Asset Allocation Quarterly (Second Quarter 2026)

by the Asset Allocation Committee | PDF

- Recession likelihood is low over our three-year forecast period.

- Base case expects GDP growth near historical trend, with elevated tail risks widening the range of outcomes.

- Higher energy prices are likely to keep inflation elevated for longer.

- The Middle East conflict encourages overweights to energy, industrials, defense stocks, and miners.

- Passive flows remain a structural support for US equities, with the greatest benefit accruing to large caps. Our style tilt leans further to value over growth.

- We introduced a regional position in Asia Pacific developed markets as geopolitical and supply chain realignment could support these countries.

- Modestly extended duration as we expect a normalized yield curve which provides incremental yield.

- Gold is maintained due to heightened geopolitical uncertainty and the potential for elevated volatility.

ECONOMIC VIEWPOINTS

Our base case incorporates the view that the current conflict in the Middle East will not escalate significantly but also recognizes that the potential for an adverse outcome is higher than normal. Much of our focus this quarter is on preparing our portfolios for a post-conflict world. Recession risk remains contained and our economic growth expectation is cautiously optimistic with headwinds possible in the short term.

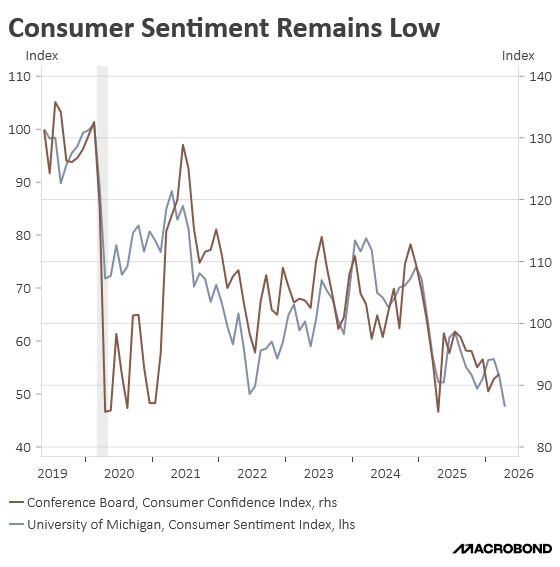

The US economy remains in expansion, but is still sensitive to policy and exogenous shocks. Recession likelihood is low over our three-year forecast period. We believe the primary macro risk is persistent inflation rather than outright recession. Price pressures appear to be sticky, calling into question future monetary policy easing. We expect the Fed to take a wait-and-see approach regarding changes in the fed funds rate as the economy endures volatile energy prices and their potential effects on a currently healthy labor market. However, consumer sentiment is depressed, with both major confidence measures still low by historical standards (see first chart). In our view, that weakness reflects affordability fatigue, political and geopolitical noise, and continued sensitivity to energy prices more than it signals imminent contraction. More broadly, economic activity continues to hold up better than sentiment surveys suggest, with consumer credit card data also pointing to ongoing spending resilience. This contrast helps explain why we believe growth can remain intact even as confidence is low and market volatility stays elevated.

We anticipate continued expansion over our three-year forecast period, with growth remaining near its long-term trend. Business investment is expected to support the economy, driven by changing supply chains and domestic reindustrialization. Business spending tied to productivity, automation, and AI-related capital expenditure continues to be strong, despite policy uncertainty and higher input costs that have created a more uneven path. Durable goods orders (see second chart) have remained positive and generally resilient, even with periodic volatility, suggesting that underlying business demand and capital spending have not rolled over. This points to an economy that is still generating sufficient investment activity to sustain growth.

We note that geopolitical risk remains an important factor. Energy disruptions, trade realignment, and broader tensions can influence inflation expectations and market psychology more quickly than they alter the underlying growth trend. With meaningful cash still on the sidelines, episodes of geopolitical stress may create temporary pauses in participation rather than a lasting withdrawal from risk markets. Cash reserves can act as stabilizers during periods of volatility, while also leaving room for renewed participation as uncertainty recedes.

STOCK MARKET OUTLOOK

Thus far in 2026, equity markets have seen a shift away from the growth-oriented, large cap technology franchises to value, small cap, and defensive sectors. While the macro environment remains supportive for risk assets, investors appear to be more valuation sensitive, possibly the result of investors anticipating a slower growth environment with interest rates remaining higher for longer. We expect improving breadth across sectors and market capitalizations, with a wider opportunity set emerging beyond the dominant mega-cap leaders. Structural support from passive flows remains important, particularly for index heavyweights, but the overall market narrative is shifting from concentration toward broader participation and greater dispersion.

We remain constructive on US large cap equities, adding to the asset class where risk-appropriate. Given our market rotation expectations, lower-risk strategies take on a heavier value-oriented tilt, while higher-risk strategies are more evenly weighted between growth-value. We added an energy sector position across the portfolios to capitalize on evolving global supply chains and the US’s position as a net energy exporter. In the more risk-tolerant strategies, we also introduced an industrials position to benefit from domestic reindustrialization and exited the communication services position. We continue to hold dividend-oriented ETFs as dividend income can serve as a reliable cushion in the higher-volatility environment we expect. Within industry positioning, we retain exposure to advanced defense and security-related technologies amid ongoing geopolitical tensions. Domestic small and mid-caps were eliminated due to relative margin differentials and passive flows that have disproportionately supported large caps.

Regarding the Middle East conflict, the world now knows that the Strait of Hormuz is uncertain and we expect a global effort to reduce the risk from this chokepoint. Thus, energy, defense stocks, and miners remain poised to benefit from these changes. Although the current conflict will likely boost energy and other commodity prices, especially in developed Asia and Europe, those markets typically have a high concentration of value stocks, which will likely benefit from the rotation discussed above. Despite the potentially long-lasting rise in energy and commodity prices, Asia and Europe also retain stock market sectors that are still likely to perform well in the coming years.

The longer-term fundamental trends of a polarizing world and US dollar softness underscore the diversification benefits of foreign assets. We maintain our allocation to international developed equities but remain out of emerging markets. International developed market exposure includes a broad-based allocation as well as several targeted positions. We continue to hold positions in global metals and miners, gold miners, and international small cap value, along with a Europe-focused ETF. This quarter, we added an Asia Pacific developed markets ETF as geopolitical and supply chain realignment could support these markets. Japanese equities are likely to benefit from recent shareholder-friendly policies in export-heavy industries, which is likely to spur overall economic growth.

BOND MARKET OUTLOOK

While we anticipate elevated inflation in the near term, as turbulence from the Iran war wends its way through the global economy, we expect it will prove temporary without a further catalyst. However, the Fed has shifted its policy stance from accommodation before the war to neutral, recognizing the near-term inflation risk from higher energy prices. Historically, a shift to tighter policy tends to pressure interest rates higher, which we saw near the end of the first quarter. However, over the next few years, we expect a more accommodative monetary policy as commodity price inflation abates. Geopolitical risks are likely to increase broad market volatility, which in turn raises the likelihood of monetary and fiscal policy mistakes. Accordingly, longer maturity Treasurys can play a helpful role for conservative investors, particularly because the normalized shape of the yield curve offers a measure of incremental yield. Overall, we expect interest rates to be relatively steady in the coming quarters as changes in inflation, monetary policy, market volatility, and attractive yields generally balance the forces pushing bond prices higher and lower.

Among sectors, we maintain the overweight to mortgage-backed securities (MBS). Although spreads on MBS have narrowed from previously elevated levels, the sector remains attractive. Duration extension risk should remain low, given the overhang from vast issuance at low rates earlier this decade. At the same time, well-seasoned MBS trading at discounts to par continue to offer an attractive opportunity to collect coupon payments while discounts amortize. Conversely, corporates remain underweight in the strategies owing to sizable issuance and narrow spreads relative to historical levels. Duration has been extended modestly, reflecting our preference to trade in favor of a measure of interest rate risk, while reducing some credit risk. Our aversion to tight corporate spreads is applicable to both investment and speculative grade bonds, leading us to eliminate almost all exposure to high-yield bonds.

OTHER MARKETS

We retain gold across all strategies for its role as a store of value and as a hedge against inflation and geopolitical volatility. Ongoing foreign central bank buying, alongside a broader trend toward reserve diversification beyond sole reliance on the US dollar, should sustain demand and reinforce gold’s role in a diversified, risk-managed portfolio. We also maintain platinum in the more risk-tolerant strategies, where favorable supply-demand dynamics and an attractive valuation profile support the allocation. The platinum-to-gold ratio remains attractive, and potential demand from resource hoarding and the aforementioned central bank reserve diversification could provide an additional tailwind for the metal.