Daily Comment (August 3, 2017)

by Bill O’Grady and Thomas Wash

[Posted: 9:30 AM EDT] Washington is shutting down for August, earnings remain solid and news flow is rather quiet. Here’s what we are watching today.

BOE holds steady: The BOE held everything steady. Its QE remains in place and rates were left unchanged. The Monetary Policy Committee (MPC) voted 8-0 to keep buying Gilts but had two dissenters on rates, with two wanting hikes. BOE Governor Carney warned that inflation is rising but also noted that wages are not keeping pace, meaning real wages in the U.K. are contracting. This situation puts the BOE in a difficult spot; if it raises rates to ease inflation it will further harm households seeing weak wage growth, but if it allows inflation to keep rising it will further cut real wages unless wage growth improves. We do expect rates to rise in the U.K. in the coming year but, like here, the pace of hikes will be slower than in the past. The GBP fell sharply on the news and Gilt yields declined.

A “clean” debt ceiling hike? Politico is reporting[1] that Senate Majority Leader McConnell and House Speaker Ryan are quietly trying to build a coalition of centrists from both parties to pass a straight increase in the debt ceiling. This would avoid spending cuts from the Freedom Caucus and spending amendments from Democrats. It isn’t clear if such a coalition is possible. On the one hand, the debt ceiling is obscure enough that progressive opposition probably won’t be strong. On the other hand, creating this coalition will isolate the Freedom Caucus and highlight internal GOP divisions. Another complication is that the Democrat Party leadership will be sorely tempted to pay back the GOP for the series of debt ceiling crises President Obama endured. And, that same leadership doesn’t want to pass a clean bill only to see the GOP push tax cuts on them soon after. So far, financial markets expect smooth sailing on this issue; we remain concerned.

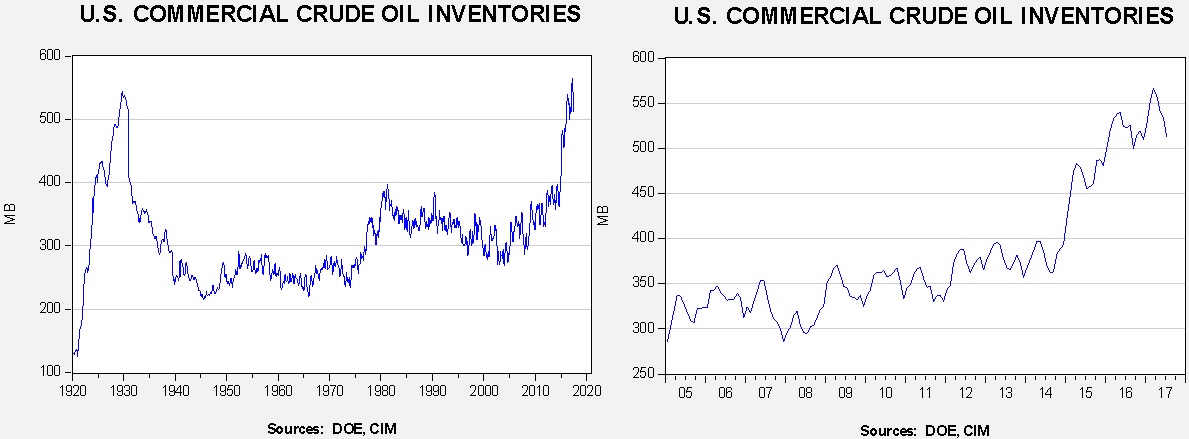

Energy recap: U.S. crude oil inventories fell 1.5 mb compared to market expectations of a 3.3 mb draw.

This chart shows current crude oil inventories, both over the long term and the last decade. We have added the estimated level of lease stocks to maintain the consistency of the data. As the chart shows, inventories remain historically high but they are declining. Again this week there was no oil sold out of the Strategic Petroleum Reserve. The authorized sale is nearly complete, as 16.2 mb have been released out of an authorized 17.0 mb.

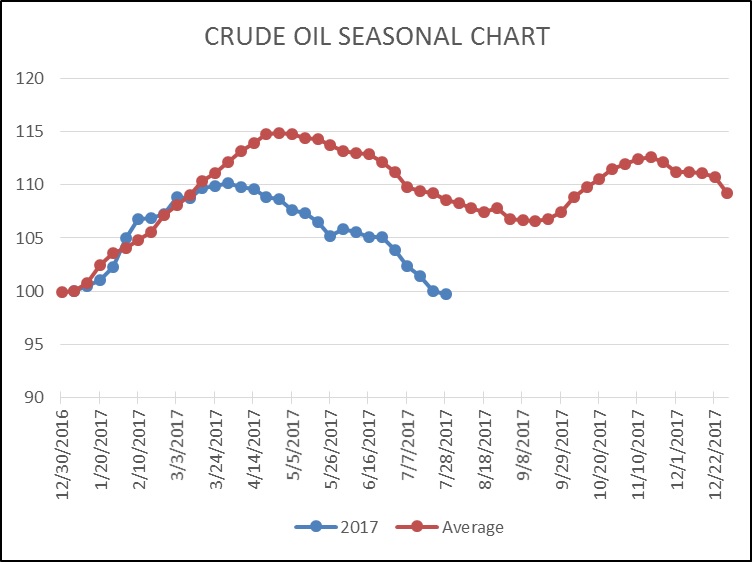

As the seasonal chart below shows, inventories are usually well into the seasonal withdrawal period. Even with the SPR sales, we have already seen a larger than normal seasonal decline; the seasonal trough isn’t usually hit until mid-September. Thus, we should see further stock withdrawals over the next six weeks.

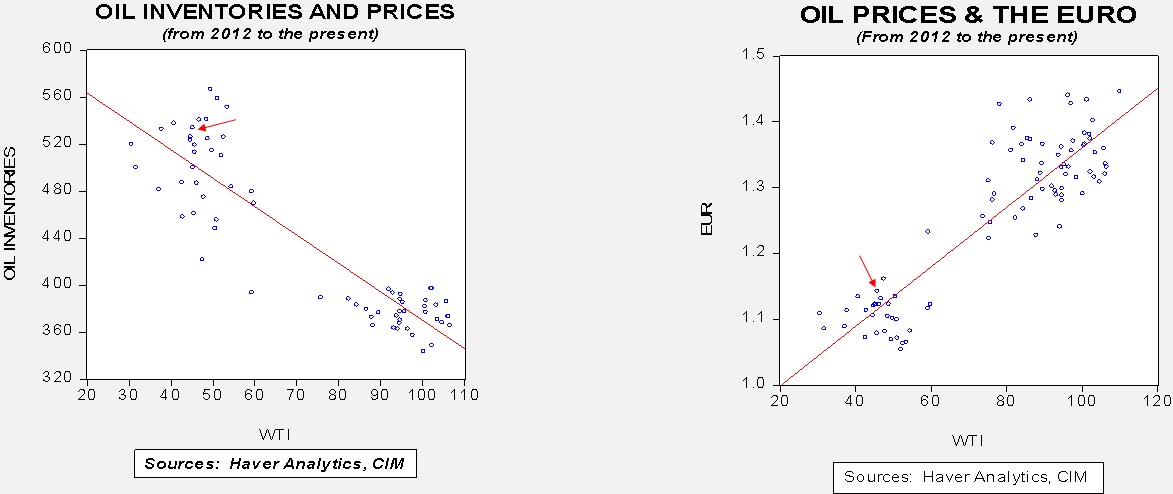

Based on inventories alone, oil prices are overvalued with the fair value price of $47.18. Meanwhile, the EUR/WTI model generates a fair value of $56.55. Together (which is a more sound methodology), fair value is $53.38, meaning that current prices are well below fair value. The most bullish factor for oil currently is dollar weakness, although the rapid decline in inventories is also supportive.

Oil prices have recovered from earlier weakness and are stalling at about the midpoint of the recent range.

This chart shows the nearest oil futures price; we have placed a box that highlights the price range of $45 to $55 per barrel. We have also set a downtrend line from the past three price peaks. Prices are struggling to break that downtrend line, but if they do manage to move higher then resistance rests at $52 and $54 per barrel. We would not expect prices to break out above $55.

[1] http://www.politico.com/story/2017/08/03/debt-ceiling-republicans-clash-congress-241263