Daily Comment (September 28, 2016)

by Bill O’Grady and Kaisa Stucke

[Posted: 9:30 AM EDT] Overall, there wasn’t much news overnight. We haven’t had much to say about Deutsche Bank (DB, $11.92, +0.07), although there have been legitimate fears that Germany’s largest bank could need a bailout despite protests to the contrary. Shares did lift this morning on news that the bank sold off some insurance assets and continues to promise it won’t raise new capital. Probably the most supportive news came from Reuters, which reported that the German government is quietly preparing a rescue plan. According to the report, the German government is prepared to acquire up to a 25% stake in the lender. Usually, the bearish trend begins to dissipate once the markets know a backstop is in place. For the broader markets, this step will be welcomed in the hope that it will reduce the odds of a financial breakdown.

The other important news is that oil prices ticked higher overnight despite the almost certain likelihood that OPEC won’t be able to negotiate a deal. We have been under the impression that the Saudis are trying to shift the blame to Iran by offering a cut only if Iran freezes its output, fully aware that the Iranians won’t accept the deal. However, reports from Bloomberg build the case that the kingdom is working toward a deal with Iran and hopes to come to an agreement at the regular meeting in November. Roughly speaking, there is a 0.6 mbpd production cut gap between Iran and Saudi Arabia that will have to be negotiated. It should be noted that even if Iran and Saudi Arabia come to an agreement, Russian oil output continues to rise, reading a new post-Soviet record of 11.1 mbpd of crude oil and condensate, exceeding the old record by 0.2 mbpd. U.S. production also appears to have stabilized. Thus, a Saudi-Iran deal within OPEC may put a floor in the market but may not lead to a major recovery.

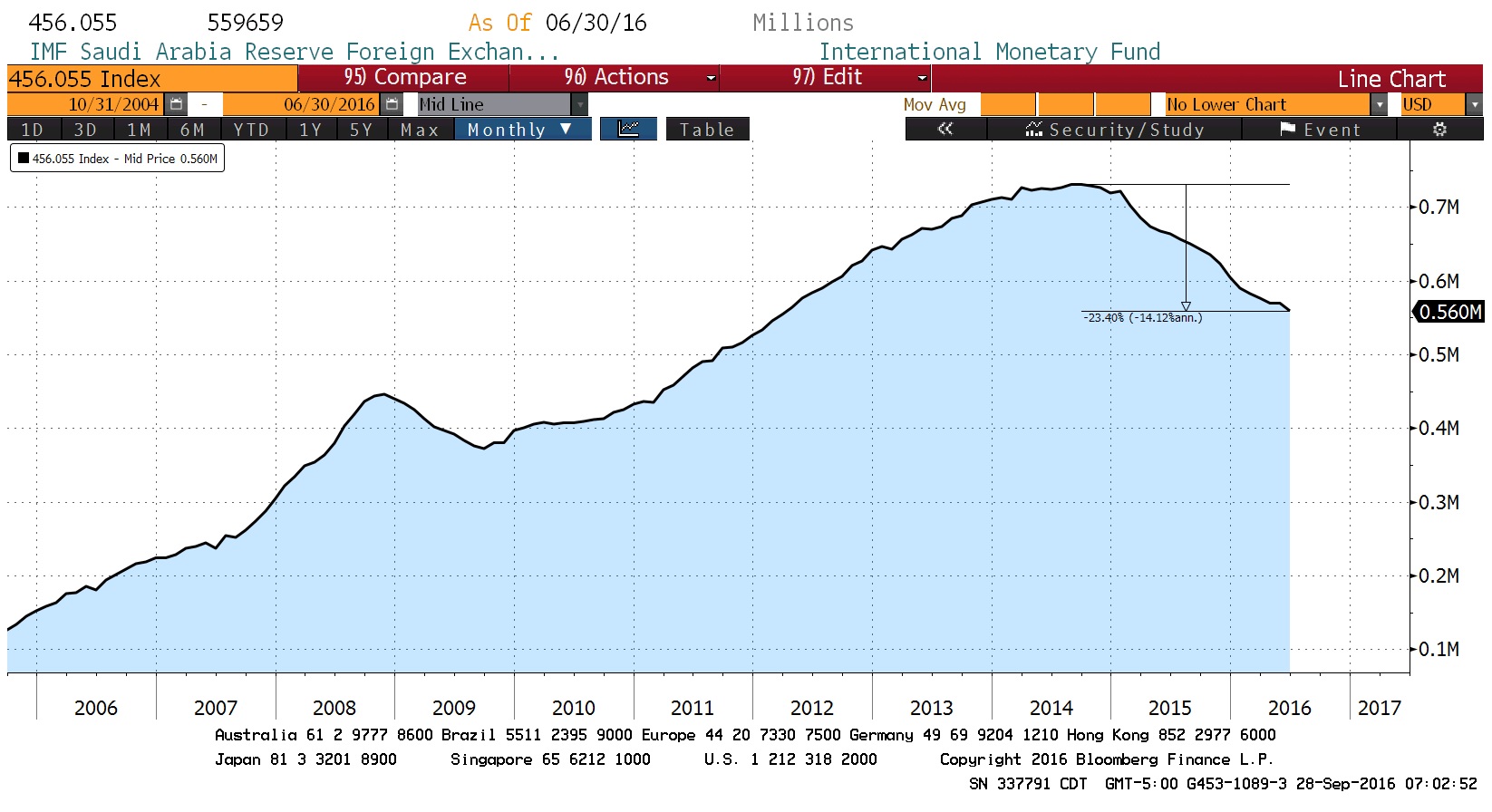

If there is an evolving change in Saudi Arabia’s production policy, suggesting the kingdom needs price relief, we suspect its coming from continued deterioration in its financial position. Earlier this week we discussed the kingdom’s plan to slash government workers’ wages and benefits. As we noted, this move undermines the Royal Family’s social contract with its people, where the people forfeit any say in running the government in return for a posh lifestyle. Here are a couple of charts that show the problems the kingdom is facing.

The chart above shows Saudi Arabia’s foreign reserves. They have declined over 23% from the peak set in September 2014, and the pace of the decline is unmistakable. In addition, the country is facing growing financial pressure.

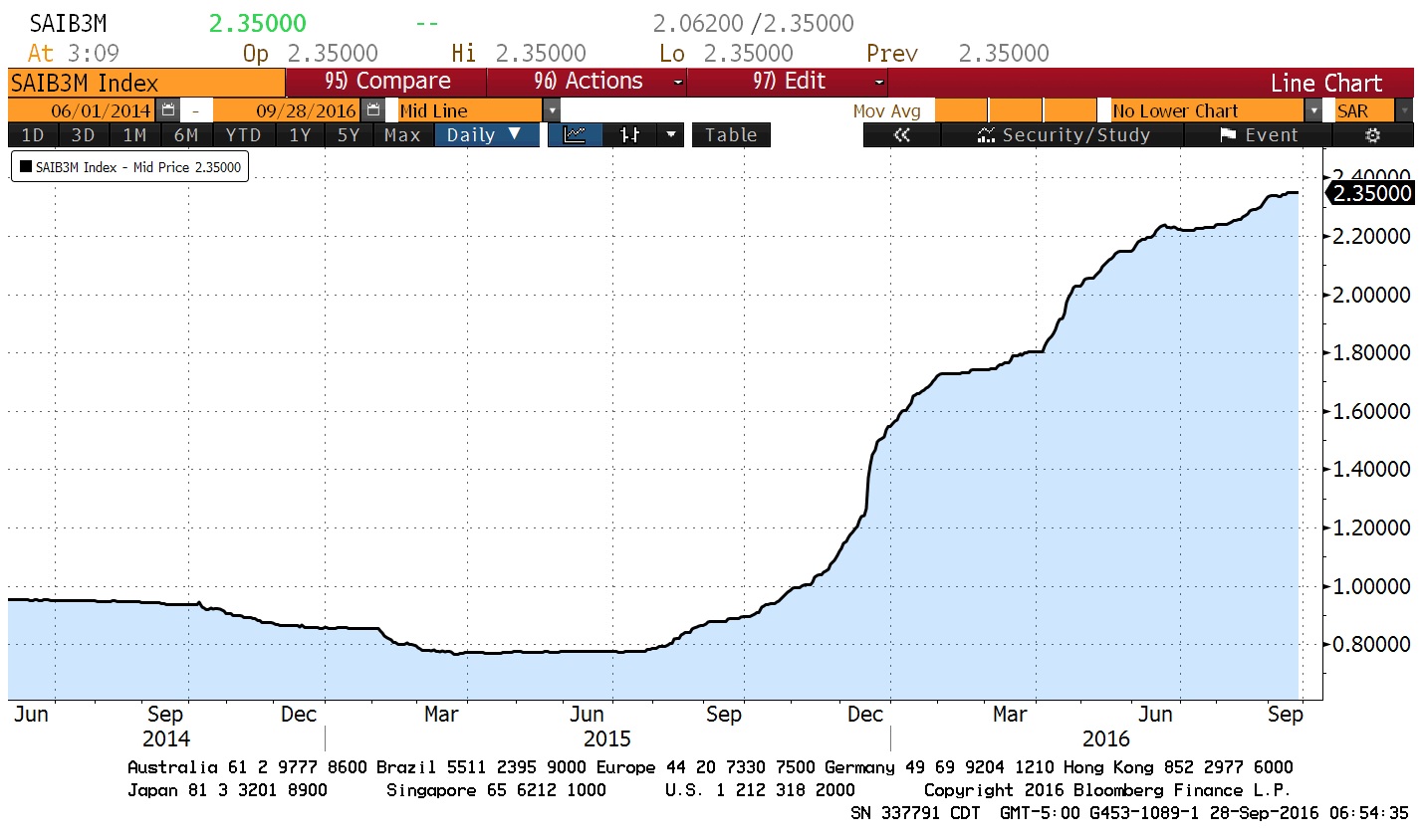

This chart shows Saudi three-month LIBOR. Since the summer of 2015, interbank lending rates in Saudi Arabia have been rising quickly. These rates can often reflect stresses in a nation’s banking system. The steady rise in yields suggests problems in the Saudi financial system.

The short-term cure to falling Saudi foreign reserves and rising financial stress is higher oil prices. The more conciliatory position may be a signal that the kingdom is “tapping out” to some extent and is preparing to abandon its singular focus on market share. We don’t know for sure whether Deputy Crown Prince Salman is the architect of this potential policy shift, or if he will step in at the last minute as he did in the spring and signal that the kingdom will maintain its goal of gaining market share. This unknown will likely be addressed in November. Nevertheless, if OPEC can signal that there is hope for a deal in two months, it would probably put a floor in prices and prevent a drop under $40 per barrel.