Daily Comment (April 28, 2026)

by Patrick Fearon-Hernandez, CFA, and Thomas Wash

[Posted: 9:30 AM ET] | PDF

Our Comment today opens with a short update on the war in Iran. We next review several other international and US developments with the potential to affect the financial markets today, including a decision by the Bank of Japan to hold its benchmark interest rate steady despite rising price inflation due to the war and new data showing US banks have responded to deregulation by boosting their holdings of Treasurys, potentially helping cap US bond yields.

United States-Israel-Iran: New reporting confirms that Iran is rapidly running out of facilities to store its oil output as the US continues its blockade of Iranian oil-export terminals and other ports. Iran is trying to ship more oil to China by rail, but the effort is not likely to end the problem, so we see an increasing risk that Iran will have to shut in production at well sites.

- If Iran does shut in its oil wells at scale, it would be difficult and time consuming to bring them back into production quickly when the conflict ends. Some of the wells might never produce oil again.

- This is therefore another example of how the war could leave lasting scars on the global supply of oil and keep post-war oil prices from falling back to their pre-war levels.

- As the US and Iran remain far apart on their negotiating demands this morning, the Strait of Hormuz remains effectively closed and the US continues its blockade. With the standoff continuing, investors are becoming increasingly unnerved by the worsening impact on energy and commodity markets. Brent crude oil prices so far today have therefore risen about 3.0% to $104.77 per barrel.

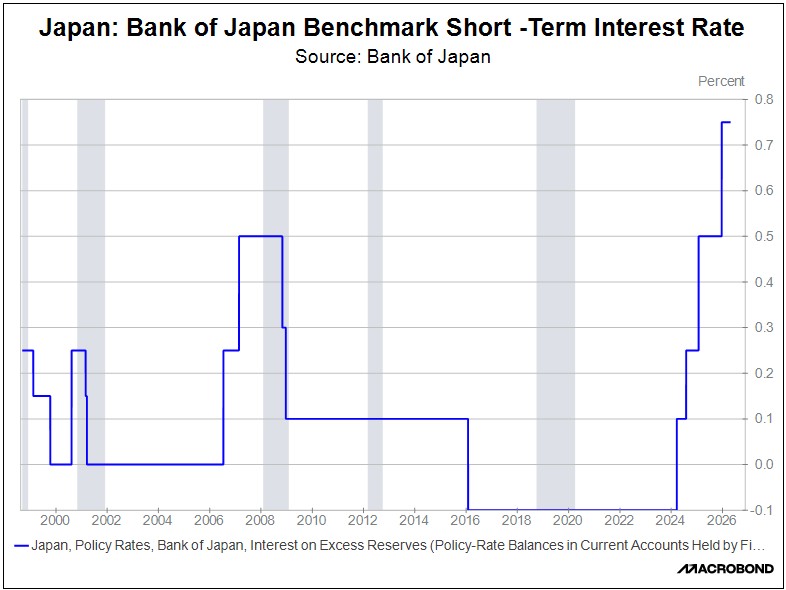

Japan: As widely expected, the Bank of Japan today held its benchmark short-term interest rate unchanged at 0.75%, despite the central bank projecting increased consumer price inflation because of the war in Iran. However, three of the nine members of the policy committee voted against the move and called for an immediate rate hike to help contain price pressures. The BOJ has been raising rates gradually to normalize policy now that deflation is less of a concern, but some investors and policymakers believe the central bank should be moving faster.

Germany: New data from the national statistics agency today showed that just over 654,000 babies were born in Germany in 2025, barely half the 1.36 million born at the peak of the baby boom in 1964 and the lowest number since post-war records began in 1946. Meanwhile, there were about 1.01 million deaths in Germany last year, highlighting the continued demographic headwinds for economic growth.

United Kingdom: In a sign of Labour Party Prime Minister Starmer’s increasing political vulnerability, parliament today will begin hearings on Starmer’s appointment of Lord Peter Mandelson as British ambassador to the US despite Mandelson’s ties to disgraced financier Jeffrey Epstein. Ultimately, the process could lead to lawmakers referring Starmer to the privileges committee for an inquiry into claims he misled parliament about Mandelson’s appointment. The resulting political instability is likely to be negative for British stocks going forward.

Canada: Prime Minister Carney yesterday announced the creation of Canada’s first sovereign wealth fund, initially capitalized at $18 billion and known as the “Canada Strong Fund.” The fund will work with the private sector to finance 15 infrastructure proposals with the country’s Major Projects Office, which was set up in August. Carney also said the fund will include a retail investment product for individuals. The fund is aimed at boosting investment and spurring faster economic growth amid the challenges of a more hostile, protectionist US.

US Monetary Policy: The Fed’s policy committee begins its latest two-day meeting today, with its decision to be released tomorrow at 2:00 PM ET. Based on interest-rate futures prices, investors are nearly unanimous in expecting the committee to keep its benchmark fed funds rate unchanged at 3.50% to 3.75%. The more significant news will be whether Chair Powell uses his post-decision press conference to reveal anything about his plans for staying on the Fed board after his chairship ends next month.

US Bond Market: New research by the Financial Times shows that net Treasury inventories held by primary dealers — the big banks that underwrite US government debt — have risen to about $550 billion on average this year, from less than $400 billion in 2025. The data suggests the recent easing of capital rules has enticed banks back into the market, providing incremental demand for Treasurys and probably helping to hold bond yields somewhat lower than they otherwise would be.

US Housing Industry: New reports say a bill passed by the Senate last month is freezing some large-scale home construction projects across the country even though it hasn’t yet passed the House or become law. The bill includes dozens of measures to make it faster and easier to build homes, such as streamlining environmental reviews and cutting rules for factory-built homes. However, it would also force developers to sell homes built to rent within seven years, forcing developers to shelve large-scale build-to-rent projects in states such as Arizona and Texas.

US Artificial Intelligence Industry: According to inside sources, OpenAI has been missing internal financial and operational goals since late last year, reflecting slowing growth in the number of regular ChatGPT users. In response, CFO Sarah Friar and members of the board have become worried that the firm might not be able to meet its contracts for future computing-power purchases. They are therefore pushing to impose more discipline on future contracts and on the firm’s build-out of data centers.

- The news of missed financial and operational goals could undermine investor enthusiasm for OpenAI ahead of its expected initial public offering later this year.

- Slowing growth in ChatGPT usage could simply reflect growing competitive pressure from other popular AI services. All the same, investors may start to interpret the slowdown as a sign that the industry is maturing faster than expected. That kind of concern would likely be negative for a swath of AI-related stocks.

US Budget Airline Industry: A trade group representing low-cost airlines yesterday said it would ask the Trump administration for $2.5 billion to offset some of the spike in fuel costs from the war in Iran. US jet-fuel prices have essentially doubled from their typical level before the war, creating an especially onerous financial burden on low-margin budget airlines. Bankrupt Spirit airlines is also seeking a $500-million loan from the federal government to stave off liquidation — a deal that could see the US taking a stake in the airline.