Business Cycle Report (August 28, 2025)

by Thomas Wash | PDF

The business cycle has a major impact on financial markets; recessions usually accompany bear markets in equities. The intention of this report is to keep our readers apprised of the potential for recession, updated on a monthly basis. Although it isn’t the final word on our views about recession, it is part of our process in signaling the potential for a downturn.

The US economy sustained its expansion in July, and our proprietary Confluence Diffusion Index stayed out of contraction territory for the sixth straight month. Two indicators entered expansion territory, which helped lift the overall diffusion index. Despite initial concerns, the equity markets were positively affected by the reduction in trade uncertainty. Bond markets, however, showed concern about the potential removal of Federal Reserve Chair Powell. Signs of improvement were also seen in the real economy, with both business spending and construction showing growth. The labor market remained stable but did show some signs of weakening.

Financial Markets

Equity markets are proving resilient, with the ongoing trade friction having little apparent impact on investor sentiment. This optimism has spurred a rally, led by strong performances in the Utilities and Information Technology sectors. In the bond market, yields are rising, a reflection of growing investor unease over a potential threat to the Federal Reserve’s independence. The concern is that if its autonomy is compromised, the Fed could be pressured to prioritize maximum employment over its core mandate of price stability, an outcome that would have significant implications for monetary policy.

Goods Production & Sentiment

July brought encouraging signs of resilience across key economic sectors. The goods production and sentiment segments notably improved, marked by the first expansion in our indicator that tracks the three-month average of new orders for core nondefense capital goods since 2022. This industrial strength was complemented by a significant jump in housing starts, driven by a pivot toward larger multi-family projects. Furthermore, consumer confidence rebounded noticeably as expectations began to normalize following earlier tariff-related shocks, although the indicator remains in contraction territory.

Labor Market

The labor market was the sole category exhibiting signs of weakness, but conditions remain broadly healthy. A slight increase in the unemployment rate weighed on the index, pulling it further into contraction territory. However, downward revisions to July’s nonfarm payrolls pushed the indicator to just above the contraction threshold. Some of this weakness is attributable to firms adopting a more risk-averse approach amid ongoing trade uncertainties; this should improve as greater policy clarity emerges.

Outlook & Risks

The economy is on solid footing, with some metrics reaching post-pandemic highs. This trend is expected to continue, provided policy remains predictable. Markets are likely to focus on the potential for monetary easing. While lower rates could mitigate the impact of tariffs on businesses, they also risk fueling inflation by stimulating consumption. Consequently, we are cautiously optimistic on risk assets due to strong fundamentals but await confirmation that this growth is sustainable for the medium term.

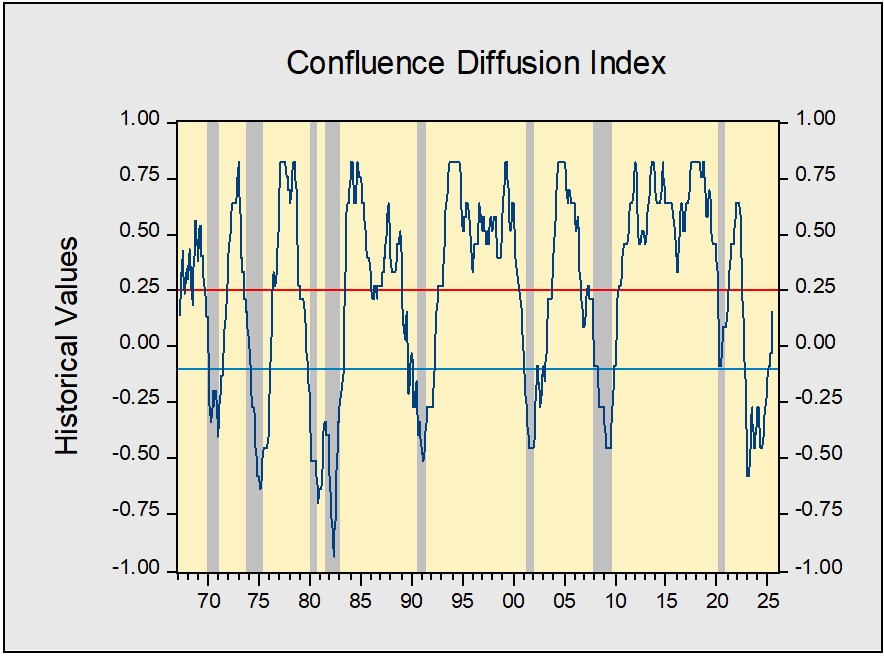

The Confluence Diffusion Index for August, which encompasses data for July, remains well above the recovery indicator. However, two of the 11 benchmarks remained in contraction territory from last month. Using July data, the diffusion index rose from -0.0303 to +0.1515, above the recovery signal of -0.1000.

- Equities softened due to trade tensions but remain elevated.

- Business spending showed signs of picking up.

- Revisions hurt job numbers but not enough to enter contraction territory.

The chart above shows the Confluence Diffusion Index. It uses a three-month moving average of 11 leading indicators to track the state of the business cycle. The red line signals when the business cycle is headed toward a contraction, while the blue line signals when the business cycle is in recovery. The diffusion index currently provides about six months of lead time for a contraction and five months of lead time for recovery. Continue reading for an in-depth understanding of how the indicators are performing. At the end of the report, the Glossary of Charts describes each chart and its measures. In addition, a chart title listed in red indicates that the index is signaling recession.