Daily Comment (December 14, 2021)

by Bill O’Grady, Thomas Wash, and Patrick Fearon-Hernandez, CFA

[Posted: 9:30 AM EST] | PDF

Note to readers: The Daily Comment will go on holiday after Friday’s comment and return on January 3, 2022. From all of us at Confluence Investment Management, have a Merry Christmas and Happy New Year!

In today’s Comment, we open with a review of key U.S. news, including an update on the weekend’s tornadoes, the status of President Biden’s latest fiscal program, and the opening of the Federal Reserve’s policy meeting today. We next deal with a range of international news, including the recent U.S. pushback against China’s aggressive geopolitical moves. We wrap up with the latest developments regarding the coronavirus pandemic.

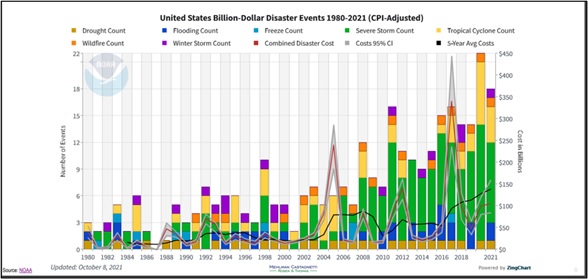

U.S. Tornado Toll: The number of confirmed fatalities from last weekend’s tornadoes rose to 88, with the vast majority of the deaths in Kentucky. So far, we haven’t seen an estimate of insurable loss damages, but it could be high. Although meteorologists believe the unusually powerful storms for this time of year had their origin in extraordinarily warm temperatures, they couldn’t yet tie them directly to global warming. All the same, we note that as global temperatures trend upward, the increased heat in the atmosphere has coincided with a rise in particularly devastating storms, especially over land, as shown in the graph below.

U.S. Fiscal Policy: President Biden lobbied Senator Joe Manchin of West Virginia by phone yesterday in another effort to garner the senator’s support for the Democrats’ $1.75 trillion “Build Back Better” social policy and climate change legislation. However, neither side reported any breakthrough, other than agreeing to talk again in the coming days.

U.S. Monetary Policy: Today, the Fed begins its latest two-day policy meeting. When the new policy statement is released tomorrow, the officials are expected to say they will accelerate the tapering of their bond-buying to end the program by March, which would position them to start hiking the benchmark fed funds interest rate in the first half of the year if they so choose. However, Chair Powell’s abrupt mutation into an inflation hawk has some investors nervous about what the policymakers will actually do at the meeting. Until the decision is out, it could lead to further volatility in the markets as it did yesterday.

- As we noted in our Comment yesterday, most major central banks are holding a policy meeting this week, but their expected policy actions range widely. Importantly, the IMF warned in its latest review of the British economy that the Bank of England is already behind on tamping down inflation pressures and must not delay rate hikes, even as the fast-spreading Omicron mutation of the coronavirus has some observers thinking the central bank might punt on rate hikes this week.

- Separately, the Canadian government and the Bank of Canada yesterday agreed to renew the central bank’s mandate to target 2% annual inflation, with a new emphasis on giving the central bank flexibility to address economic challenges and help obtain full employment when conditions warrant.

- Under the renewed mandate, which runs until the end of 2026, the central bank will set rate policy to achieve 2% annual inflation or the midpoint of a 1% to 3% target range.

- The bank will have flexibility in rate setting to achieve “maximum sustainable employment . . . The central bank will utilize the flexibility of the 1% to 3% range only to an extent that is consistent with keeping medium-term inflation expectations well anchored at 2%.”

United States-China: In a major policy speech delivered in Jakarta, Secretary of State Blinken criticized “Beijing’s aggressive actions” against its neighbors and reaffirmed Washington’s commitment to an Indo-Pacific region “free from coercion and accessible to all.”

- Blinken said the U.S. plans to strengthen its treaty alliances with Japan, South Korea, Australia, the Philippines, and Thailand in order to counter China’s aggressive geopolitical moves. In addition, he said the Biden administration is developing a “comprehensive Indo-Pacific economic framework” that would include co-operation on trade, the digital economy, technology, supply chain resilience, and investments in decarbonization.

- Although the speech broke little new ground, it drew a sharp rebuke from the Chinese government, which understands that its effort to build up Chinese power and geopolitical influence could be hemmed in to the extent that foreign nations understand the threat they face from China.

United States-China-Japan: Elaborating on comments he made earlier this month, former Japanese Prime Minister Abe said that any Chinese attack on a U.S. military vessel in a contingency concerning Taiwan could become a situation allowing Japan to exercise the right of collective self-defense, i.e., military action. Pointing out that Yonaguni Island — Japan’s westernmost territory — is only 110 kilometers away from Taiwan, Abe said, “If something happens here, it will definitely become a crucial situation” affecting Japan’s peace and security as stipulated in the country’s security legislation. The statement points to a growing realization in Japan that the country faces a severe security risk from China and needs to strengthen its alliance with the U.S. to counter it.

Norway: NATO General Secretary Jens Stoltenberg said he has applied to become the governor of Norway’s central bank starting next October. Stoltenberg, who formerly served as Norway’s prime minister, and finance minister before that, is a political heavyweight who would likely be a front-runner for the position, along with current deputy governor Ida Wolden Bache.

- Stoltenberg’s supporters have said that having a political heavyweight in the role would be desirable and that few understand Norway’s economy as well as Stoltenberg, who, as finance minister, came up with the spending rule that decides how much government can take out of the oil fund each year. Stoltenberg’s leadership of the central bank would likely be well received by investors.

- In contrast, however, Stoltenberg’s critics argue that the credibility of both Norges Bank and the country’s sovereign wealth fund would be placed at risk by putting a former politician — and one who is close friends with current Labor leader and prime minister Jonas Gahr Støre— in charge.

Global Supply Chains: Data from the OECD indicate corporate capital investment fell in the U.S., Canada, Japan, Germany, South Korea, the Netherlands, and Switzerland during the third quarter, despite the excess of demand over supply that’s driving up prices worldwide. The causes of the slowdown appear mixed. Many businesses cite price rises, supply-chain problems, and uncertainty regarding how long the surge in consumer spending will last.

COVID-19: Official data show confirmed cases have risen to 270,933,004 worldwide, with 5,316,286 deaths. In the U.S., confirmed cases rose to 50,120,820, with 798,722 deaths. (For an interactive chart that allows you to compare cases and deaths among countries, scaled by population, click here.) Meanwhile, in data on the U.S. vaccination program, the number of people who have received at least their first shot totals 239,274,656. The data show that 72.1% of the U.S. population has now received at least one dose of a vaccine, and 60.9% of the population is fully vaccinated.

Virology

- U.K. officials reported the first death of someone infected with the Omicron mutation and the hospitalization of at least ten others. The government continues to raise the alarm about a massive wave of Omicron infections and the potential need to impose strict new lockdowns to combat them. In Denmark, Omicron is already driving record-high infections and is expected to become the dominant strain this week.

- Chinese officials also reported their country’s first Omicron infection. The infection was discovered in a traveler who arrived in the northern port city of Tianjin from overseas last Thursday. Later, state television reported that a second Omicron case was discovered in the southern city of Guangzhou, raising fears that the government might clamp down on factory activity and further snarl global supply chains under its “zero-tolerance” COVID-19 policy.

- In the U.S., an administration official warned that an “explosion” of new COVID-19 cases driven by Omicron is now imminent. Even though most cases won’t be severe, the sheer number will ensure that hospitalizations will surge and put further stress on the nation’s healthcare system.

- In California, the state government will again require masking in all public indoor settings, regardless of vaccination status, as it confronts rising case rates ahead of the winter holidays and uncertainty about the Omicron variant.

- To encourage vaccinations, grocery chain Kroger (KR, $45.63) said it would no longer provide two weeks of paid emergency leave for unvaccinated employees who contract COVID-19 unless local jurisdictions require otherwise. The company will also add a $50 monthly surcharge to company health plans for unvaccinated managers and other non-union employees.

- Based on final trial results, Pfizer (PFE, $55.20) said its antiviral treatment for COVID-19 cuts the risk of hospitalization or death by up to 89% in high-risk patients.

- The trial was held while Delta was the dominant variant, but Pfizer said early lab work suggested the antiviral will continue to work against Omicron, and other studies are underway.

- Pfizer’s apparent success with its antiviral, known as Paxlovid, underlines how the scientific community is broadening its toolkit against the coronavirus. Not only have the vaccines proven to be safe and effective in preventing the most serious illnesses from COVID-19, but now antiviral treatments are starting to prove their worth in managing the disease among those who get infected. Since that provides hope that society can eventually live relatively comfortably with the virus, it’s a positive for the global economy and risk markets, at least as long as a dangerous new mutatios doesn’t arise.

Economic and Financial Market Impacts

- In its monthly report, the International Energy Agency predicted that the Omicron mutation will only modestly reduce global oil demand in the coming months. Coupled with rising output in both OPEC and non-OPEC countries, that should help bring the market back into balance and eliminate the recent tightness that drove up prices earlier this year, according to the IEA.