Asset Allocation Bi-Weekly – The Dip That Didn’t Bounce (March 2, 2026)

by Thomas Wash | PDF

Retail investors have emerged as a crucial stabilizing force behind the ascent of the “Magnificent 7” in recent years. Rather than displacing institutional or ETF demand, their participation has added a new, resilient layer of support. This cohort’s propensity to buy and hold mega-cap tech stocks, even through periods of market anxiety, has helped sustain momentum and enthusiasm for these names, insulating them to some degree from the sharper sentiment swings affecting the broader market.

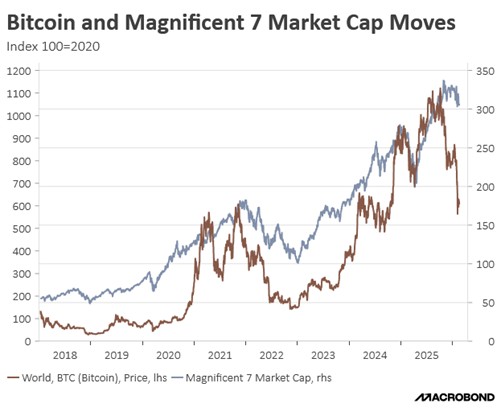

This distinct retail influence extends beyond equities, manifesting clearly in the behavior of Bitcoin. Estimates suggest that roughly two-thirds of Bitcoin’s supply remains in the hands of individual investors. Throughout 2024 and 2025, a notable correlation emerged, with Bitcoin and major tech and software names frequently moving in tandem. This parallel behavior reinforces the narrative that for many investors, particularly those with a higher risk appetite, mega-cap tech and crypto have effectively merged into a single, cohesive trade.

The sharp rise in Bitcoin and many tech-related stocks has coincided with a wave of new retail investors entering equity and crypto markets. This surge has been supported by pandemic-era stimulus payments, which boosted households’ risk-taking capacity, and by the rapid growth of easy-to-use, commission-free trading apps such as Robinhood, drawing many younger investors into markets for the first time. As a result of this new participation, the share of the daily trading volume of US equities attributable to individual investors went from the low single-digits pre-pandemic to nearly 20%.

This increased retail participation has pushed a larger share of market attention toward future growth potential and market themes, particularly in high‑growth technology and AI‑related names, rather than strictly traditional valuation metrics. Many retail investors have piled into rising tech stars, such as Nvidia, and into cryptocurrencies at the same time, often under the belief that prices would keep climbing, helping to cement a “buy‑the‑dip” mentality in which market pullbacks were frequently met with renewed retail buying.

This newer approach to investing has provided meaningful support to markets during periods of stress as it has been a source of incremental demand. Most notably, after President Trump’s “Liberation Day” tariff announcement sparked a sharp sell‑off, a strong wave of retail dip‑buying helped stabilize prices and fuel a powerful rebound. Also, brokerage and bank data indicate that retail investors’ returns around this episode and over 2025, as a whole, compared very favorably with many institutional strategies.

A major driver of this renewed wave of retail buying is the influx of younger investors into the market. Many of them have lived through a recession but have not experienced a deep, protracted equity downturn driven by widespread corporate failures. The only meaningful market pullback they recall is the 2022 episode, during which many of the hardest hit names later rebounded and went on to post extraordinary gains. As a result, many of these younger investors have held out hope that the equity market can help them accelerate their savings.

That said, retail investors — particularly younger cohorts — may prove to be a less reliable source of support for the market going forward. Using Bitcoin as a reference point, there are signs that individual traders have now become more risk‑averse, and this shift is starting to weigh on broader sentiment. This helps explain why the tech sector has seen limited upside so far this year, as investors continue to grapple with the true profitability of AI‑focused firms in light of their rising debt burdens and the threat they pose of triggering a broader “SaaS-pocalypse.”

While retail investors are likely to play a bigger role in markets over time, current uncertainty may prevent them from acting as buyers of last resort during future periods of stress. This growing risk aversion is especially likely to weigh on familiar large cap names in the technology sector. In our view, clients should pay closer attention to overlooked areas of the market as persistent pessimism toward mega‑cap tech could eventually drive a broader sector rotation as investors look to diversify into other industries.