Daily Comment (December 11, 2017)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EST] It was a quiet weekend in front of an active week. Here is what we are watching this morning:

NYC bombing: This is a developing incident but early reports suggest a pipe bomb or similar device was detonated near Times Square. According to early reports, there are four non-life threatening injuries and a man is in custody. At least three subway lines have been shut down. We saw the typical market reaction—equities suffered a mild selloff and Treasuries rallied. This doesn’t appear to be a major situation, at present, and if there are no follow-on incidents we would expect the flight to safety buying to reverse in the later hours of the morning.

Central bank week: The ECB, Fed and BOE all meet this week. The FOMC is expected to raise rates 25 bps on Wednesday. We will get new economic forecasts and dots plots; it will also be Chair Yellen’s last scheduled press conference. No action is expected from the ECB or the BOE, although the latter may set the stage for another rate hike.

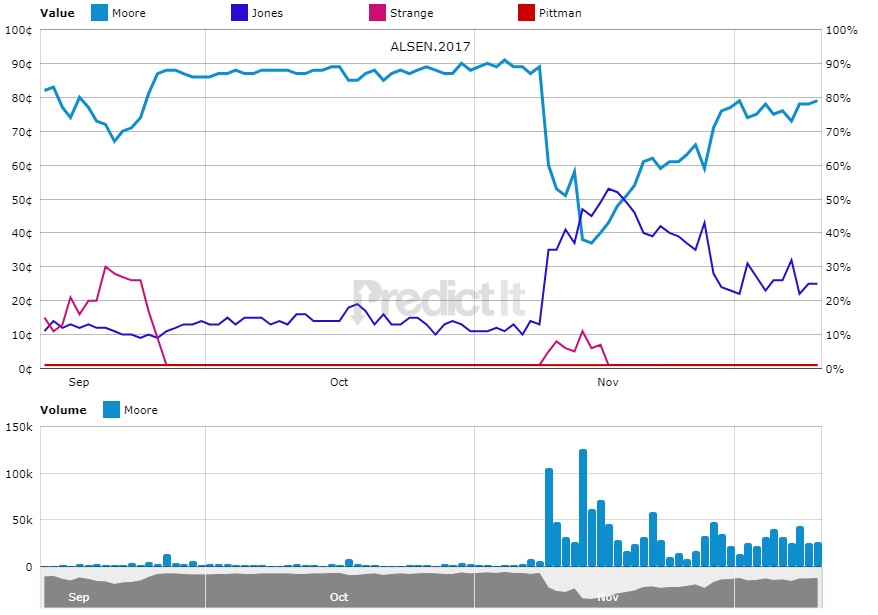

Alabama special election: Although polling suggests Democrat Party candidate Jones is gaining ground, the prediction markets are solidly indicating that GOP candidate Moore will win easily.

If the prediction markets are correct, in the short run, it’s a bonus for the GOP as it holds the Republicans’ narrow majority. The long-run implications may be less sanguine as one would expect the Democrats to use the controversy surrounding Moore as a way to boost their chances at the mid-terms.

Tax bill: Conference committee negotiations continue this week. The president will offer his “closing arguments” on Wednesday. Passage of something is likely but the final package could be rather muddled. The haste to put the bill together will almost certainly yield some unexpected outcomes, both positive and negative. But, until the final bill emerges, projections of what it will do are highly susceptible to error.

Negative nominal interest rates remain: The FT[1] reports there are $11.2 trillion of financial instruments with negative nominal yields, the highest reading since August. Although the FOMC is clearly tightening U.S. monetary policy, this data shows the effect of accommodative policy in Japan and Europe. These negative rates are keeping U.S. long-duration interest rates lower than they would be otherwise; therefore, we should see the negative nominal rate number ease when the ECB begins to reduce accommodation. This outcome may have a modestly bearish impact on long-duration U.S. debt.

[1] https://www.ft.com/content/0217091e-af9f-3884-96b1-0071016392ae