Asset Allocation Weekly (August 31, 2018)

by Asset Allocation Committee

In light of the recent conviction of Paul Manafort and the guilty pleas by Michael Cohen, along with the upcoming midterm elections, we have been receiving questions about the political landscape going into winter. In this report, we will discuss our baseline expectations for political trends and their potential effect on financial markets.

Our expectations:

We expect the Democrats to win the House in November but the GOP will hold the Senate. Current prediction market wagers are the primary basis for this expectation.

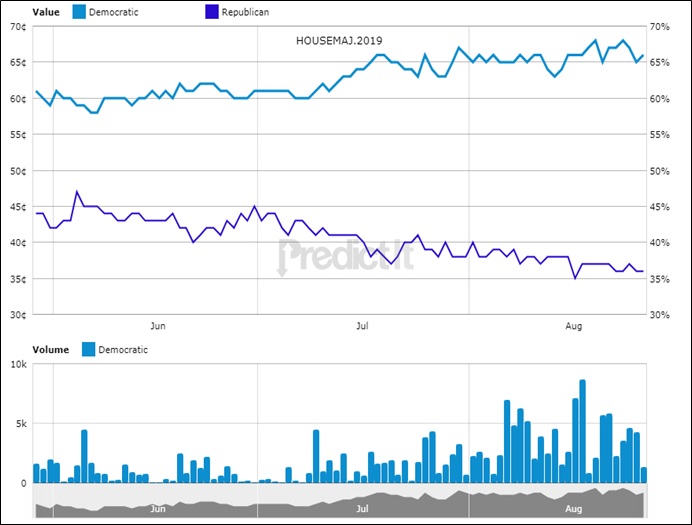

For the House, the prediction market has been consistently indicating a 65% likelihood that House control changes parties. At the same time, the same group shows the likelihood that the GOP retains control of the Senate is above 70%.[1]

A divided legislature will lead to gridlock. We expect a Democrat-controlled House to use its subpoena power to investigate any potential corruption in the Trump White House. According to Axios,[2] there will be a plethora of potential areas to examine. Because of this distraction, we doubt the White House will be able to muster any significant legislative achievements. This outcome isn’t all that unusual. Normally, the peak of a president’s power is in the first 18 months of his first term. Any political capital that isn’t spent in this period is lost. By summer of the second year in office, midterm elections are looming and Congress is distracted by the upcoming vote. Often, the president’s party loses seats in Congress after the midterms and legislative progress grinds to a halt. This usual pattern, coupled with the likelihood of perpetual investigations, probably means not much will get done.

Will the Democrats impeach President Trump? Much of this will depend on what the House investigations unearth. Although articles of impeachment might be approved, there is very little chance that two-thirds of the Senate would vote to remove Trump from office.

How will financial markets react to these baseline forecasts?

Equity markets: There have only been two impeachment events during modern market conditions, in the early 1970s under Nixon and the late 1990s under Clinton. In the former event, equities declined but the Watergate scandal was probably nothing more than a minor contributing factor. The economy was in a deep recession in 1973-74, and the world economy was reeling from the end of Bretton Woods and the Arab Oil Embargo. Simply put, there was a lot going wrong and the Nixon resignation was only part of the overall turmoil. In the latter case, equity markets were in the midst of the great tech bubble and mostly ignored the political news.

In general, equity markets will be sensitive to the business cycle and policy. We don’t expect a recession over the next three to four quarters. If the Fed overtightens, which will be an increasing risk next year, a recession is possible. For now, we expect the FOMC to move slowly on rates and avoid a policy error. In terms of fiscal and regulatory policy, the equity markets have already received support in the form of corporate tax cuts, additional spending and deregulation. At the same time, we have seen some weakness develop on fears of a wider trade war. If congressional investigations slow the trade conflict, we could see the bull market in equities not only continue but gain strength.

Debt markets: If trade impediments don’t increase and the Fed continues to raise rates, the odds of higher interest rates will increase. Political turmoil may lead to some flight-to-safety buying for Treasuries, but credit spreads could widen as a result. Overall, we could see the 10-year Treasury yield move toward 3.15% but would not expect it to move much above that level.

Currencies: The dollar is probably the most vulnerable of all the asset classes. On a parity basis, the dollar is overvalued (our parity against the EUR is approximately $1.3050) and has been rallying mostly on trade worries. If the U.S. puts up broad trade barriers, we would expect foreign nations to depreciate their currencies in order to offset the price increases triggered by the tariffs. When President Trump appeared ready to apply trade restrictions globally, the dollar rallied. However, the recent deal on NAFTA and the détente with the EU suggests that the administration’s real goal may be to contain China. If so, the dollar could weaken; political turmoil might accelerate that trend. A weaker dollar would tend to benefit international investments, U.S. large caps and commodities.

The political situation will not be the only factor affecting market behavior. For equities, earnings and the overall economy will still be significant. Political peace coupled with a recession would still be bearish for stocks. The above discussion addresses the likely impact of the unfolding political situation. The bottom line is that our position, for now, is that the current political situation, by itself, probably won’t be a major market-moving event.

[1] https://www.predictit.org/Market/2703/Which-party-will-control-the-Senate-after-2018-midterms

[2] https://www.axios.com/2018-midterm-elections-republicans-preparation-investigations-180abf7b-0de8-4670-ae8a-2e6da123c584.html