Daily Comment (April 30, 2024)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Our Comment today opens with growing concern among top Israeli officials that they could be indicted for war crimes over their conduct of the war against Hamas. We next review a wide range of other international and US developments with the potential to affect the financial markets today, including several key economic statistics and a preview of the Federal Reserve’s latest policy meeting, which starts today.

Israel-Hamas Conflict: New reporting says Israeli Prime Minister Netanyahu has become increasingly concerned that he and other top Israeli officials could be indicted for war crimes by the International Criminal Court, which has been investigating Israeli and Palestinian conduct against each other over the last decade. The reports say Netanyahu is so concerned that he asked President Biden over the weekend to intervene to make sure the ICC doesn’t issue arrest warrants against him or his national security officials.

- A spokesman for the US National Security Council issued a statement saying that the ICC has no jurisdiction over the Israel-Hamas conflict and that the White House does not support its investigations.

- In any case, Netanyahu’s concern illustrates the risk that Israel is becoming increasingly isolated and is suffering significant reputational damage over its battle against Hamas in the Gaza Strip. As a result, the Israeli stock market, which had become an investor darling in recent years, could face years of headwinds.

Eurozone: Excluding price changes and seasonal effects, first-quarter gross domestic product rose 0.3%, beating expectations and easily reversing the revised 0.1% decline in the fourth quarter of 2023. The growth rate in January through March was the region’s strongest since the third quarter of 2022. Much of the growth reflected a renewed expansion in the German economy, which benefited from stronger investment and exports. Excluding the volatile food and energy categories, the core GDP price index was up just 2.7% year-over-year.

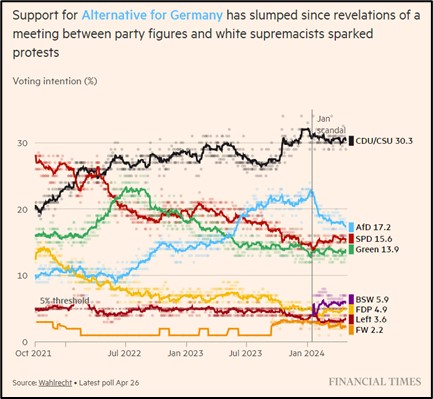

Germany: Little more than a month ahead of the elections for the European Parliament, new polling shows the once-surging, right-wing populist Alternative for Germany (AfD) party is rapidly losing support following revelations that Chinese and Russian spies have been working in its ranks. The reports suggest Chinese and Russian agents have infiltrated populist, anti-establishment political parties and media outlets throughout the West. In turn, any further revelations of the type could slow populist gains in other countries as well.

Japan: Masato Kanda, the vice minister of finance in charge of currency policy, declined today to confirm reports that the government had intervened in the market yesterday to prop up the yen (JPY). Nevertheless, he noted that the recent depreciation in the currency was hurting vulnerable people by raising the prices of imported goods. He stressed that the government would therefore respond firmly to excessive movements in the currency market, in what amounts to a virtual admission of the intervention yesterday.

- Taken together, Kanda’s statement and the intervention yesterday suggest the government’s red line on the yen’s value is now about 160 per dollar ($0.00625). If the currency looks set to depreciate below that level going forward, the government is likely to intervene again.

- So far this morning, the yen is trading at approximately 156.92 per dollar ($0.00637).

Australia: March retail sales unexpectedly fell by a seasonally adjusted 0.4%, wiping out the revised 0.2% gain in February. The culprit? In part, it was Taylor Swift, whose multiple sold-out concerts in February had boosted ticket sales, travel, and other types of consumer spending. Now that the Swifties have gotten back to normal life, the data shows that Australian consumers are in a funk, with retail sales in March up just 1.3% year-over-year.

China: The official purchasing managers’ index for manufacturing fell in April to a seasonally adjusted 50.4, beating expectations but still down from 50.8 in March. The nonmanufacturing PMI fell to 51.2 from 53.0. Like most major PMIs, these are designed so that readings over 50 indicate expanding activity. The April data therefore suggests the Chinese economy is still growing again after a period of weakness, but because of challenges such as the continued decline in real estate development, the recovery remains modest and could fizzle out.

- Faced with the risk of the current recovery petering out, the Communist Party Politburo today issued a statement hinting at new economic stimulus measures.

- The statement suggests the People’s Bank of China could soon launch a new set of interest-rate cuts, while the government provides new support for the housing market.

China-Solomon Islands-United States: The Solomon Islands’ pro-China prime minister, Manasseh Sogavare, yesterday said he would not stand for a new term when lawmakers vote this week for a new prime minister. Rather, ex-Foreign Minister Jeremiah Manele will represent his party. By stepping down, Sogavare insists his party will cobble together 28 of the 50 seats in parliament to retain power, but a coalition of key opposition parties has 20 seats locked up and could convince enough smaller parties and independents to join it and take power.

- If Sogavare’s party loses the parliament vote, it could reflect popular dissatisfaction over his 2022 security deal with Beijing, which has brought Chinese police to the Solomon Islands and drawn the Solomons away from the US.

- Parliament’s vote for the prime minister is due to be held on Thursday.

US Monetary Policy: The Fed begins its latest policy meeting today, with its decision due at 2:00 PM EDT tomorrow. Given the continued momentum in US economic growth and persistent price pressures, the policymakers are widely expected to hold the benchmark fed funds interest-rate target unchanged at a range of 5.25% to 5.50%. Based on interest-rate futures trading, it now appears investors expect the first rate cut — perhaps the only rate cut this year — to come around the end of summer.

- As we’ve noted before, continued high interest rates will likely put stress on certain banks, commercial real estate owners, and other players in the financial markets.

- Despite the economy’s current positive momentum, high interest rates probably remain a risk for the economy and financial markets.