Daily Comment (August 18, 2022)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Today’s Comment is split into two sections. In the first half, we explain why speculation about a Fed pivot is premature. We briefly summarize the meeting minutes, show the market’s reaction, and discuss how the strong jobs market will affect the central bank’s decision to raise rates. In the second half, we review reports indicating that regional bloc formation can change over time. We discuss India’s military exercises with U.S. rivals China and Russia, Beijing’s reaction to the U.S. trade negotiations with Taiwan, and Turkey’s growing disenchantment with the West. After each section, we provide a synopsis of the stories covered and their possible ramifications.

Central Bank News: Meeting minutes revealed the Fed’s openness to a pivot, but employment and inflation data suggest that monetary tightening is still needed.

- The Federal Reserve meeting minutes reinforced the market’s dovish perception of the central bank. Although Fed officials agreed unanimously to raise rates by 75 bps at the July 27 Federal Open Market Committee meeting, the minutes revealed that policymakers were also concerned about the economy. Fed officials noted that specific interest-rate-sensitive sectors, such as housing, were hurt by higher rates and warned the impact would spread into other areas of the economy. Additionally, it mentioned that some officials could support a pause once the rates reach the restrictive territory.

- Investor optimism that the Fed will end its tightening cycle before achieving its 2% target is misguided. On Wednesday, the S&P 500 pared back most of the day’s losses, Treasury yields dipped, and the dollar fell from the day’s high. The market’s reaction suggests that a recession will force the Fed to change its policy path. However, the minutes revealed the central bank is only focused on achieving its dual mandate of price stability and low unemployment.

- Prediction of policy moderations is overblown. The Fed would like the labor market to show tangible signs of deterioration before it ends its tightening cycle. The July employment payrolls report exceeded expectations, and the unemployment rate dropped from 3.6% to 3.5%. The Fed fears that an overly tight labor market leads to wage pressure, thus contributing to inflation. As a result, it is unlikely to stop raising rates as long as inflation remains high, and the unemployment rate is low.

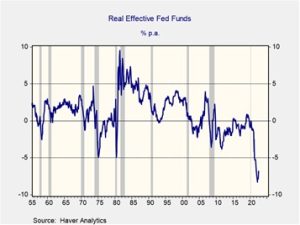

- Another reason for our skepticism of a Fed halt or reversal in its policy path is real fed funds. The Fed has never stopped tightening with a negative real Fed funds rate, which stands at -6.82% as of August 10. The Fed would need to raise rates almost 700 bps before the real Fed funds returned to positive territory.

The period of ultra-low inflation has likely passed, but it was good while it lasted. Although the Federal Reserve remains optimistic that slower economic growth will eventually resolve supply chain issues, we are not. Ongoing geopolitical tensions in Europe and Asia will make firms rethink their supply chains. Relatively safe countries that are friendly to the U.S. will be attractive destinations for firms looking to move their operations. That said, in the short run, labor will be able to extract higher wages from their employers, especially as the U.S. unemployment rate remains low. As a result, we believe investors should position themselves to adjust to a higher interest rate and inflation environment.

Geopolitical Tensions: Regional blocs are forming in ways that are hard to predict in the long run.

- U.S. ally India will join China, Russia, and Belarus for joint military exercises. India’s participation highlights the delicate balance countries are playing not to align with major power blocs. Its decision to play both sides isn’t without precedence. India was one of the founding members of the nonalignment movement during the cold war. The U.S. has recently turned a blind eye to India’s buying of Russian fuel and weapons. However, it isn’t clear if they will continue to do so indefinitely. The U.S. has built closer ties with India as a way to isolate China in the Indo-Pacific region. If it turns out that India is cozying up to China, the U.S. could back away and look for an alternative country to challenge China’s dominance within the region.

- India has been a significant foreign direct investment target over the last two years. Firms have relocated manufacturing and service operations to the country due to its vast labor market and relatively low costs. If India’s relationship with the U.S. begins to sour, it could force firms to change tactics and look elsewhere.

- The U.S. continues to annoy China with its flirtation with Taiwanese recognition. The White House plans to hold trade discussions with Taiwan in the fall of this year. The talks have angered China, which views the gesture as another attempt to undermine its sovereign claim over the self-governing island. Although the negotiations are unlikely to lead to conflict, they may pave the way for further escalation. Hence, the possibility of a direct confrontation between the two major powers remains elevated. Firms with considerable revenue exposure or deep supply chains within China or Taiwan may be at risk.

- Despite the dangers, European firms are still investing in China. Financial inflows from Europe increased 15% in the first half of 2022 compared to a year earlier. The increased investment suggests that firms are prioritizing short-term gains over long-term security.

- Internal rivalries within the Western military alliance threaten the group’s commitment to supporting Ukraine. To the annoyance of Ankara, Greece has played a central role in the U.S.’s ability to transport weapons to the Ukrainians. The Mediterranean nations have a long and heated rivalry, including conflict over Cyprus and other territorial disputes. Turkey fears its ties with the U.S. are threatened by Greece’s growing importance in the war. The growing closeness between the U.S. and Greece can partially explain why Turkey has built closer economic relations with Russia. The breakdown of the Western alliance will likely make it harder for Ukraine to maintain its war efforts and could pave the way for the war’s conclusion. Any end to the conflict will be taken positively by markets.

- Turkish President Recep Tayyip Erdoğan will meet with Ukrainian President Volodymyr Zelensky to discuss steps to end the war.

The reshuffling of allies is not unusual during times of war. During World War II, Italy notoriously declared war on its former Axis partner Germany. Therefore, as regional blocs start to form, we do expect that certain countries could decide to switch sides or choose to fly solo. Over the last few weeks, we have been paying close attention to the European Union. Although it has historical and economic ties with the U.S., its reliance on Russian energy and its exposure to China shows its interests are not fully aligned with its American counterparts. We are not predicting a break of ties but rather that the two regions may push for separate aims. If we are correct, the lack of foreign policy cohesion between the U.S. and Europe could severely complicate firms’ ability to operate in different countries.