Asset Allocation Bi-Weekly – Are Long-Term Treasurys No Longer a Safe Haven? (March 16, 2026)

by Patrick Fearon-Hernandez, CFA | PDF

Historically, major geopolitical or economic crises, such as the war against Iran, have prompted investors to sell riskier assets and buy “safe-haven” investments whose values were expected to remain stable or even rise amid the disruptions. The most popular safe havens have been the US dollar, gold, and longer-term US Treasury obligations. Faced with the crisis, or the prospect of one, investors would typically bid up the value of the dollar versus other currencies. Many would also avidly buy up gold, driving prices for the precious metal upward. Others would snap up Treasurys, boosting their values and pushing their yields down. However, market action so far during the Iran war has defied expectations. Treasury demand has been relatively muted, and yields have been markedly resilient. This raises the question of whether long-term Treasurys are still a safe haven. And if not, why?

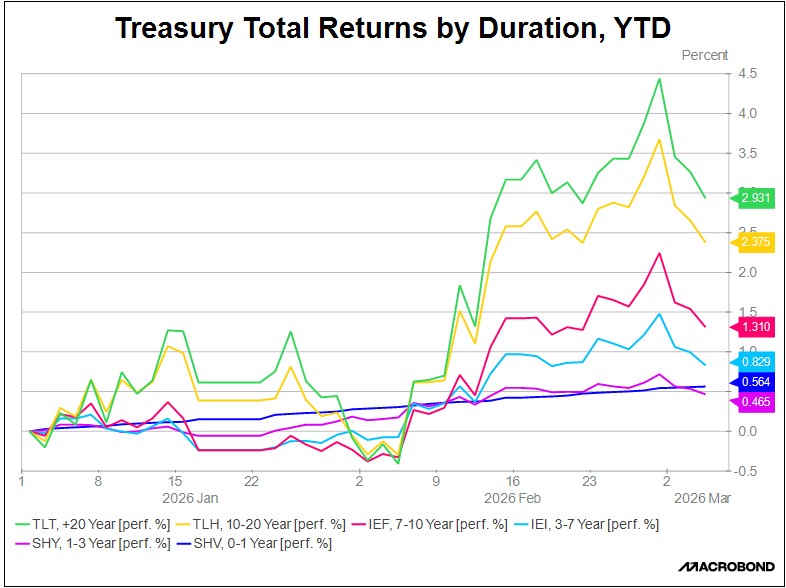

One way to see the unusual performance of long Treasurys is to compare their recent total returns versus shorter-term Treasurys. In the chart above, we show the total return (price change plus interest) for exchange-traded funds (ETFs) tracking Treasury obligations maturing in 20+ years (TLT), 10-20 years (TLH), 7-10 years (IEF), 3-7 years (IEI), 1-3 years (SHY), and 0-1 year (SHV). The graph shows how Treasurys of all tenors were bid up starting in mid-February, when it became clear that the US was prepping for a potential strike against Iran. However, once the war started, investors sold off Treasurys. The selling was especially strong for long-duration obligations as investors began to realize that the conflict could be more drawn out than anticipated, driving up global energy prices and rekindling consumer price inflation.

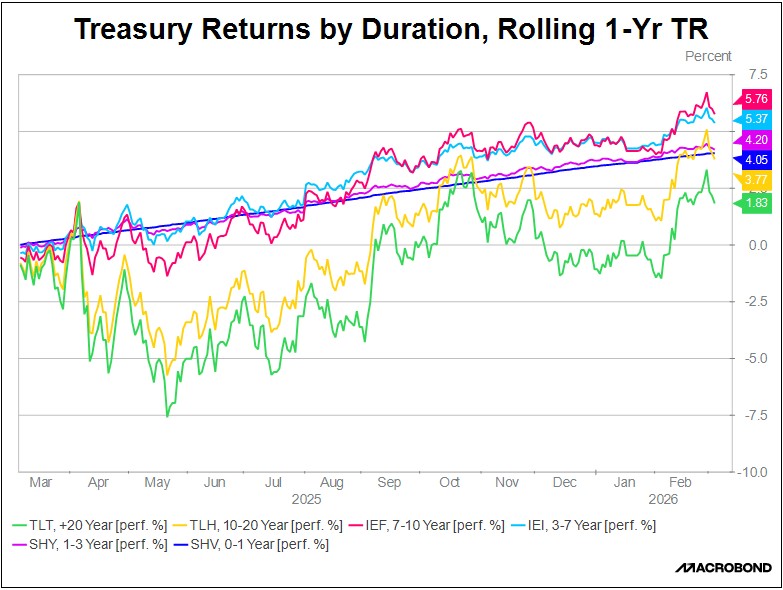

Importantly, the outsized selling of long Treasurys came after a protracted period of weak returns. The chart above displays Treasury total returns by duration over rolling one-year periods. It shows clearly how one-year returns from long Treasurys have lagged since early 2025.

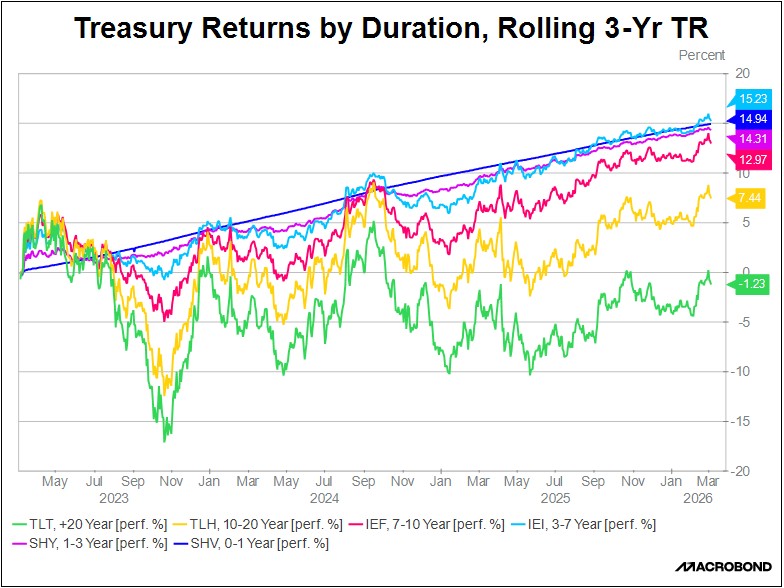

Indeed, long-term Treasury returns have lagged for quite some time. The final chart, on the next page, shows that three-year returns for long Treasurys have not only lagged shorter-term Treasury returns, but they have also lost money in the latest three-year period. This happened even though the Federal Reserve has been cutting its benchmark fed funds interest rate since September 2025. In contrast, shorter-term Treasury securities have offered steady positive returns. Shorter-term Treasurys have largely held their value even after the Iran war started and it became clear that the conflict would threaten global energy supplies and risk reigniting inflation.

Why have long Treasurys lost their attraction as a safe haven? We believe their weakness reflects increased investor concerns about US fiscal dynamics, prospects for a more politicized Fed, and fear of currency debasement. The key evidence for this has been the sell-off in long Treasurys after the war started, once it became clear that the conflict could last long enough to seriously disrupt energy supplies and cause rising global inflation. If investors were truly confident that the Fed would temporarily hike interest rates as needed to wring the inflation out of the economy and protect the purchasing power of the dollar, then demand for Treasurys should have gotten a boost from wartime safe-haven buying. However, the fact that Treasurys have not behaved as usual suggests they may have lost a lot of their cache as a safe haven. As investors also sell off gold to cover margin requirements and raise needed cash, it seems like they only see one true safe-haven asset these days, i.e., cash.