flipped from contango to backward. In other words, the nearest futures contract rose relative to the deferred contracts. This means that losses were being accumulated on the roll yield and on the outright short position against volatility, which pushed prices down to points where some (but not all) ETN managers, to protect losses, exercised the call provision of the note and closed their products.

The unknown is how widespread was anti-vol positioning, who was in it and how much leverage was being deployed? A casual look at the holders of XIV (0.00), the primary inverse ETN, shows a number of banks and broker dealers that were probably holding these for customers. But, a large number of hedge funds are also represented and that is where the concern lies. The fact that we are seeing selloffs in the last hour of trading may be a signal that these entities are still trying to build liquidity. We don’t think the current event is going to be another 1987 situation, but we are watching the volatility issue closely because that is the most likely source if this does turn out to be a similar occurrence.

Is there a Powell put? At present, if there is one, we are far from its strike price. Various Fed speakers have been out in recent days and none seem overly concerned about the decline in equities, and fed fund futures are still projecting the odds of a March rate hike at around 85%.

A budget: The president signed the Senate budget deal that was passed early this morning by the House and Senate. We did have a filibuster in the Senate that delayed the passage but we felt confident it would pass. The good news is that we have now removed the budget drama from the markets for a couple of years. What we have to deal with is the additional fiscal stimulus coming from the tax bill and this new spending. We expect much of the expansion to boost imports, meaning the national growth effect will not be all that impressive but it is quite good for the global economy.