Asset Allocation Bi-Weekly – The UAE’s Exit From OPEC (June 1, 2026)

by Bill O’Grady | PDF

On May 1, the United Arab Emirates (UAE) formally exited both the Organization of the Petroleum Exporting Countries (OPEC) and the broader OPEC+ grouping of major oil producers. Such exits are not unheard of. For example, Indonesia suspended its membership in OPEC in 2015. However, Indonesia left the cartel not because it wanted to produce more oil, but because it had become a net oil importer. Qatar left the cartel in 2019, but there were several factors that led to its exit, including the fact that it had become more of a natural gas producer and Saudi Arabia and the UAE had isolated the country over its fostering of the news organization Al Jazeera.

Unlike Indonesia, the UAE has excess oil production capacity that represented about 25% of the cartel’s total. Like Qatar, tensions between Saudi Arabia and the UAE are elevated. The two countries have supported opposing sides in Yemen, for example.

In the immediate term, the UAE’s decision won’t affect the oil markets significantly. That’s because the Strait of Hormuz remains mostly closed. Although the UAE does have a pipeline to the Gulf of Oman, bypassing the strait, it is currently already fully utilized. Thus, the UAE can’t increase its oil output or exports until the US-Israeli war against Iran comes to some sort of resolution. But once that occurs, there will likely be a market impact.

Just what sort and how much of an impact is the focus of this report. To understand why the UAE’s action is important, it’s worth examining the role of cartels in the oil market. Oil supply has a tendency to be “lumpy.” On occasion, large oil fields are discovered and developed. Once these fields begin producing, supply usually increases dramatically. Oil demand is price inelastic, which means that in the short run demand doesn’t immediately react to the increase in supply. A glut of oil occurs, which brings sharply lower prices. Usually, suppliers react to the drop in price by reducing output. However, oil fields have limited flexibility in boosting or cutting output as oftentimes it can be very costly to reopen a well once it has been shut in. Oil is also unique compared to other commodities in that there is an incentive to continue producing once a well is operational because, if a producer were to stop, there would be nothing to prevent other drillers from pulling oil from the same field.[1]

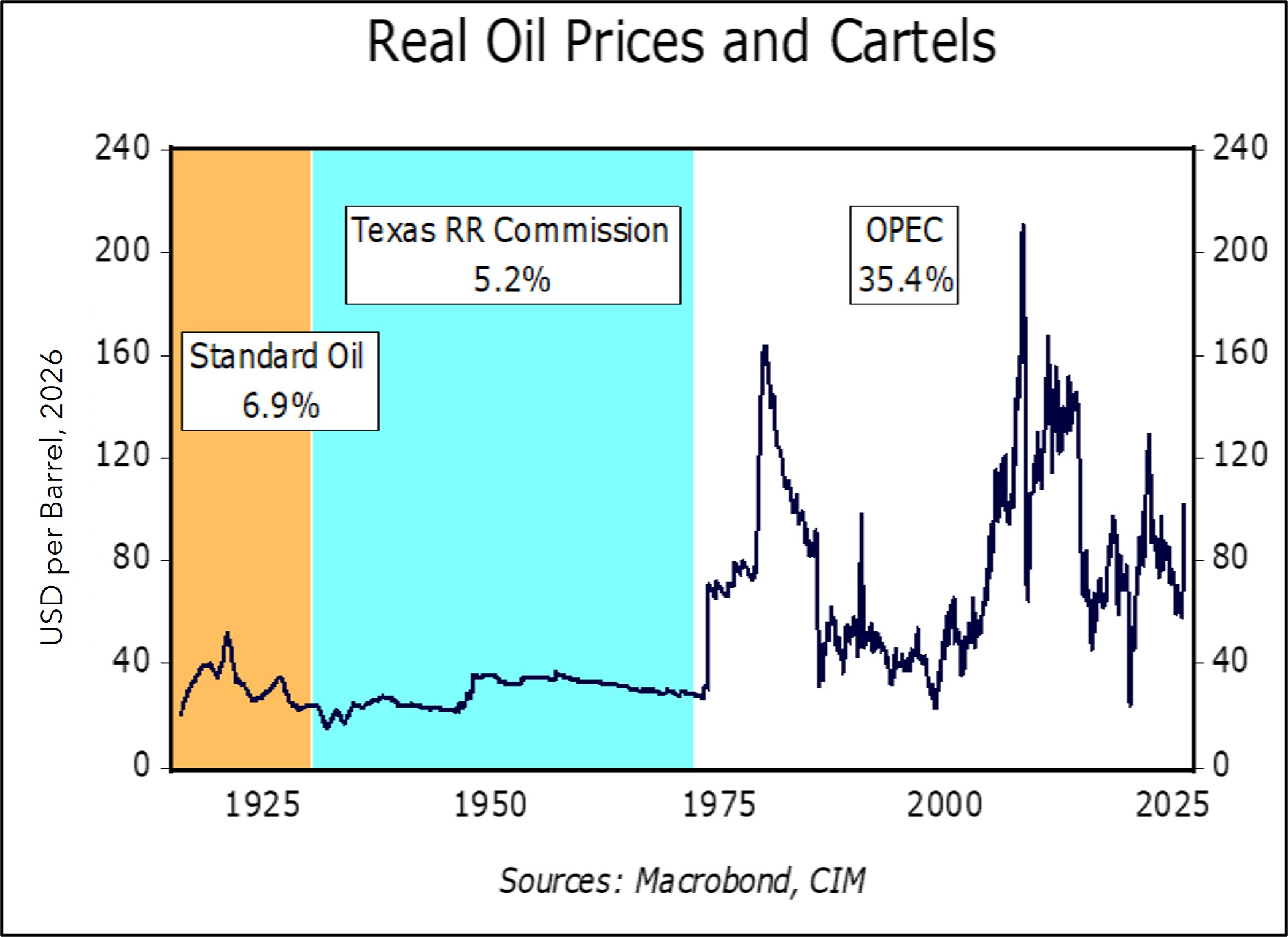

This situation can lead to collapsing prices. When the East Texas Oil Field was discovered during the Great Depression, production soared and caused prices to fall from $1.10 per barrel to $0.15 per barrel. Not only can such a glut be ruinous for producers, but the rush to generate cash flow can lead to overproduction and damaged reservoirs. In this example, the Texas Railroad Commission, which had authority to regulate oil production in the state, used the state militia to enforce production shares. The commission became the de facto cartel manager of the oil market, holding production off the market to keep the price higher than a free market would have generated, while also helping to stabilize prices. The Texas Railroad Commission held this role until 1972, when US consumption matched the state’s production capacity. From this point forward, OPEC became the cartel that manages the oil price.

The chart above shows the inflation-adjusted price of West Texas Intermediate oil, deflated by the US consumer price index. Although Standard Oil was formally broken up in 1911, its successor companies mostly managed production. From 1915 until 1930, the standard deviation of oil prices was 6.9%. The Texas Railroad Commission era shows a standard deviation of 5.2%. Clearly, OPEC has been the least successful cartel in terms of price management, with a standard deviation of 35.4%. But, as the chart shows, it has been successful at managing prices at times. For example, from 1986 through 1999, the standard deviation was 10.0%, even during the Gulf War.

Nevertheless, OPEC has struggled to manage prices in this century, with a standard deviation of 24.2%. First, it was unable to contain prices during China’s emergence after joining the WTO in 2001. It also struggled to manage the market following the advent of US shale oil.

The decision by the UAE to leave the cartel will likely further complicate price management. As we noted above, the decision doesn’t matter much while the Strait of Hormuz is blocked. However, once it reopens and supply chains are restored, the UAE’s production will be a bearish factor for oil prices. We expect Saudi Arabia will attempt to maintain price stability for a time, given the country’s history of cutting its output to preserve higher prices. But, as we saw in 1985 and again in 1999, the kingdom eventually decided that it was tired of providing support for “free riders” and punished overproduction by flooding the market with oil, and we would anticipate a similar outcome here. We don’t know when this moment will occur, but traders will have to factor this possibility into prices.

Complicating matters further is the closure of the Strait of Hormuz. Oil consumers now know that this region of the world is an unreliable supplier and will undoubtedly take steps to diversify energy sources moving forward. China’s ability to manage through an “all of the above” strategy will likely support alternative energy sources, such as coal, wind, solar, nuclear, et al. The uncertainty of oil supplies tends to depress demand over time. Therefore, even before the UAE’s decision, oil prices would have eventually had to decline enough to offset the uncertainty surrounding future supply. A smaller OPEC cartel will increase the likelihood of lower prices…eventually.

[1] As highlighted in the “milkshake” scene in the movie There Will Be Blood (1:34).