Asset Allocation Bi-Weekly – The AI Arms Race: Navigating the Divide Between Promise and Profit (October 6, 2025)

by Thomas Wash | PDF

AI is arguably the most exciting investment story of our time, with discussions swirling around its potential to create new businesses, boost productivity, and drive unprecedented revenue growth. This excitement has fueled massive spending as tech firms race to capitalize on the technology’s promise. As the hype has intensified, however, a critical question has emerged: Is AI growing faster than our ability to adapt to it?

A recent MIT report, “The GenAI Divide: State of AI in Business 2025,” suggests this may be the case. The study reveals a staggering 95% of corporate generative AI pilots have failed to deliver a measurable return on investment. This poor performance is fundamentally attributed to “execution failure,” with key issues including a lack of organizational readiness and a disconnect between the technology and day-to-day business workflows. The report also found that firms using consultancy services were more successful, highlighting that effective implementation and user adoption are critical to success.

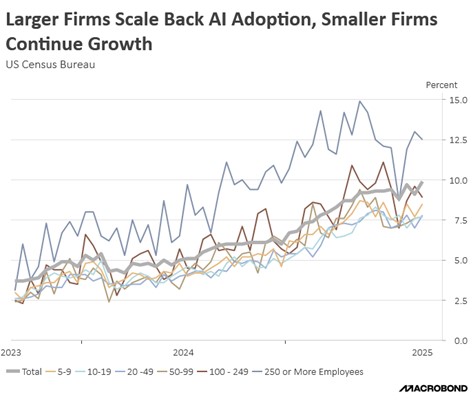

This finding aligns with a separate trend observed in a U.S. Census Bureau survey, which shows that large firms have begun to slow their adoption of AI. This indicates that the initial hype that fueled demand may be giving way to a more cautious, results-driven approach as companies grapple with the practical challenges of integrating AI into their operations.

The current spending by major tech companies on AI infrastructure suggests that while AI may be the technology of the future, they are investing as if it’s already a present-day reality. Driven by the immense computational and energy needs of training large AI models, firms like Microsoft, Alphabet, Meta, and Amazon have made the uncharacteristic decision to ramp up capital expenditures.

In 2025 alone, tech companies are projected to spend up to $344 billion on AI infrastructure, including data centers and the hardware required to run complex models. This surge marks a sharp departure from the sector’s traditionally asset-light strategy, which prioritized intellectual property over physical assets to maintain large cash reserves. The current high-stakes environment has led to a massive increase in capital expenditures (capex), often referred to as the AI “arms race,” which is rapidly drawing down the operating free cash flow of many major tech companies.

This capital-intensive trend is expected to continue, significantly aided by the passage of the One Big Beautiful Bill Act (OBBBA) in July. This legislation permanently reinstated a 100% bonus depreciation for qualified property (like computer equipment and servers) acquired after January 19, 2025. It also introduced a new, temporary allowance for 100% expensing of “Qualified Production Property.”

The significant effort to build out AI infrastructure has acted as a healthy indicator of growth across the sector, boosting revenue for numerous suppliers. Nvidia has been the most notable beneficiary, but other firms, including Intel and SAP, have also seen gains. Most recently, Oracle saw its stock jump by nearly 30% after reporting that its first quarter booked revenue included over $455 million in new business related to its cloud infrastructure, signaling strong enterprise demand for AI-enabling services.

While supplier earnings remain robust, the sector faces growing risks of over-dependence. Many key AI technology providers rely on a highly concentrated group of customers — primarily the few cloud giants — for the vast majority of their revenue, raising concerns about the concentration risk inherent in their earnings estimates.

Furthermore, concerns persist that a significant portion of AI funding is circulating within a closed loop of major companies. This occurs when cloud giants invest in smaller AI startups, which then use that capital to purchase cloud infrastructure and compute time from their investors. This circular dynamic risks distorting genuine market demand and may artificially inflate the revenue of the largest players.

Despite these concerns, we believe the current equity rally has a strong chance of continuing for the foreseeable future. The bull market, which began in October 2022, has historical precedent on its side, with average cycles lasting about five years, suggesting the potential for another two to three years of upside.

However, given the market’s heavy concentration in large cap technology, the risk of a sharp correction in these high-growth stocks is elevated. To mitigate this risk, we recommend maintaining exposure to value stocks, which can provide crucial defensive ballast to a portfolio. Value-oriented sectors typically exhibit lower volatility and have historically demonstrated greater resilience during periods of economic uncertainty or growth stock selloffs.