Daily Comment (May 26, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with an update on the Iran war, where the optimism over a potential new peace deal late last week has started to give way in the face of new US attacks on Iran’s military over the last 24 hours. We next review several other international and US developments that could affect the financial markets today, including new data showing that rising prices are starting to push down consumer purchasing power around the world and new research indicating that deregulation has opened up huge new lending opportunities for US banks.

United States-Israel-Iran: Despite statements late last week by President Trump and other US and Iranian officials indicating a 60-day ceasefire extension was in the works, the president, starting on Saturday, suggested the deal could still take several days to be finalized. Of course, the hints of a new deal could be mostly political posturing as in the past. It would not be a surprise if no deal materializes this week. The US yesterday also launched attacks on Iranian missile sites and mine-laying boats, further undermining hopes for a more permanent end to the fighting.

- In any case, the key point is probably that even if a peace deal is struck, normalizing global energy and commodity flows in the Middle East would likely take a year or more. That suggests global energy and commodity prices are likely still at risk of further increases, which would potentially weigh on economic growth around the world, drive government bond yields even higher, and cause important political implications.

- Separately, Israeli Prime Minister Netanyahu ordered his military to step up its attacks on the Islamist militant group Hezbollah in southern Lebanon. The move came after far-right members of Netanyahu’s cabinet demanded a full-scale resumption of Israel’s offensive there in defiance of the US administration’s preference that they stand down to support the current US-Iranian ceasefire.

- While global oil prices had fallen sharply into the weekend on hopes for a peace deal, the new US strikes on Iran and Iranian threats to retaliate have given a boost to oil prices this morning. Near futures prices for Brent crude are up some 2.9% so far today to about $96.20 per barrel.

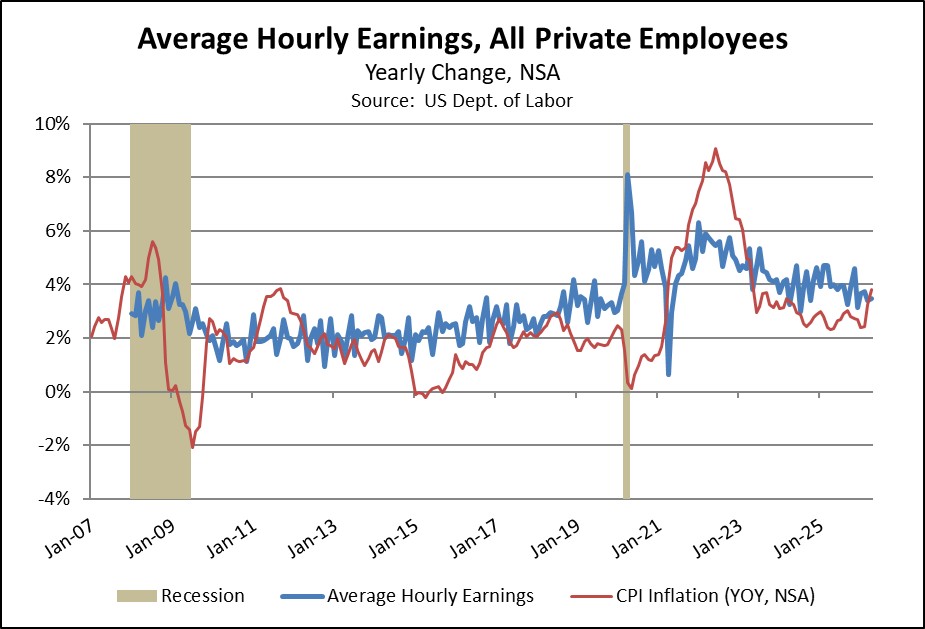

Global Labor Market: An article in the Financial Times today notes that spiking prices for energy and other commodities are threatening to cut the total purchasing power of workers around the world. In the US, for example, we have noted that the consumer price index in April was up 3.8% from the same month one year earlier, while average hourly earnings were only up 3.5%. The FT article notes that the trend is moving in the same direction in economies such as the UK and the eurozone, which will likely weigh on growth and asset values.

European Union-China: Five key EU countries have signed a paper calling for the bloc to respond more aggressively to “systemic and structural industrial overcapacity,” a phrase that is often taken as shorthand for China. The paper by the Netherlands, France, Spain, Italy, and Lithuania illustrates how the EU is increasingly riven by disagreements over whether to engage more closely with Beijing to offset a fraying US relationship or erect strong trade barriers to protect domestic industries.

- The issue will be discussed at an EU summit on Friday.

- For investors, the risk is that if trade and investment flows between the EU and China remain relatively unfettered, EU companies could gradually be weakened, even if they preserve some economic opportunities in the short term. However, tougher trade and investment barriers could lead to a trade war that results in immediate disruptions.

United States-Japan: The US has reportedly warned Japan that its purchase of 400 Tomahawk cruise missiles will be severely delayed as Washington works to rebuild its depleted arsenal after the Iran war. Japan’s Tomahawk purchase was meant to give it advanced strike capabilities and help it defend itself against China while it worked to develop its own missiles. The delay will likely spur Japan to redouble its missile development efforts, potentially giving further impetus to its expanding defense industry and creating new investment opportunities.

United Kingdom: New data yesterday said bank lending to non-financial companies fell to 59% of the UK’s GDP in the third quarter of 2025, marking the lowest level in almost 30 years. The figures were especially weak for lending to small- and medium-sized firms. The reduced bank lending reflects both weak economic growth and tougher bank regulation.

Indonesia: In a little noticed announcement last week, President Prabowo said the government will take control of the country’s major commodity exports. The first two commodities brought into the plan will be coal and palm oil. By taking the control of foreign commodity sales away from legions of middlemen, Prabowo’s goal is to curb tax evasion and improve efficiency. However, few details have been released, leaving producers and current middlemen unsure of how to proceed.

US and UK Banking Industries: New research by consultancy Alvarez & Marsal has found that deregulation allowed major banks in the US and UK to expand their balance sheets by a cumulative $1.3 trillion over just the last two quarters, giving them a significant leg up on their more constrained rivals in the eurozone and Switzerland. The figure illustrates the under-appreciated impact of recent reforms in the US and UK, which should be supportive of those countries’ bank stocks.