Asset Allocation Weekly (November 3, 2017)

by Asset Allocation Committee

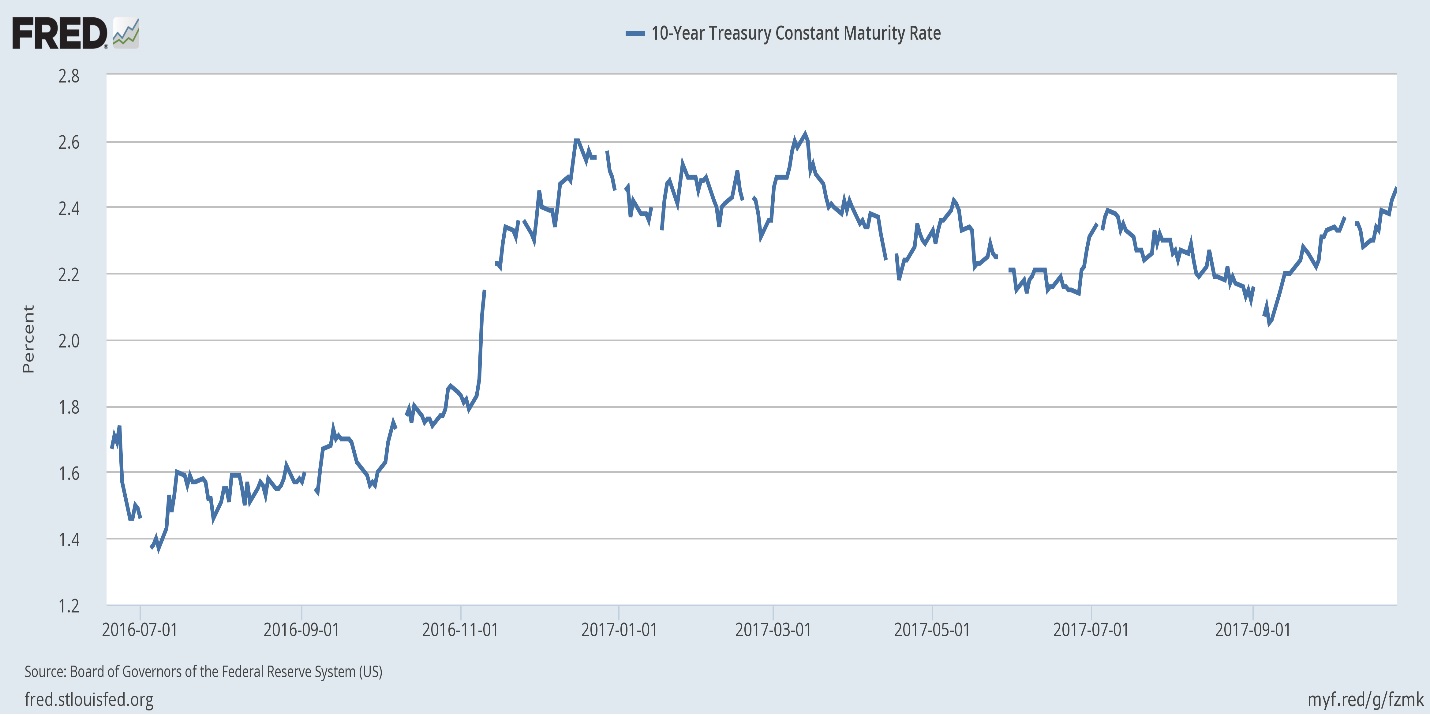

The 10-year Treasury yield has recently been trending upward.

Since early September, yields have risen from 2.06% to 2.46%. What’s behind this rise and do we expect it to continue?

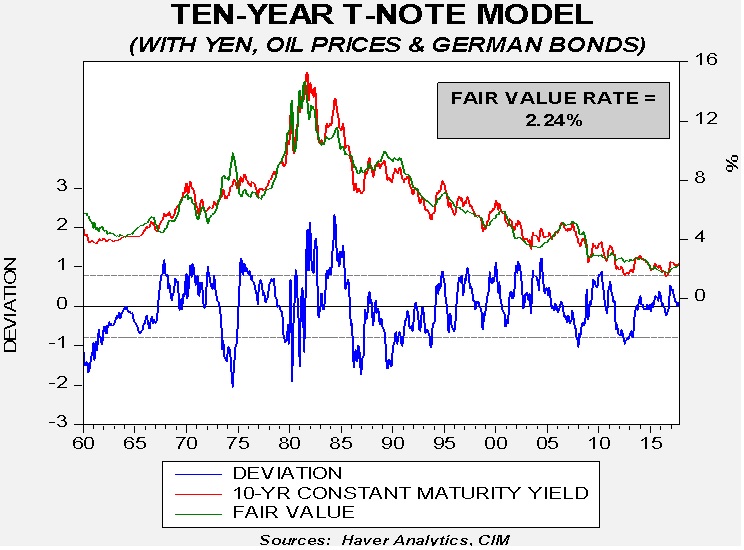

We use our 10-year T-note model for guidance. It estimates the fair value level of the 10-year T-note yield based on the long-term average of inflation, fed funds, German long-dated sovereign yields, the yen/dollar exchange rate and oil prices.

Based on these factors, the current fair value is 2.24%, a bit lower than the current yield. At the end of 2016, fair value was 1.96%, so the fair value rate has been moving higher. The primary reason has been a modest rise in German yields, rising fed funds and higher oil prices.

What do we see going forward? The two independent variables that have the most potential for pushing the fair value higher in the near term are fed funds and German yields. If the fed funds target rises to 2.25% by the end of next year and nothing else changes, the fair value yield would rise to 2.78%. If German bunds were to rise in yield to 0.75% at the same time, the fair value yield would rise to 2.80%. Thus, the primary worry is monetary policy. As we discussed last week, given the FOMC’s voting roster next year, the FOMC will be unusually hawkish in 2018, so the odds of higher yields are rising.

What about tax policy? Would larger deficits boost yields? The impact of deficits on interest rates is mixed. Perhaps the best way to think about this is with the savings identity.[1] The identity is: (private saving) + (public saving) + (foreign saving) = 0. In theory, if tax cuts result in a deficit of public saving, it must either be offset by rising private saving (saving>investment) or rising foreign saving (otherwise known as a current account deficit). If the public deficit is resolved by private saving, interest rates usually rise. But, if it is offset by foreign saving, domestic interest rates become a function of foreign interest rates. In other words, if foreign interest rates are low, domestic interest rates may not necessarily rise. In practice, large deficits usually occur during recessions and private saving is rising anyway as consumption falls. Thus, there will be talk about tax cuts boosting interest rates but the evidence isn’t clear to support such statements.

The long-term risk for fixed income is inflation expectations. We use the 15-year average of CPI as a proxy for inflation expectations. Although we still expect inflation expectations to remain low, if populism leads to reregulation and/or deglobalization of the economy, inflation and expectations of future inflation would likely increase. If policymakers conclude that inequality must be reduced by restricting the introduction of new technology and restraining trade, greater inefficiencies will likely bring higher inflation. If such policies develop, we will become more defensive on fixed income.

[1] For a deeper discussion, see WGRs from May 2017, Reflections on Trade: Parts I-IV.