Daily Comment (May 27, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment opens with our takeaways from the pope’s first encyclical letter. We then turn to the war in Ukraine and its broader implications for modern conflict. Next, we briefly review the strong performance of chipmakers, the Texas primary, and the latest consumer confidence data. As always, we conclude with a summary of recent domestic and international economic developments.

Pope’s AI Warning: Although artificial intelligence is becoming more ubiquitous, there are growing calls for stronger guardrails. Over the weekend, Pope Leo XIV compared the rush to develop AI to the Tower of Babel in Genesis, using the analogy to underscore rising unease about both the pace of innovation and growing overconfidence in its ultimate impact. His remarks come amid broader concerns that the market’s enthusiasm for AI could prove vulnerable to a reversal if expectations run ahead of reality.

- In Genesis 11, the Tower of Babel serves as a cautionary account of human ambition outpacing restraint. The story describes a unified effort to build a city and a tower reaching the heavens — an expression of collective confidence and self-sufficiency. In response, God disrupts the project by confounding their language and dispersing the population, effectively halting progress. The episode is often interpreted as a warning about the risks of unchecked ambition and the limits of human control.

- The pope’s appeal comes at a moment when the rapid rollout of AI is generating significant disruption but, so far, only modest and uneven gains. A recent research paper from the Federal Reserve Bank of San Francisco finds that AI’s impact on productivity has been mixed, with benefits concentrated in a few sectors and slow diffusion elsewhere. Reflecting similar concerns from the private sector, Uber’s COO has acknowledged that the company’s substantial AI investments have yet to deliver consistently strong returns.

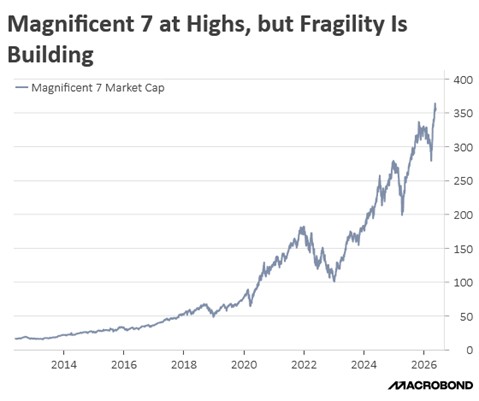

- AI remains the dominant market theme, but the related stocks have been highly volatile. They sold off in fall 2024 on worries about frothy valuations after Nvidia’s earnings underwhelmed sky‑high expectations. The group weakened again in early 2025 after DeepSeek’s launch, which investors saw as a competitive threat to leading US AI firms. Another downturn in fall 2025 followed renewed concerns that circular revenue models in the AI ecosystem were undermining the durability of underlying business momentum.

- AI still has strong momentum, but we think the rally is vulnerable to a sudden shock that could reset expectations, even if no such trigger is currently visible. We therefore recommend maintaining some exposure to value stocks as a buffer in periods of uncertainty, given their tendency to outperform during past episodes of market stress. While this diversification can mean some relative underperformance in powerful growth-led rallies, it also supports better capital preservation over time.

The Forgotten War: While there are tentative discussions about ending the US-Iran standoff, the war between Russia and Ukraine appears to be entering a new phase. On Tuesday, Moscow warned civilians and diplomats to leave Kyiv as it announced plans to target “decision‑making centers” in Ukraine’s capital. The escalation comes as Russia seeks to regain momentum after recent setbacks. The ongoing conflict in Ukraine also helps explain why the United States and Iran are struggling to find a clear off‑ramp as markets push for de-escalation.

- Moscow’s decision to escalate the conflict comes as momentum on the battlefield has shifted against it. In recent months, Ukrainian forces have regained some territory, though it remains unclear whether they can decisively tilt the war in their favor. A key concern for the Kremlin is that domestic support for the campaign may be eroding, and authorities have reportedly tightened control over Telegram, a popular social media platform, in an effort to shape and contain the narrative.

- Moscow is contending with setbacks, but Ukraine is also facing mounting challenges. A report on Monday indicated that roughly half of the countries participating in the Czech-led ammunition initiative for Ukraine have pulled out, potentially constraining supplies of badly needed shells and other munitions. Although the specific states that withdrew were not identified, Germany and several Nordic countries are reported to be continuing their military support for Ukraine.

- Ukraine and Iran’s abilities to prolong conflict reflects how cheaper weapons, particularly drones, have made it easier and less costly for states to defend their territory. These capabilities mean that, even if they cannot decisively defeat a stronger adversary, smaller countries can continue fighting and inflicting damage despite losses of key military systems. In this environment, they have little incentive to accept unconditional surrender.

- Similar to the US-Iran conflict, the lack of a clear victory has made it difficult for the two sides to reach an agreement, largely due to concerns about political backlash from the costs incurred. Russia is in a particularly difficult position, as it needs something to show for its massive casualties and the likely continued isolation resulting from the invasion. These prolonged conflicts are likely to become more common, as cheaper weapons make it easier for smaller nations to fight larger ones.

Chip Demand: AI chipmakers Micron and SK Hynix have both crossed the $1 trillion mark as demand for processors that power cloud-based AI services continues to outstrip supply. Memory chip producers, in particular, underscore the centrality of hardware to AI build‑outs and have been among the largest beneficiaries of big tech’s infrastructure push. Yet, while these companies are thriving today, it is important to remember that the chip industry has historically been highly cyclical, with frequent booms and busts driven by shifts in supply and demand.

Texas Primary: Texas Attorney General Ken Paxton defeated Senator John Cornyn in the Republican Senate primary. His victory has created an opening for Democrats, as James Talarico is currently viewed as having a slight edge in early polling. A Democratic pickup of this seat would significantly increase the odds that Republicans lose their Senate majority. Reflecting this shift, the Cook Political Report moved the race from “likely Republican” to “lean Republican.”

Consumer Confidence: The Conference Board reported a modest easing in consumer sentiment in May. The decline reflects persistent inflation concerns, which continue to weigh on household expectations for future prices of goods and services. Compared with the University of Michigan survey, the Conference Board’s measure — typically more sensitive to labor market conditions than inflation — has shown a more moderate deterioration. Even so, the data indicates that household economic expectations remain notably less optimistic than prevailing market sentiment.