Asset Allocation Bi-Weekly – The Evolution of the Tech Life Cycle (June 29, 2026)

by Thomas Wash | PDF

AI is reshaping the fundamental business model of technology companies. For decades, many tech firms distinguished themselves through capital-light operations and strong cash generation, allowing them to deliver both growth and profitability. This model enabled companies to attract investors by telling a compelling growth story, one centered on adaptability, continuous product expansion, and the development of diversified revenue streams.

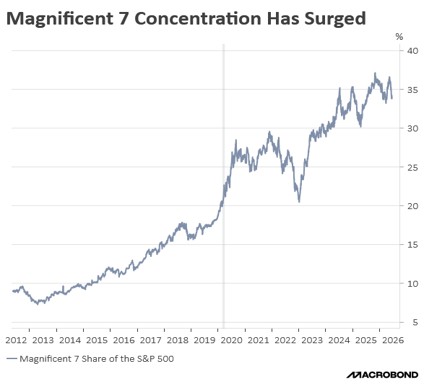

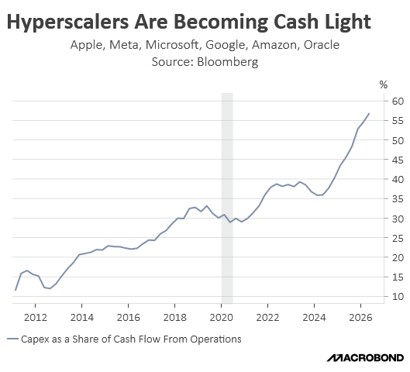

However, this paradigm is shifting. Over the past three decades, investors have grown accustomed to technology companies positioning themselves as perpetual growth stories. Today, that narrative is becoming difficult to justify in the face of swelling capital expenditures and the compression of free cash flows. We believe the rise of hyperscalers marks the beginning of a fundamental structural change. Over the next decade, many of these dominant firms are poised to evolve toward a model that more closely resembles traditional utilities, characterized by stable demand, sticky recurring revenues, and high capital intensity.

The business life cycle typically unfolds in distinct stages, and the internet and data‑center ecosystem appears to be following a similar pattern. In the early stage, the focus was on launching websites and building foundational digital infrastructure. As the sector moved into its growth phase, firms increasingly monetized data and pursued acquisitions of smaller technology companies to expand capabilities and market reach. With the rise of AI, the industry is now entering a more mature phase, one that is likely to emphasize disciplined investment, stable cash flows, and a greater focus on returning capital to shareholders.

Early Stage

The modern technology company emerged in the late 1990s alongside the commercialization of the internet. This period saw a surge in startup formation, fueled by lower capital gains taxes, supportive regulatory conditions, and accommodative financial markets, all underpinned by optimism surrounding a potential productivity boom. Within this environment, many firms prioritized rapid user acquisition and market share expansion, often at the expense of a clearly defined path to near-term profitability.

This era produced early versions of today’s household names. Amazon initially focused on selling books online, while Google operated solely as a search engine. As broadband spread and connected computers around the world, the internet quickly evolved beyond simple information access. It first enabled the growth of e-commerce, and then expanded into entertainment, news, and social networking, fundamentally reshaping how people interacted, consumed content, and transacted.

Growth Stage

While growth during this period was rapid, profitability remained elusive, pushing many firms to pivot toward monetizing their platforms. They began offering data-driven services that allowed businesses to pay for insights into customer behavior, marketing, and research. This marked an early stage of maturation, as companies recognized that while raw data was inexpensive to collect, its true value lay in aggregation, analysis, and resale. That realization has since become a defining feature — and a central economic driver — of today’s digital economy.

The recognition of data as a valuable resource laid the foundation for the rise of artificial intelligence. Initially, hyperscalers leveraged data to generate insights into customer behavior, enabling more precise targeting of products and services across specific demographics. Over time, as data became more granular and analytical techniques more sophisticated, firms moved beyond insight generation toward automating routine tasks. This shift marked the emergence of a new revenue model, in which technology companies began developing tools and platforms designed to perform work directly, rather than simply to inform decision-making.

Maturing Phase

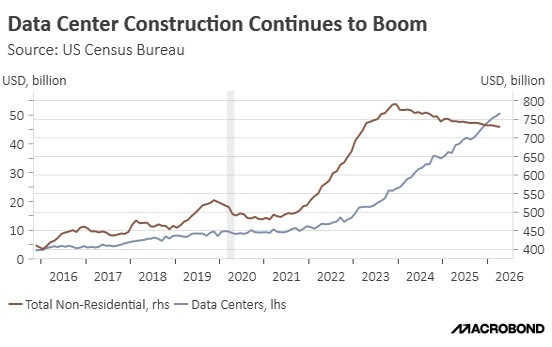

As these companies roll out more enterprise‑grade AI services, their strategic focus is shifting toward providing the tools and cloud infrastructure required to process vast amounts of data for AI workloads. In turn, this transition is pushing them away from historically capital‑light, software‑centric models and toward far more capital‑intensive structures as they invest heavily in building and expanding large‑scale data centers to support these compute‑ and energy‑hungry systems.

The shift toward providing these tools, combined with their capital-intensive nature, is likely to push these companies away from a pure growth profile and toward a more utility-like, value-oriented model over time. The scale of required investment implies a persistent cycle of maintenance, depreciation, and equipment replacement, which will weigh on margins and dampen long-term earnings growth.

Declining Phase or Life Cycle Extension

While the AI technology sector is likely far from its declining phase, the long-term trajectory is becoming clearer. The substantial fixed costs required to build and maintain AI infrastructure create significant barriers to entry, increasing the likelihood that dominant firms evolve into natural monopolies. At the core of this thesis is the expectation that these firms will become essential cloud service providers, as enterprises increasingly outsource workflows to AI-based systems.

As market share consolidates, revenue growth is likely to moderate. Rising dependence on a small number of providers — alongside mounting concerns around security, energy usage, and data control — could drive increased regulatory scrutiny. Over time, this concentration raises the probability of policy intervention aimed at ensuring broader access and affordability, particularly if AI services are viewed as critical economic infrastructure. Such oversight would likely constrain pricing power and compress margins, ultimately reducing growth expectations and prompting a reassessment of valuations as these firms begin to resemble value-oriented, rather than high-growth, equities.

There remains a plausible path for life cycle extension, but it likely requires a structural shift. As the industry matures, these firms may begin to resemble telecom companies in the post-dot-com era. During that period, telecom providers undertook massive capital investments to build out foundational networks in anticipation of rising data demand. Over time, they transitioned into broadband providers and expanded into adjacent services such as television and mobile, ultimately operating as stable, cash-flow-generating businesses.

A similar evolution could unfold in AI. While these firms initially focus on providing compute and infrastructure services, they may increasingly move up the value chain by offering more tailored, application-layer solutions, encroaching on areas traditionally dominated by software-as-a-service providers. This shift would support more stable and predictable earnings streams, but it would also limit the sector’s ability to sustain the elevated revenue growth rates currently being observed, reinforcing a transition from a high-growth to a more utility-like profile.

In Conclusion

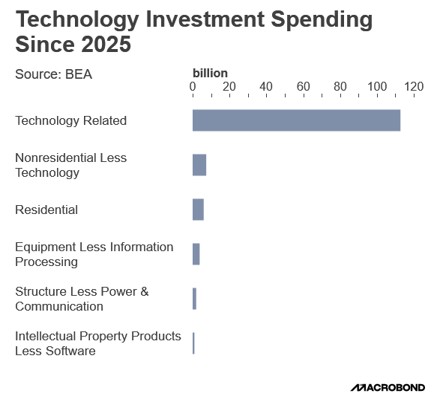

While we remain confident that the AI rally still has momentum, we do not expect it to persist indefinitely. As large technology firms — particularly enterprise-focused builders — continue to scale out infrastructure, the market is likely to reassess whether current growth and valuation trajectories are sustainable. Elevated capital expenditures and ongoing reinvestment needs are likely to weigh on incremental returns on invested capital, gradually compressing margins. As growth opportunities become more constrained, this dynamic increases the likelihood of a valuation reset.

Over time, this maturation could pressure these companies to shift toward capital return, including dividends. However, we do not expect such a transition in the near term. Until then, the gap between elevated expectations and realized returns may become more apparent, particularly as government involvement increases, raising the probability of regulatory constraints on pricing and profitability.

Against this backdrop, we see more attractive long-term opportunities emerging in other parts of the market. Industrials and energy are particularly well positioned to benefit from the capital expenditure cycle required to build out AI infrastructure, while dividend-oriented equities may become increasingly attractive as investors seek more stable income streams. As AI names increasingly trade like regulated utilities, we view value stocks as a stable foundation for investors navigating the transition ahead.