Daily Comment (December 13, 2017)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EST] It’s Fed Day! Here is what we are watching this morning:

FOMC today: At 2:00, we will get a decision with certainty regarding a 25 bps rate hike. We will also get new dots and forecasts, along with Chair Yellen’s last press conference at 2:30. Usually, press conferences are important. This one really won’t be because she will exit by February. Thus, anything she says could be moot in less than two months. The debate now is whether we will get three or four hikes next year. At present, the financial markets only have two hikes discounted.

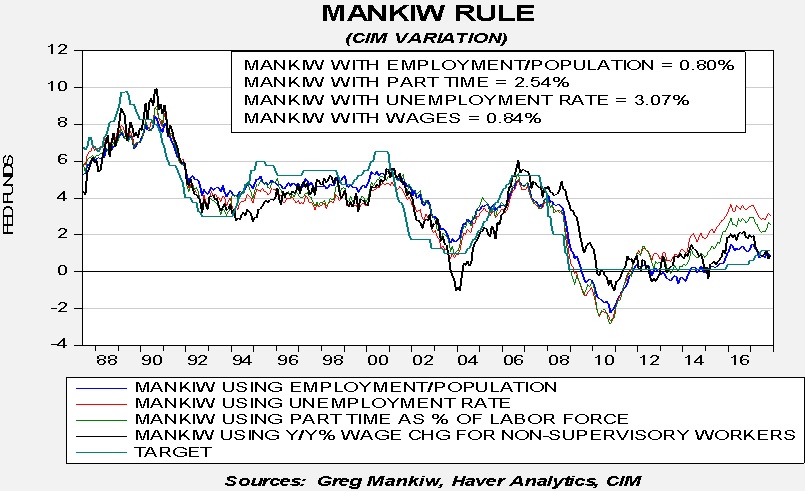

With the release of the CPI data we can upgrade the Mankiw models. The Mankiw Rule models attempt to determine the neutral rate for fed funds, which is a rate that is neither accommodative nor stimulative. Mankiw’s model is a variation of the Taylor Rule. The latter measures the neutral rate using core CPI and the difference between GDP and potential GDP, which is an estimate of slack in the economy. Potential GDP cannot be directly observed, only estimated. To overcome this problem with potential GDP, Mankiw used the unemployment rate as a proxy for economic slack. We have created four versions of the rule, one that follows the original construction using the unemployment rate as a measure of slack, a second that uses the employment/population ratio, a third using involuntary part-time workers as a percentage of the total labor force and a fourth using yearly wage growth for non-supervisory workers.

Using the unemployment rate, the neutral rate is now 3.07%. Using the employment/population ratio, the neutral rate is 0.80%. Using involuntary part-time employment, the neutral rate is 2.54%. Using wage growth for non-supervisory workers, the neutral rate is 0.84%. The fact that core CPI remains steady maintains the split within the variations. If the proper measure of slack is unemployment or involuntary part-time employment, then the FOMC lifting rates is clearly proper. On the other hand, if either the employment/population ratio or non-supervisory wage growth is the better measure, then further rate hikes are dangerous. However, in the latter two variations—employment/population ratio or non-supervisory wage growth—there is still some room to raise rates before one achieves policy tightness. Both models have a standard error between 100 to 125 bps. So, roughly, taking the policy rate target to 1.75% to 2.00% would raise the risk of recession. This is probably why the financial markets don’t expect fed funds to go above 2.00%. We will recap the meeting in tomorrow’s report.

Alabama: In an upset, Doug Jones won the special election for the remainder of Jeff Sessions’s term, which ends in 2020. Here are our takeaways:

- In the immediate term, this won’t matter a whole lot. As long as Congress gets the tax bill to the president before 2018, the GOP will maintain its two-seat majority for this key vote. However, the election makes it abundantly clear that Congressional Republicans have to get this bill done before New Year’s. If they don’t, it may be impossible to craft a bill that will placate both Bob Corker (R-TN) and Susan Collins (R-ME).

- Although losing this seat should make passing legislation even more difficult, we don’t know for sure how Doug Jones will vote. Will he follow the dictates of his caucus, reducing the chances of holding the seat in two years, or will he vote mostly as a Republican in a bid for re-election? Despite last night’s outcome, Alabama remains a deeply red state and only a confluence of circumstances led to Jones’s win. It may make no difference how he votes as to whether he retains the seat. It is important to remember that the last time a Democrat won a Senate seat in the state, he changed party affiliation afterward.[1] At the same time, it is reasonable to expect Jones to be more conservative than Dianne Feinstein (D-CA).

- The divisions in the GOP were laid bare by this election. The establishment/populist political division is something we have noted since 2014. It affects both parties. One of the characteristics we have noted about populist candidates is that they are often significantly flawed. The political establishment is sort of a “finishing school” for political candidates. Usually, establishment political figures “move up the ladder” through lower level office elections; large corporations perform similar grooming for their executives when they move up the organizational chart. Populists tend to simply come into the political sphere due to popular anger; President Trump is a classic archetype. Roy Moore did win offices but, in something of a political “hothouse” in Alabama politics, that didn’t expose him to the rigors of national political life. Thus, his alleged activities that were highlighted in this special election campaign were simply not exposed by the local media. Steve Bannon has become the de facto leader of the right-wing populists. It appears that he, or his organization, lacks the ability to properly vet potential candidates. Simply put, this loss was an “own goal” for the GOP; Luther Strange would have probably held the seat easily. As a result, this is vindication for Senate Majority Leader McConnell (R-KY) and, to some extent, might be a welcome outcome to the GOP establishment.

- Although the GOP has struggled in recent elections, the Senate election calendar still strongly favors the Republicans in 2018. Twenty-three Democrats and the two independents who caucus with them are up for reelection next year, while only eight Republicans face elections. A number of pundits are trying to argue that Jones’s win suggests Republicans everywhere are in trouble, but this is probably reading too much into a single election. Roy Moore was a controversial candidate even before the recent allegations emerged. If the right-wing populists put up a slate of similar candidates, similar outcomes are obviously possible. But, this outcome should lead the right-wing establishment to “take the wheel.”

- Elections are becoming almost impossible to call. Polling before this election was literally all over the place. The prediction markets, which have tended to be more reliable, missed this one by a mile. We believe a major factor in recent elections is “preference falsification.” In other words, respondents are simply lying to pollsters because they feel uncomfortable telling the truth. A joke during the 2016 presidential election was, “How do you tell the pollster you are voting for Trump with your wife within earshot?” The version during this election may have been, “How do you tell the pollster you are voting for Jones with your husband in the room?” However, preference falsification doesn’t resolve the prediction market issue. After all, lying simply means you lose money. But, it may show that money distorts the market. For example, we know that Remain looked likely to win in the Brexit vote, but the brokers noted in the aftermath that Remainers had put larger individual wagers on that side but there were more small-sized punters on Leave. We may have seen a similar outcome here.

- Overall, Jones’s win will increase the odds of gridlock next year but, frankly, the financial markets will probably welcome that outcome because (a) the president can use executive orders and selective enforcement to deregulate, and (b) nearly all the concern was on taxes and, if that passes as we expect, anything after that is anticlimactic.

North Korea: SOS Tillerson told Pyongyang that he would be willing to talk “without preconditions.” At the same time, the White House is reportedly asking China to ramp up sanctions and pressing for an oil embargo. Given Tillerson’s tenuous position in the administration, his offer for talks may not have legs but it bears watching if North Korea takes him up on the offer.

[1] Sen. Shelby won in 1992, then became a Republican in 1994.