Daily Comment (April 26, 2023)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM EDT] | PDF

Good morning! It’s a mixed market this morning after a rough day yesterday. The dollar and interest rates are lower, while S&P futures were higher but have seen gains erode as the morning wears on.

In today’s Comment, we open with President Biden’s announcement of his second and last campaign. From there, we move to financial news, with a focus on the banking system (again). China news is next (spoiler alert—Xi has talked to Zelensky). International news comes after, and we close with economic news.

Biden’s Last Campaign: As widely anticipated, President Biden formally announced he is running for a second term. Although polling shows little enthusiasm for this news, there isn’t really an obvious alternative for the Democrats at this point. Beyond the spoiler candidate of Robert Kennedy, we don’t expect a serious challenge to this nomination. What is getting a good deal of focus is the president’s decision to keep Kamala Harris as this running mate. Harris has had a rocky tenure as VP and given Biden’s advance age, there is a higher-than-normal chance she could become president if Biden is reelected. Usually, the VP candidate doesn’t garner this amount of attention, but that doesn’t appear to be the case for now.

Financial News: First Republic Bank (FRC, $8.10) is in trouble and Microsoft’s purchase of Activision has been scotched. We also note the curious case of one-month T-bill yields.

- Equity markets were rocked yesterday as FRC shares plummeted after the bank released its Q1 results. The loss of $100 billion of deposits is what raised fears about the soundness of the bank. There are clear worries about the ability of the bank to continue operations. Essentially, the bank is holding assets that have fallen in value due to rising interest rates and is facing a jump in funding costs. The bank is attempting to sell off assets (although it will probably be at a loss), but will likely need some sort of government support to remain in business. Although this news has rekindled worries about the banking system, we note that this bank is part of a handful of banks that made aggressive investments in long duration assets. It doesn’t appear that this practice was widely adopted. Still, bank runs are psychological events, and we will be watching to see if this news spurs another jump in money market assets.

- Microsoft’s (MSFT, $275.42) acquisition of Activision Blizzard (ATVI, $86.74) has been blocked by U.K. regulators. This would have been Microsoft’s largest acquisition to date.

- In the wake of the Great Financial Crisis, leveraged loans became the preferred vehicle for leveraged buyouts, supplanting high yield bonds and other similar instruments. These leveraged loans were considered senior debt to bonds and so in bankruptcy, the loans tended to be safer. However, a recent court ruling has upset the “capital stack” which has forced these loans into the pool of more junior debt. This ruling is upsetting the leveraged loan market and could lead to widening credit spreads.

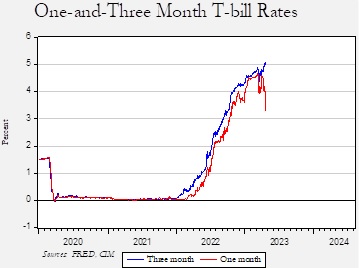

- Short duration Treasuries tend to be one of the sleeper parts of the financial system. These short-term government obligations are nearly cash like and constitute much of the “plumbing” of the non-bank financial system. Recent behavior in the one- and three-month T-bill market is raising worries.

- Most of the time, the difference in rates between these two instruments is negligible, although the one-month rate has lagged the three-month since early last year. Recently, though, we have seen a sharp divergence between the two rates. It is generally thought that the drop in one-month yields is tied to the debt ceiling issue (see below). The government may not be able to issue short-debt as it runs out of borrowing capacity, leading to scarcity. The market expects the situation to be resolved shortly though, and so three-month rates are holding up. However, we do worry that this divergence may be signaling something less benign. We could be seeing a scramble for collateral that is often used in repo transactions, and the drive to secure this collateral is leading to a drop in yields on this short-dated paper. Given the turmoil in the banking system, a problem in the non-bank system could be a significant worry. Again, it is hard to separate the debt ceiling issues from other issues, but this is a situation we will be monitoring closely.

- Remember SPACs? It is becoming clear those were a function of easy money.

China News: As we noted above, Xi has spoken to Zelensky. China is crawling toward implementing a property tax, and Chancellor Scholz has invited Premier Li to Berlin amid a major revolution in the car market.

- For years, the CPC leadership has considered implementing a property tax. The government recently announced that it has built a real estate register, an important step in applying a property tax. However, putting a property tax in place is fraught with risk. First of all, it is widely believed that high ranking CPC officials hold lots of property surreptitiously. Property is still the preferred method of holding assets in China and party officials who may have acquired cash in unorthodox ways[1] often invest in real estate under false names or under the names of other family members. A tax would reveal this practice and likely trigger another purge and capital flight. Second, a tax would almost certainly trigger additional losses in property, something that would hurt the economy. So, for now, we don’t expect a tax, but at some point, the need for revenue will probably overcome these objections.

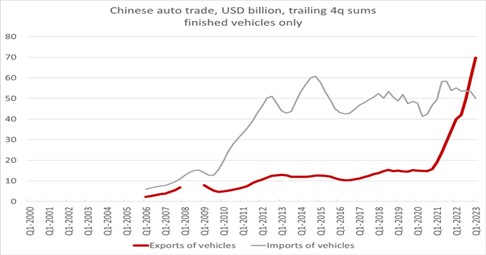

- Chancellor Scholz has invited Chinese Premier Li Qiang to Berlin in a bid to ease tensions. We note that something is developing in the auto market that could be a serious problem for Germany’s auto industry. In fact, there are twin developments underway. First, Chinese car quality standards have been improving and there is growing evidence that Chinese car companies are boosting export sales.

(Source: Brad Setzer)

- This development may be especially problematic for the EU in general and Germany in particular.

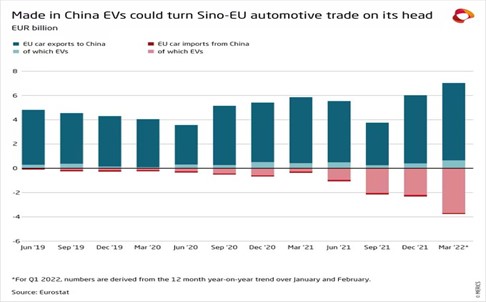

- Now, this isn’t just gasoline cars. EVs sales are growing rapidly, especially in China, and given China’s dominance in battery production and rare earths, Chinese automakers have a strong advantage in this area. German automakers have been slower to adopt EVs and could face an onslaught of Chinese EV imports.

- Although French President Macron’s recent comments on EU relations with China have been widely panned, he may not be as much of an outlier as portrayed. The U.K. foreign secretary gave a speech opposing isolating China, for example. Although we believe the world is evolving into competing blocs, there will be those who oppose this development, or prefer to work between the blocs to maintain the benefits of wider trade.

- China’s development model was based on investment and exports. This model of development isn’t unique to China as Japan and Germany used it after WWII, and to some extent, the U.S. did too, from 1870 to 1930. Once a certain level of development is achieved, the model ceases to work, because at some point, diminishing returns on investment occur and foreign nations tire of absorbing imports. There are a few paths of transition with the most durable being to shift to domestic consumption (the U.S. path after the Great Depression) or colonization (the U.K. after its industrial revolution or Germany with the Eurozone). Japan never made the transition and has suffered economic stagnation for three plus decades. We believe this is where China is now. The Belt and Road initiative is a form of imperialism and one potential path. Still, giving up on the development model is hard, and we note that China is rolling out an export promotion plan that will be hard to execute given how fraught relations have become with the West.

- In our 2023 Bi-Weekly Geopolitical Outlook, we noted that a new space race was underway. China has unveiled a three-stage project to have a moon base operational by 2050. The U.S. sees China’s activities as a serious national security threat.

Markets, Economics and Policy: There is a glimmer of hope that the House will pass a budget bill.

- The GOP holds a slim five-vote majority in the House, meaning that passing legislation is devilishly hard, given the divided nature of the party. The party needs to pass a budget bill to begin negotiations on the debt ceiling. Without a budget bill, there is nothing to negotiate, so Speaker McCarthy knows he needs the budget bill to start the process. He has a bill in place, which would cut spending, and he claims to have the votes to pass it after making a deal with some elements of his caucus.

- There is virtually no chance that this budget will pass into law. The GOP doesn’t control the Senate or the White House. However, it could become the basis of difficult negotiations and could force the White House to accept some spending cuts. And, more importantly for markets, it raises the odds of a debt crisis and potentially a temporary default. If, on the other hand, the budget fails to pass, the House would likely be forced to accept a “clean” increase in the debt ceiling. Although financial markets expect a resolution, there are concerns growing (see T-bill commentary above) that a disruption is possible.

International News: South Korea and the U.S. discuss nuclear deterrence, and Sudan remains tense.

- During the Cold War, the U.S. and the U.S.S.R. controlled the bulk of the world’s nuclear weapons, however, they weren’t the only nuclear powers. France, the U.K., and China also had small programs, and Israel has a well-known, but officially denied, program. For the most part, though, France and the U.K. operated under American doctrine, and China was subservient to the Soviets. The key to nuclear deterrence is that a nuclear power can never be forced into unconditional surrender, since if a nuclear power fears it is about to fail, it can threaten to launch against its adversary. Both major nuclear powers had numerous nations under their “nuclear umbrella.” Although these nations didn’t have warheads themselves, there was a credible threat from an allied nuclear power that if the umbrella nation were to be invaded, then the nuclear power would prevent surrender. For the nation under the umbrella, there was always a worry that, at the 11th hour, the nuclear power would balk at deployment.

- South Korea is facing this problem. North Korea has nuclear weapons and likely the ability to deliver them, and the South Korean leadership is increasingly worried that the U.S. will “sacrifice Seoul for San Francisco.” In other words, if North Korea threatens the South with nukes, or even with conventional invasion, the U.S. won’t use nuclear weapons to protect it, due to worries that America could be bombed by Pyongyang. Thus, South Korea has suggested it would like nuclear weapons on its soil to counter the North Korean threat.

- For obvious reasons, the U.S. is reluctant to take that step, but when South Korean President Yoon comes to the U.S. this week, the administration is expected to provide assurances to the South Koreans.

- A shaky ceasefire in Sudan appears to have broken down. Western nations are struggling to evacuate citizens during the continued violence.

- There is growing evidence that the long-awaited Ukraine spring offensive may be about to start. Continued Western support will likely require some degree of success.

- There is a continued debate over Ukraine grain supplies. Neighboring nations are facing a glut of grain from Ukraine, who has struggled to export grain via the Black Sea. There is a program to export grain, but it looks like it may expire soon. The EU is trying to stop neighboring nations from freezing imports of grain from Ukraine, but the farm sectors in these nations are reeling from falling prices.

- Quietly, the EU is looking to ease rules on government spending. Although Germany remains reluctant to change regulations, the current rules tend to trigger austerity during recessions.

- We are noting widespread military exercises in the Far East. These appear to involve multiple carrier groups. Although nothing will likely come of these actions, so many warships floating in a small area does bear watching.

- Japan’s lunar mission failed.

[1] Otherwise known as bribes.